Key Stats for NCLH Stock

- Past week’s performance: -12.7%

- 52-week range: $14 to $27

- Valuation model target price: $24

- Implied upside: 33.7% over 2.7 years

Value your favorite stocks like NCLH with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Norwegian Cruise Line Holdings (NCLH) stock fell 12.7% last week as investors focused on two pressures at once. The company announced a major board overhaul on March 27 after reaching a cooperation agreement with Elliott Investment Management. But the stock still stayed under pressure because investors were also dealing with rising fuel costs and a softer 2026 setup.

The board changes were significant. Norwegian Cruise said it will add five new independent directors, CEO John Chidsey will become chairman, and four directors will step down effective March 31. Reuters said Elliott had built a stake of more than 10%, pushed for changes, and became the company’s largest shareholder.

Even so, the governance news did not erase the macro overhang. Reuters reported on March 16 that oil prices had risen more than 35% since the conflict in Iran began, and Brent had crossed $100 a barrel. That matters for cruise operators because fuel is a major operating cost, so higher oil prices can quickly pressure margins.

Sector headlines added to the pressure late in the week. Carnival cut its annual profit forecast because higher fuel costs were weighing on margins, even though bookings stayed strong. That reinforced concerns already hanging over Norwegian after its March 2 earnings report, when management flagged uncertain fuel costs, pressured demand, and a muted 2026 profit outlook.

See analysts’ growth forecasts and price targets for NCLH (It’s free) >>>

Is NCLH Stock Undervalued?

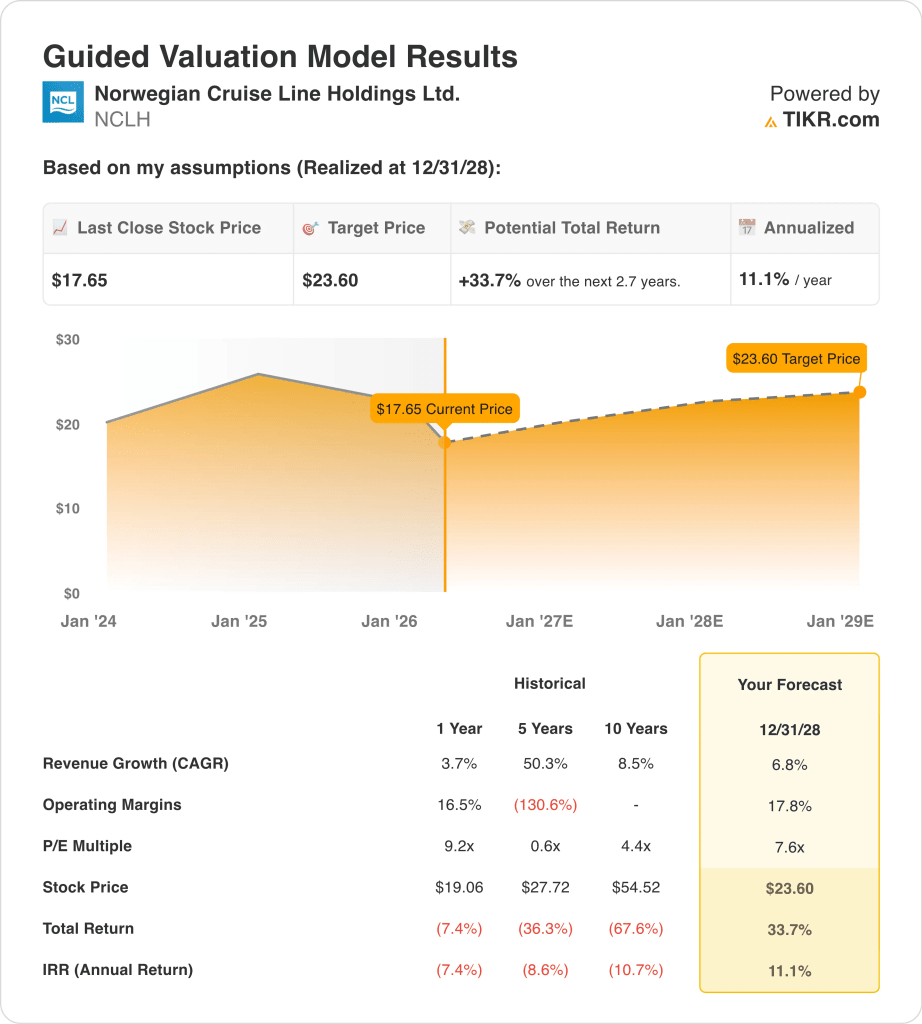

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 6.8%

- Operating Margins: 17.8%

- Exit P/E Multiple: 7.6x

Based on these inputs, the model estimates a target price of $24, implying 33.7% total upside from the current share price and a 11.1% annualized return over the next 2.7 years.

The valuation case looks reasonable, but it is not low-risk. An 11.1% annualized return is attractive enough to matter, yet it depends on Norwegian delivering margin gains while carrying heavy leverage. The company still has about $15.3 billion of net debt, and that keeps the equity sensitive to booking trends, fuel costs, and execution.

Norwegian Cruise has clearly improved since the pandemic, and that supports part of the valuation. Revenue rose 3.7% to $9.8 billion in 2025, gross margin improved to 42.6%, and EBIT margin reached 15.9%. Adjusted EBITDA increased 11% to $2.73 billion, which shows the fleet is producing better onboard spending and ticket economics even in a tougher backdrop.

But the market is also discounting real issues. GAAP net income fell to $423 million in 2025 from $910 million in 2024, and fourth-quarter revenue of $2.24 billion missed analyst estimates, according to Reuters. On top of that, the company entered 2026 with flat net-yield guidance and said it was operating against a “pressured backdrop” after commercial execution missteps.

That mix explains why the stock can look inexpensive and still stay volatile. Norwegian trades far below its 52-week high, but it also has much more balance-sheet risk than asset-light travel companies. Reuters noted the stock has fallen nearly 30% over the last five years, while Royal Caribbean surged 211%, so investors still want proof that this turnaround can close the gap.

What’s Driving NCLH Stock Going Forward?

The next driver is execution on demand and pricing. In its March 2 results, the company said 2026 net yield on a constant-currency basis is expected to be about flat, while Q1 net yield is expected to decline about 1.6%. Management tied part of that weakness to a 40% year-over-year increase in Caribbean capacity and a mismatch between commercial strategy and deployment.

Fuel will stay in focus, too. Norwegian told Reuters it is monitoring the Middle East situation closely and does not currently expect itinerary impacts, but executives also said the long-term effect on fuel costs remains uncertain. That matters because even if demand holds up, a higher fuel bill can still limit earnings growth and slow deleveraging.

Management is also trying to improve the underlying business. CFO Mark Kempa said, “Our priorities in 2026 are centered around improving financial performance, overall execution, and reducing Net Leverage.” The company expects 2026 adjusted EBITDA of about $2.95 billion, adjusted EPS of $2.38, and year-end net leverage of about 5.2x, so investors will be watching whether those targets hold.

There are still some constructive signals underneath the noise. Norwegian said 2026 occupancy is expected to reach 105.7% versus 103.5% in 2025, and demand has been especially strong in its luxury brands. Oceania Sonata posted record opening bookings, and Regent recorded its strongest booking month ever in January, so the key question is whether that strength can outweigh fuel volatility and broader consumer caution.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Norwegian Cruise Line Holdings Ltd.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NCLH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NCLH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Norwegian Cruise Line stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!