Key Stats for COIN Stock

- Year-to-Date Performance: -23%

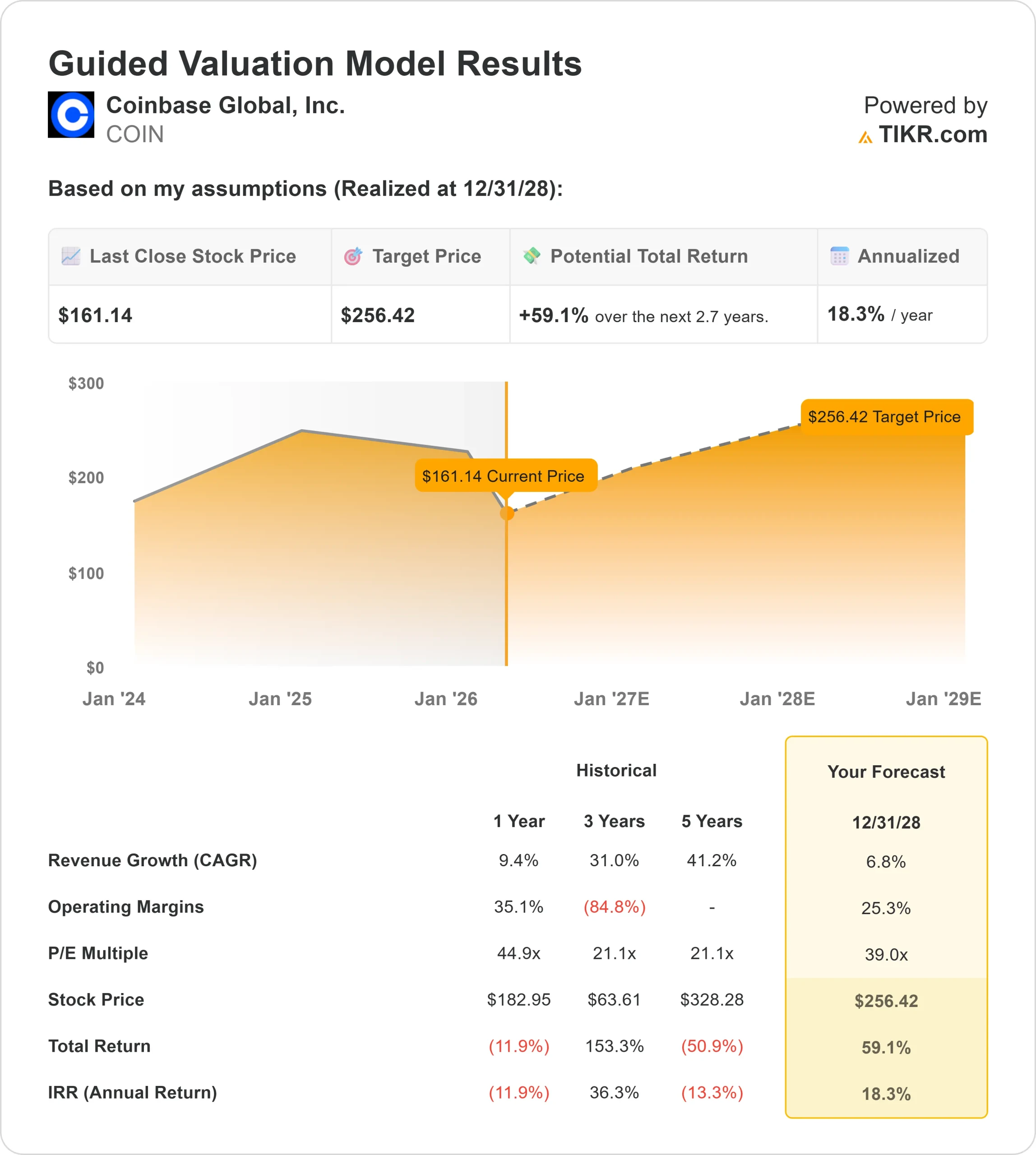

- 52-Week Range: $139 to $445

- Valuation Model Target Price: $256

- Implied Upside: 59%

Analyze your favorite stocks like Coinbase Global with TIKR (It’s free) >>>

What Happened?

