Key Stats for BILL Stock

- Past-Week Performance: -7.2%

- 52-Week Range: $35.5 to $57.2

- Current Price: $37.2

What Happened?

Bill Holdings (BILL), a cloud-based financial operations platform serving small and mid-sized businesses, proved its growth re-acceleration thesis when Q2 core revenue surged 17% year-over-year to $375 million, beating guidance and lifting the stock to $37.24.

On February 5, BILL reported Q2 total revenue of $414.7 million against an IBES estimate of $398.4 million, while adjusted net income of $73.4 million beat the $64.3 million consensus, prompting management to raise full-year core revenue guidance by roughly 170 basis points to $1.49 billion–$1.51 billion.

The sharpest proof of platform momentum came from Spend and Expense, BILL’s corporate card and expense management business, where revenue grew 24% year-over-year to $166 million, driven by a record card spend per business of $148,000 and card payment volume growth of 25%.

CFO Rohini Jain stated on the Q2 earnings call that “we accelerated core revenue growth and strengthened our margin profile, proving that our disciplined investment approach and improved execution are delivering tangible results,” a statement backed by non-GAAP operating margin expanding 290 basis points year-over-year to 18%.

BILL’s Embed 2.0 distribution strategy, which embeds BILL’s payment infrastructure inside partner platforms like NetSuite, Acumatica, and Paychex to reach close to 1 million additional businesses, combined with $400 million in contracted Supplier Payments Plus volume and an active $133 million share repurchase program in Q2 alone, positions the company to compound its 4%–5% current market share across a largely untapped SMB addressable market over the next three to five years.

Wall Street’s Take on BILL Stock

The Q2 revenue re-acceleration, the 170-bps guidance raise, and the 290-bps margin expansion together confirm that BILL’s core platform growth is compounding, not decelerating, directly improving the earnings trajectory that anchors the stock’s forward valuation.

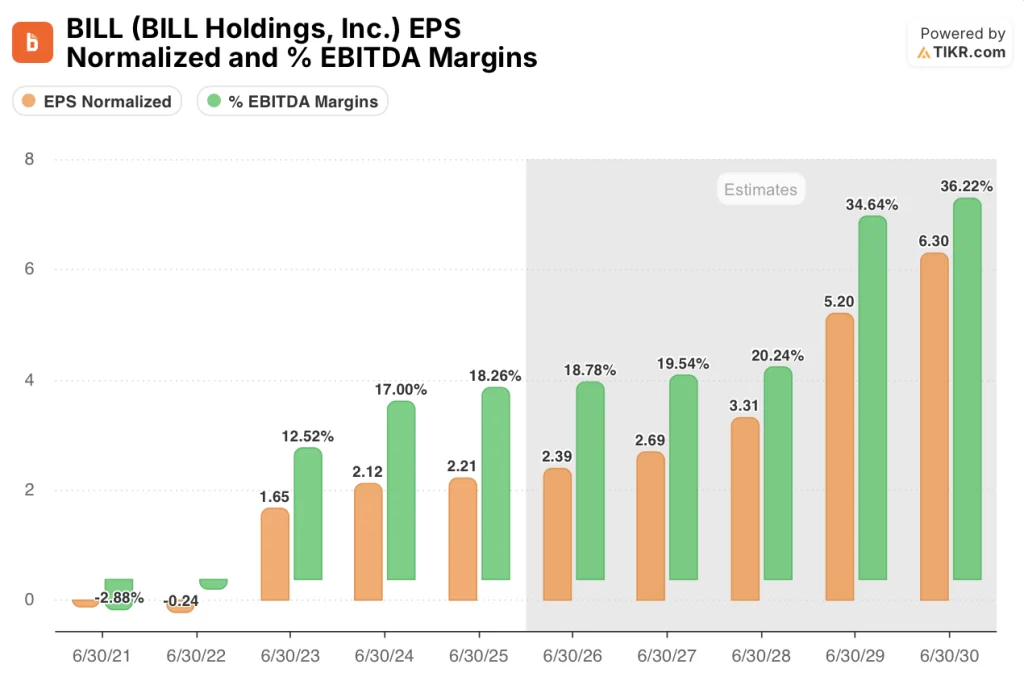

As TIKR estimates, normalized EPS grows from $2.21 in FY25 to $2.39 in FY26 and $2.69 in FY27, supported by EBITDA margins expanding from 18.3% to 18.8% to 19.5%, as the 17% Q2 core revenue acceleration, record $148,000 card spend per business, and AI agents reducing manual fraud reviews by 40% compound into a structurally more efficient earnings base.

