Key Stats for GE Stock

- Past week’s performance: -8%

- 52-week range: $159 to $348

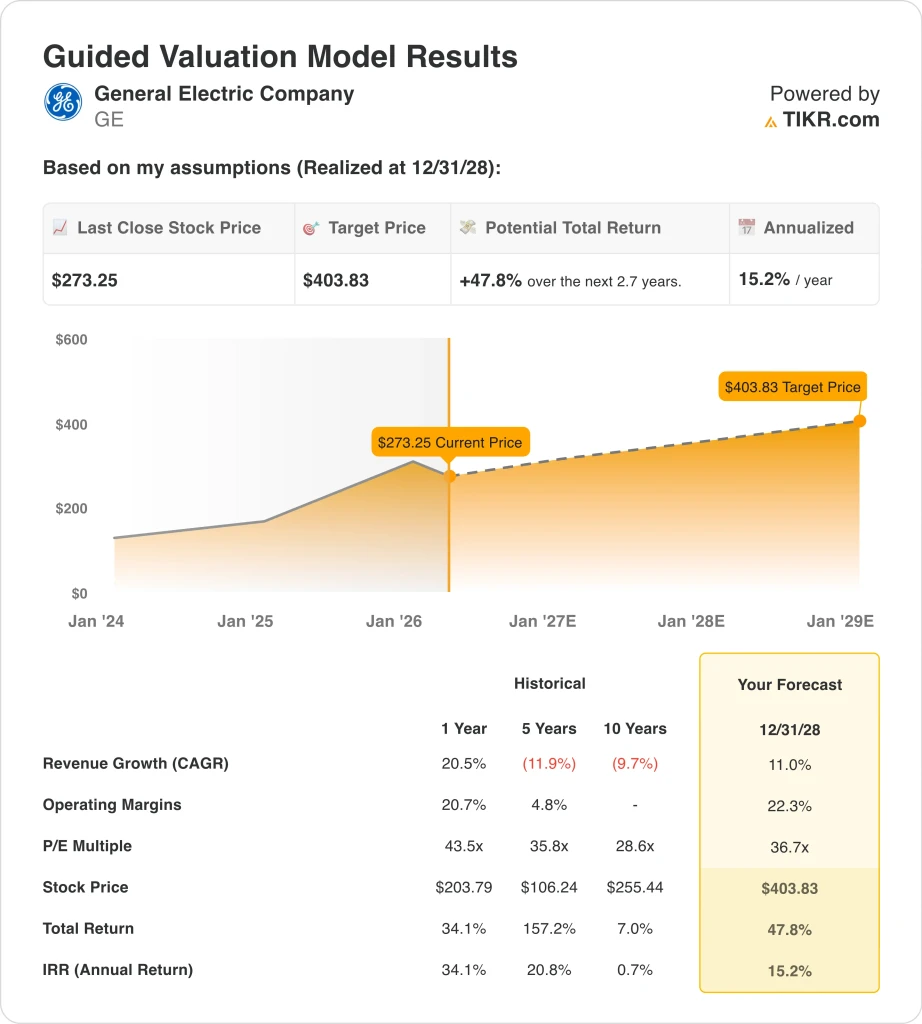

- Valuation model target price: $404

- Implied upside: 47.8% over 2.7 years

Value your favorite stocks like GE with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

General Electric Company (GE) stock fell 8% last week, and the move came even though the company kept announcing new industrial and technology investments. On March 30, GE Aerospace and Palantir said they expanded their multi-year partnership to improve U.S. Air Force aircraft readiness and GE’s own production system with AI tools.

Earlier in the month, GE also said it would invest another $1 billion in U.S. manufacturing in 2026 and more than €110 million across Europe to expand capacity.

The problem is that last week’s market was not focused only on company-specific positives. Reuters reported on March 19 that European airlines warned of higher fares and fuel shortages tied to the Iran war, while fuel prices were rising sharply.

Investors were also likely digesting how far the stock had already run before the pullback. GE Aerospace closed 2025 at $308 and ended March 30 at $273, so the stock is now down about 14.6% in 2026 after a very strong multiyear rally. When a stock has traded at premium aerospace multiples, even good news can be overshadowed by macro worries and profit-taking.

Importantly, the underlying business story has not clearly broken. GE Aerospace reported fourth-quarter 2025 adjusted EPS of $1.57, ahead of estimates, and guided for 2026 adjusted EPS of $6.20 to $6.60 with free cash flow of $6.3 billion to $6.8 billion.

CEO Larry Culp said the company entered 2026 with “continued confidence” because of strong demand, service growth, and improving deliveries.

See analysts’ growth forecasts and price targets for GE (It’s free) >>>

Is GE Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 11%

- Operating Margins: 22.3%

- Exit P/E Multiple: 36.7x

Based on these inputs, the model estimates a target price of $403.83, implying 47.8% total upside from the current share price and a 15.2% annualized return over the next 2.7 years.

The valuation case still looks attractive, but it depends on GE sustaining premium execution. A 15.2% annualized return is strong in your framework, yet the model also assumes GE can hold a 36.7x exit P/E and lift operating margins from 20.7% today to 22.3% by the end of 2028. That means the stock still needs both growth and margin expansion, not just sentiment recovery.

The good news is that the recent operating trend supports those assumptions. On an LTM basis, revenue is $42.3 billion, gross margin is 31.5%, EBIT margin is 20.7%, and forward two-year revenue CAGR is 12.0%. Those numbers matter because GE is now a more focused aerospace company, and higher-margin services revenue can drive earnings faster than equipment sales alone.

Cash generation also supports the story. GE produced $8.5 billion of cash from operations and $7.7 billion of free cash flow in 2025, while LTM net debt is about $9.6 billion, or just 0.86x EBITDA. That balance sheet gives management room to keep investing in factories, suppliers, and technology without leaning heavily on leverage.

Still, the stock is not cheap in a simple sense. The overview shows GE trading at 33.97x LTM earnings and 25.52x NTM EV/EBITDA, so the market is already paying for strong aerospace demand and execution. That is why the shares can fall hard when investors worry about airline economics, supply chains, or whether the recent growth pace can last.

What’s Driving GE Stock Going Forward?

The next major catalyst is first-quarter 2026 earnings on April 21. Investors will want updates on engine deliveries, spare-parts availability, and service growth, because those are the main levers behind GE’s profit outlook. They will also watch whether management keeps its 2026 guide intact after the recent macro volatility around fuel and airline costs.

Commercial aerospace demand remains the core driver. GE Aerospace said full-year 2025 orders rose 32% to $66.2 billion, while adjusted revenue rose 21% to $42.3 billion. A large installed engine base creates recurring maintenance and overhaul revenue, so every additional flight hour can support higher-margin services income over time.

Production ramp is the second driver. The company’s new $1 billion U.S. investment and €110 million-plus Europe investment are meant to accelerate engine deliveries, expand LEAP capacity, strengthen defense output, and support thousands of new hires.

AI and defense are also becoming more visible themes. GE’s expanded Palantir partnership is aimed at improving aircraft readiness for the U.S. Air Force and boosting manufacturing efficiency inside GE’s own plants. If management can combine stronger production, recurring services growth, and defense momentum, the market may focus again on execution rather than the short-term pullback that defined last week.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in General Electric Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze General Electric stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!