Coinbase Global, Inc. stock is under pressure in 2026, with shares down about 23% year to date as a crypto market pullback earlier in the year, driven by institutional selling, macro risk-off sentiment, and regulatory uncertainty, weighed on trading activity and investor confidence. As crypto has become more institutionally owned, price declines have been more closely tied to broader market conditions, increasing volatility and pressure on trading platforms like Coinbase.

The stock is down primarily because earlier declines in major cryptocurrencies, driven by a macro risk-off environment and institutional selling, reduced trading volumes and lowered near-term revenue expectations. Because Coinbase’s earnings are highly sensitive to transaction activity, even modest declines in prices and volatility can lead to disproportionately weaker revenue.

At the same time, macro uncertainty and regulatory concerns around stablecoin rules added further pressure on sentiment by increasing uncertainty around future growth.

Over the past week, shares rebounded about 9% and now trade near $175 per share, as crypto prices moved higher after a period of weakness, lifting trading activity across the platform and improving short-term expectations. This bounce reflects how quickly sentiment can shift when crypto markets recover, even if the broader trend remains negative.

In early March at the Morgan Stanley Technology, Media & Telecom Conference, CFO Alesia Haas highlighted that Coinbase now has 12 products generating over $100 million in annual revenue, with 2 products exceeding $1 billion, while trading volume has doubled year over year driven by derivatives growth and expansion into new areas like equities and prediction markets. She also noted that retail users remain active despite volatility, stating that “the vast majority are holding their assets,” with many continuing to buy during market dips.

Recent institutional activity also reflects mixed but active positioning. Nepsis Inc. increased its stake by 23.8% to about $9.6 million, while Exchange Traded Concepts LLC raised its position by 28.6% to roughly $48.6 million, and Union Bancaire Privee UBP SA significantly expanded its holdings.

At the same time, Assenagon Asset Management reduced its stake by 76.7%, highlighting divergence in views, with institutional ownership remaining elevated at about 68.8%.

Value Coinbase Global instantly (Free with TIKR) >>>

Is COIN Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 6.8%

- Operating Margins: 25.3%

- Exit P/E Multiple: 39x

Revenue growth is expected to normalize after the extreme swings seen in prior crypto cycles, with expansion increasingly supported by subscription and services revenue such as custody, staking, and interest income rather than purely transaction-driven activity. These services generate more stable revenue compared to trading, which depends heavily on market conditions.

At the same time, trading remains the core earnings driver, especially as Coinbase expands into derivatives, which are contracts that allow traders to bet on price movements with leverage. Volumes in this segment have already doubled year over year and tend to carry higher margins than spot trading.

See analysts’ growth forecasts and price targets for Coinbase Global (It’s free) >>>

Operating margins reflect this balance between scalability and cyclicality, as trading-driven revenue can expand profitability quickly during strong markets but compress during weaker periods when activity slows. Cost discipline and continued scaling of higher-margin services will determine how much of that revenue translates into consistent earnings.

Based on these inputs, the model estimates a target price of $256, implying about 59% total upside over roughly 2.7 years, suggesting the stock may be undervalued if crypto market conditions stabilize and the company continues diversifying its revenue base.

Over the next year, performance will likely be driven by crypto price direction, which directly impacts trading volumes, along with continued growth in subscription and services revenue and expansion into newer products like derivatives, equities, and prediction markets, which could increase engagement and revenue per user.

At current levels, Coinbase appears positioned as a leveraged play on a stabilizing crypto market, with improving business diversification providing some downside support while still allowing for upside if market conditions strengthen.

How Much Upside Does COIN Stock Have From Here?

Investors can estimate Coinbase Global’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Coinbase Global in under 60 seconds with TIKR (It’s free) >>>