Key Stats for Starbucks Stock

- Past week’s performance: -6.4%

- 52-week range: $76 to $105

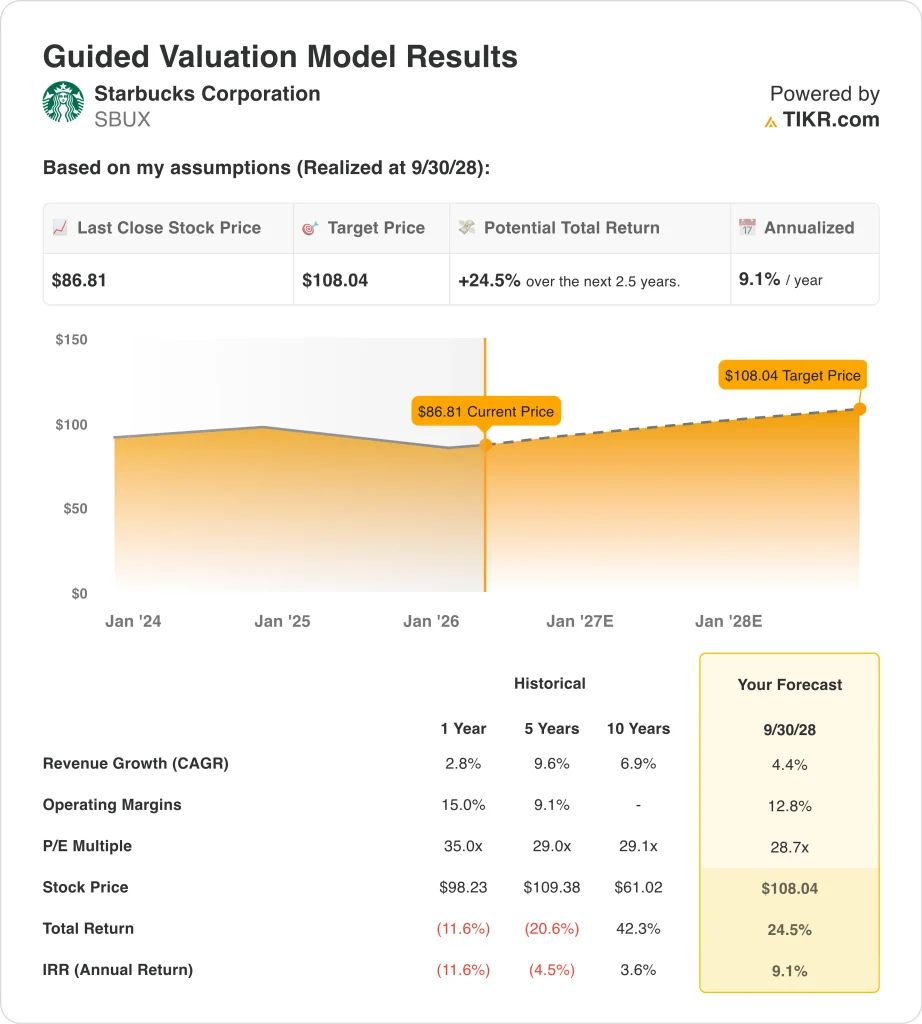

- Valuation model target price: $108

- Implied upside: 24.5% over 2.5 years

Value your favorite stocks like SBUX with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Starbucks Corporation (SBUX) stock fell 6.4% last week as investors weighed new labor and governance headlines against an already fragile margin story. The company’s annual meeting landed in the middle of that debate, and the market seemed to focus more on unresolved risks than on the company’s longer-term turnaround message. That helps explain why the stock weakened even without a new earnings report.

One pressure point was labor. Reuters reported on March 30 that Starbucks investors reelected the full board, rejecting a labor-backed challenge tied to the board’s decision to dissolve its labor oversight committee. Reuters had also reported earlier in March that ISS and Glass Lewis warned shareholders about financial and reputational risks tied to the company’s labor disputes, while Starbucks said unionized stores represent 6% of its U.S. footprint.

Another pressure point was the margin outlook. RBC downgraded Starbucks to “sector perform” from “outperform,” saying ongoing labor costs and future investment needs made the risk-reward more balanced. The same note said North America sales could improve, but that the required investments looked larger and more permanent, and the margin path remained unclear.

Investors also got another restructuring headline at the end of the week. A Reuters brief said Starbucks will lay off 69 employees in Seattle under a WARN notice, adding to the sense that management is still reshaping the business as part of its turnaround. So the stock’s weekly decline looked tied less to demand collapsing and more to investors recalibrating how expensive this recovery may be.

See analysts’ growth forecasts and price targets for SBUX (It’s free) >>>

Is SBUX Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 4.4%

- Operating Margins: 12.8%

- Exit P/E Multiple: 28.7x

Based on these inputs, the model estimates a target price of $108, implying 24.5% total upside from the current share price and a 9.1% annualized return over the next 2.5 years.

The valuation setup looks more balanced than obviously cheap. A 9.1% annualized return is decent, but it sits below the stronger return thresholds in your framework, so the stock does not screen as deeply undervalued. That makes execution especially important because the model only assumes mid-single-digit revenue growth and a modest margin recovery.

Those assumptions are grounded in a business that is still profitable, but less efficient than it used to be. LTM revenue was $37.7 billion, but gross margin fell to 22.2%, and EBIT margin fell to 9.4%. That matters because Starbucks is spending more on labor, store operations, and restructuring while also dealing with elevated coffee costs and tariffs.

The balance sheet also explains part of the market’s caution. Starbucks carries about $21.9 billion of LTM net debt, and its payout ratio is above 200%, while free cash flow has fallen to about $2.3 billion on an LTM basis. That does not mean the business is broken, but it does mean investors want clearer proof that sales gains can turn back into stronger cash generation.

Still, the company has meaningful scale and brand strength. Starbucks ended Q1 fiscal 2026 with 41,118 stores, and Q1 global comparable sales rose 4%, including 4% in the U.S. and 7% in China. So the valuation case depends on whether management can restore margins without stalling that traffic recovery.

What’s Driving SBUX Stock Going Forward?

The next big catalyst is earnings. Starbucks is expected to report Q2 fiscal 2026 results on April 28, and investors will be watching whether traffic gains continue and whether margin pressure starts to ease. Because the stock sold off on margin concerns last week, that report could matter more than usual.

Management is framing the story around operational improvement. In the Q1 release, CEO Brian Niccol said, “Our Q1 results demonstrate our ‘Back to Starbucks’ strategy is working, and we believe we’re ahead of schedule.” CFO Cathy Smith added that the company sees a clear path to translating topline strength into sustainable earnings growth, which is exactly what investors now want to see in the numbers.

The core drivers are straightforward. Starbucks said Q1 consolidated net revenue rose 6% to $9.9 billion, helped by a 4% increase in global comparable sales, but GAAP operating margin still contracted 290 basis points to 9.0%.

Investors should also watch store productivity and customer experience initiatives. Starbucks said Green Apron Service has improved speed and throughput, and the company expects to add more than 25,000 café seats in the U.S. by the end of fiscal 2026.

If those changes lift repeat visits and average store sales without requiring permanently lower margins, the stock’s current valuation could look more reasonable over time.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Starbucks Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SBUX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SBUX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Starbucks stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!