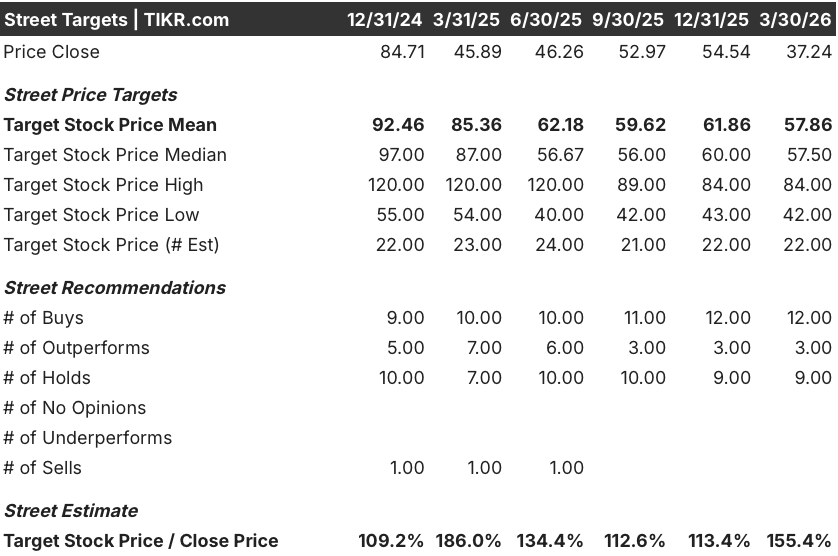

A wall of 12 buys, 3 outperforms, and 9 holds among 24 covering analysts puts the mean price target at $57.86, implying 55.4% upside from $37.24, with analysts anchoring on the platform’s multiproduct adoption acceleration and the Embed 2.0 distribution buildout as the primary re-rating triggers.

The spread between the $42.00 analyst low and $84.00 high reflects a binary read on execution: the low case prices in continued SMB macro softness compressing card spend, while the $84.00 high case prices in Embed 2.0 and Supplier Payments Plus, BILL’s enterprise supplier monetization product, reaching material revenue contribution by FY27.

What Does the Valuation Model Say?

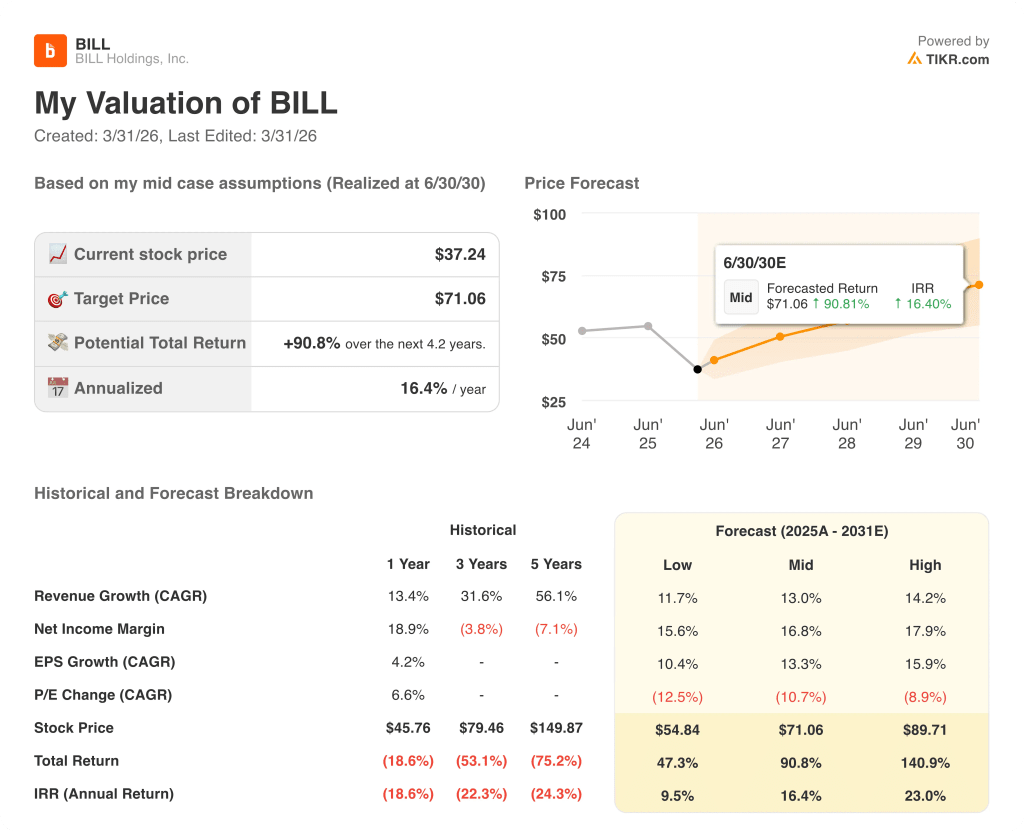

As TIKR estimates, BILL’s mid-case price target of $71.06 by June 2030 implies a 90.8% total return and a 16.4% IRR, grounded in a 13% revenue CAGR and net income margins expanding from 16.7% in FY26 to 24.8% by FY30, with the Embed 2.0 channel and AI-driven operating leverage as the primary compounding drivers.

At 15.6x forward FY26 normalized EPS of $2.39, BILL trades at a steep discount to its own implied historical multiples when the mean Street target sat at $92.46 in December 2024 against comparable EPS, making the current multiple look disconnected from a business delivering 17% core revenue growth: undervalued.

The TIKR mid-case $71.06 target is justified by the platform’s confirmed 28% multiproduct adoption growth, the $400 million in contracted SPP volume, and management’s raised FY26 core revenue guidance of $1.49 billion–$1.51 billion.

Rene Lacerte’s disclosure at the Morgan Stanley conference that Embed 2.0 partners signed contracts covering all BILL payment products from day one signals monetization optionality the current $37.24 price does not reflect.

The key risk is card spend per business reversing below the record $148,000 Q2 level, which would compress Spend and Expense revenue, the segment delivering 24% YoY growth and supporting the margin expansion trajectory the TIKR model depends on.

Q3 FY26 results, due in early May, are the next confirmation point: watch core revenue against the $364.5 million–$374.5 million guidance range and non-GAAP operating income against the $62.5 million–$67.5 million target.

Should You Invest in BILL Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BILL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track BILL Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BILL stock on TIKR for Free →