Key Stats for TOST Stock

- This-Week Performance: -5%

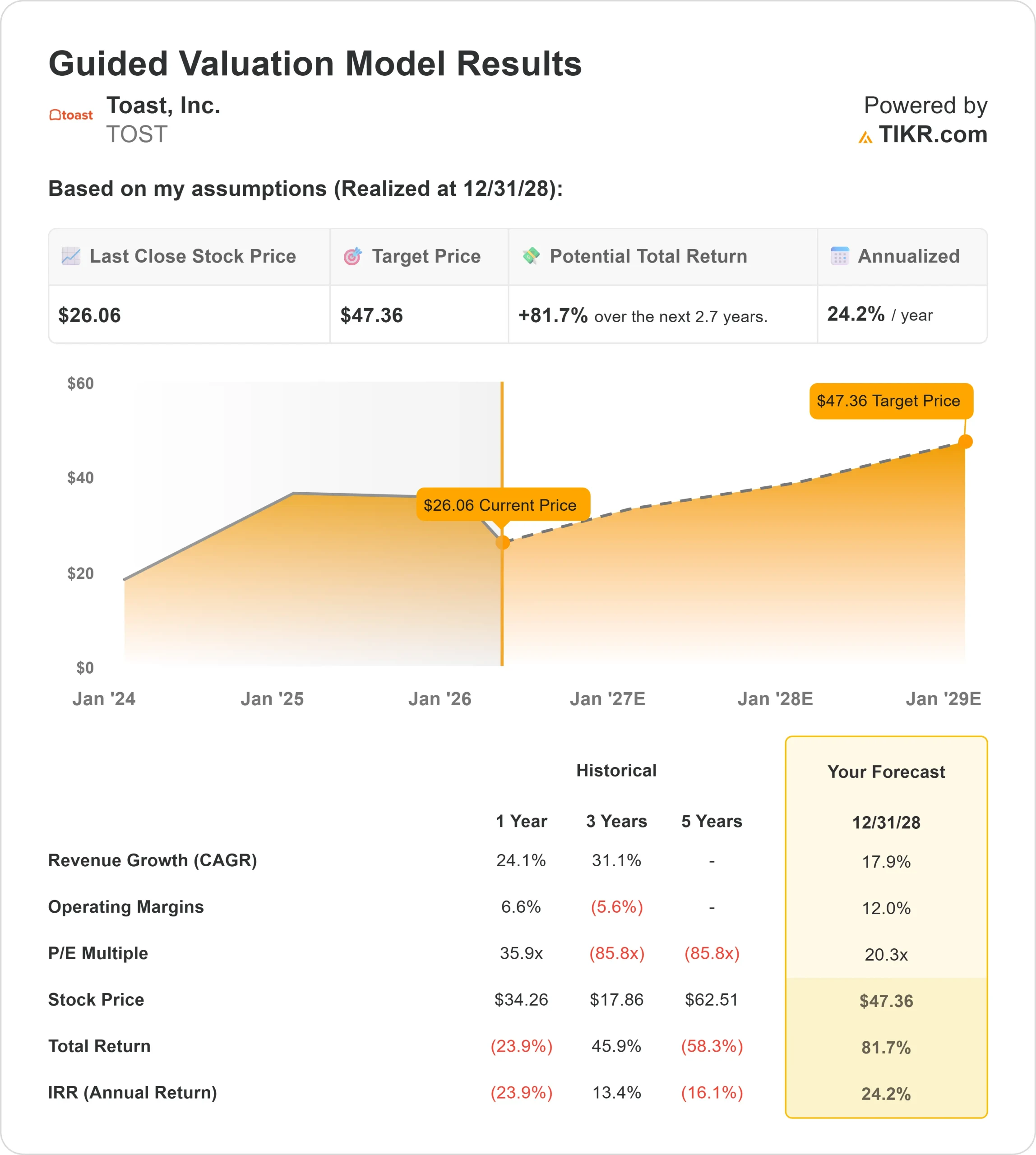

- 52-Week Range: $24 to $50

- Valuation Model Target Price: $47

- Implied Upside: 82%

Analyze your favorite stocks like Toast with TIKR (It’s free) >>>

What Happened?

Toast stock is down about 5% this week, trading near $26 per share, as restaurant software stocks have been volatile in 2026 and investors debate whether high-growth platforms like Toast can translate strong revenue growth into consistent profitability, with valuation multiples across software stocks remaining under pressure.

The decline was driven by concerns around valuation and profitability, as investors sold higher-growth software companies that are still scaling margins, with Toast facing more scrutiny compared to competitors like Block’s Square, Lightspeed, and Fiserv’s Clover, which have more established operating histories and broader product ecosystems.

At the Morgan Stanley Technology, Media & Telecom Conference, Toast reinforced strong underlying momentum, highlighting that it has surpassed $2 billion in ARR, grew recurring gross profit 33% last year, and now has 20% share of U.S. SMB and mid-market restaurants, while guiding for 20% to 22% recurring gross profit growth in 2026.

CEO Aman Narang also pointed to accelerating efficiency gains from AI, noting top developers are now “twice as effective,” while about one-third of support tickets no longer require human intervention.

Recent institutional filings showed notable shifts in positioning. AllianceBernstein increased its stake to 8,215,758 shares worth about $300 million, while Nordea Investment Management raised its position by 843% to over 1,307,158 shares worth about $47 million.

At the same time, Riverbridge Partners cut its stake by 21.6% to about 755,052 shares, and Congress Asset Management reduced its position by 36.1% to roughly 776,735 shares, as some investors added exposure while others trimmed positions following the recent run-up in the stock.

Value Toast instantly (Free with TIKR) >>>

Is TOST Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 17.9%

- Operating Margins: 12.0%

- Exit P/E Multiple: 20.3x

Toast’s platform combines point-of-sale software with payments, payroll, lending, and marketing tools, which allows the company to generate recurring revenue each time a restaurant processes transactions or uses additional services.

See analysts’ growth forecasts and price targets for Toast (It’s free) >>>

Growth is increasingly driven by higher revenue per location, as existing customers adopt more of these products, which expands monetization without relying solely on adding new restaurant locations.

This model supports margin expansion because software and fintech services carry higher margins than hardware, and as more revenue shifts toward these products, overall profitability improves over time.

Toast continues to compete in a fragmented market against providers like Block’s Square, Lightspeed, and Fiserv’s Clover, but its restaurant-focused platform supports strong product adoption and customer retention, which positions the company to continue gaining share.

Based on these inputs, the model estimates a target price of $47, implying about 82% upside over roughly 3 years, indicating the stock appears undervalued at current levels, with future performance likely driven by margin expansion, fintech monetization, and continued growth in recurring revenue.

How Much Upside Does TOST Stock Have From Here?

Investors can estimate Toast’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.