Key Stats for MCO Stock

- Past week’s performance: Consolidating

- 52-week range: $379 to $547

- Valuation model target price: $595

- Implied upside: 37.7% over 2.7 years

Value your favorite stocks like MCO with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Moody’s Corporation (MCO) stock edged up 0.9% last week, but the bigger story is that shares have been trying to stabilize after a sharp 2026 pullback. There was no major company-specific negative headline during the week, so the move looked more tied to broader market swings than a change in Moody’s fundamentals.

On March 24, U.S. stocks fell as rising oil prices, higher Treasury yields, and Middle East tensions pressured sentiment, and Moody’s also traded lower with other financial-data names that day.

At the same time, investors are still trading Moody’s against the outlook it gave in February. The company reported fourth-quarter adjusted EPS of $3.64, ahead of the $3.42 analyst consensus, and guided 2026 adjusted EPS to $16.40 to $17.00. Reuters said the stock jumped more than 6% after that report because management also pushed back on fears that AI would erode the business.

That matters because Moody’s has two engines. Moody’s Investors Service is the ratings business, which benefits when companies issue more debt, while Moody’s Analytics sells software, data, and risk tools that generate more recurring revenue. CEO Rob Fauber said 2025 was a “record year” and said Moody’s enters 2026 “well positioned and confident in the opportunities ahead.”

So last week’s quiet move likely reflected a balance of forces. Macro volatility and higher yields can pressure valuation multiples in the short run, but Moody’s still has support from healthy issuance, private credit growth, and strong analytics demand. With the next earnings report expected on April 21, investors appear to be waiting for a fresh data point rather than making a big directional bet now.

See analysts’ growth forecasts and price targets for MCO (It’s free) >>>

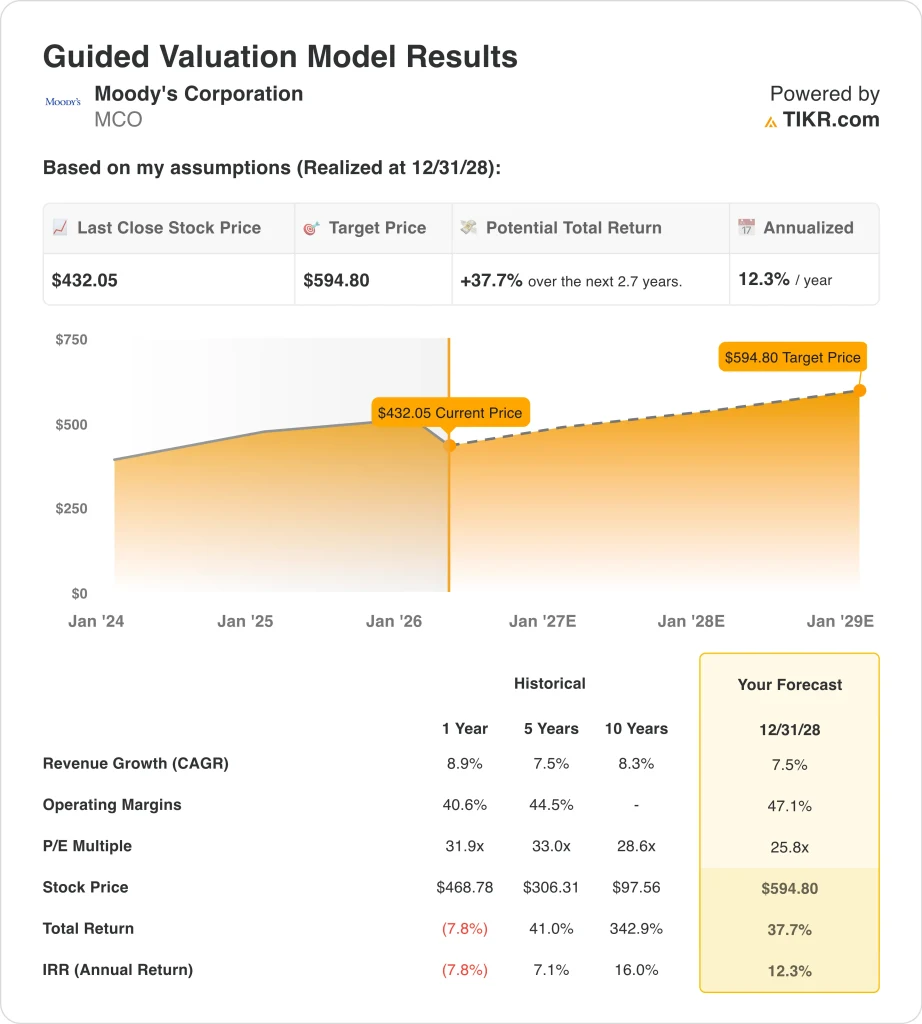

Is MCO Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 7.5%

- Operating Margins: 47.1%

- Exit P/E Multiple: 25.8x

Based on these inputs, the model estimates a target price of $594.80, implying 37.7% total upside from the current share price and a 12.3% annualized return over the next 2.7 years.

Moody’s does not look cheap on today’s multiples, but the model still points to a reasonable long-term return. The stock trades at about 31.6x LTM earnings and 10.6x LTM EV/revenue, while the valuation model assumes a lower 25.8x exit P/E. That means part of the return case comes from earnings growth and margin expansion rather than multiple expansion.

The operating profile helps explain why the market gives Moody’s a premium. In 2025, revenue rose 8.9% to $7.7 billion, operating income increased 16.3% to $3.5 billion, and LTM EBIT margin reached 44.9%. Free cash flow was also strong at about $2.6 billion, which supports both buybacks and dividend growth.

The business drivers are also clear. Moody’s said it rated a record $6.6 trillion of debt in 2025, and private credit revenue in MIS grew nearly 60%. On the analytics side, management said customer demand remains strong because funding needs, compliance demands, and risk complexity are all rising.

That leaves the key valuation question centered on durability. If revenue compounds near 7.5% and margins move toward 47.1%, the stock can justify a higher fair value even with a lower exit multiple. But because Moody’s is still a premium-quality financial-data name, the shares can stay sensitive to rate shocks and swings in issuance sentiment.

What’s Driving MCO Stock Going Forward?

The next major catalyst is the first-quarter results on April 21. Investors will focus on whether issuance stayed healthy through a more volatile bond market and whether analytics growth remained resilient. The company also has its annual meeting on April 14, which could bring more commentary on capital allocation and governance.

Bond-market activity remains one of the most important drivers. Moody’s said it expects total issuance in 2026 to rise at a low single-digit pace, with debt-funded M&A issuance up 40% to 45%. That outlook also includes continued issuance from hyperscalers and AI-driven data centers, which has become a meaningful tailwind for the ratings business.

Management also expects solid company-wide execution. Moody’s guided for high-single-digit revenue growth in 2026, adjusted operating margin of 52% to 53%, free cash flow of $2.8 billion to $3.0 billion, and about $2.0 billion of share repurchases.

Chief Executive Rob Fauber said Moody’s is embedding “decision-grade, contextual intelligence” into customer workflows, which is management’s way of saying the company wants its data and models to be used directly inside daily client decisions.

Another driver is competitive positioning. Moody’s has been arguing that AI is more of an enabler than a threat because its proprietary data, methodologies, and regulatory standing are hard to replicate. If debt issuance, private credit, and analytics demand all stay healthy, investors may focus more on earnings durability than on the macro noise that moved the stock around last week.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Moody’s Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MCO, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track MCO alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Moody’s stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!