Key Takeaways:

- Arista is benefiting from strong demand for AI networking, and management said 2025 was “the year of validation” for its Arista 2.0 strategy as the company reached 150 million cumulative ports shipped and $9 billion in revenue.

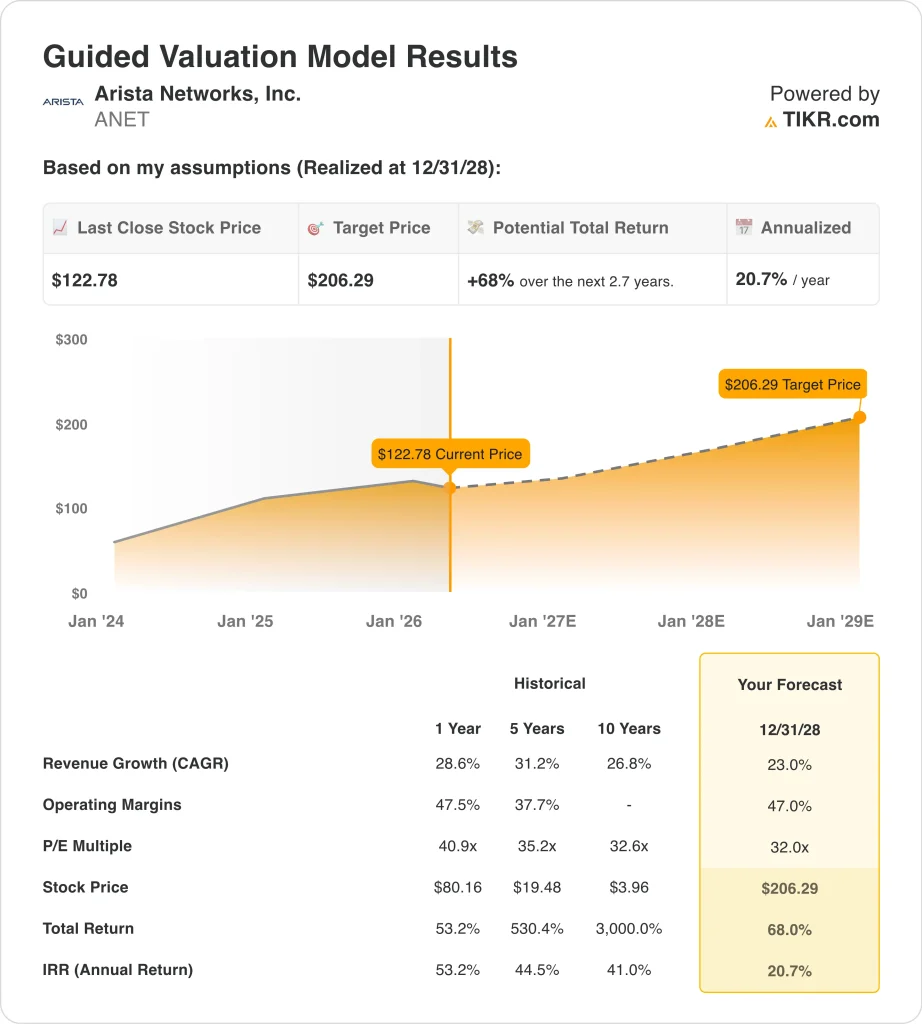

- ANET stock could reasonably reach $206 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 68% from today’s price of $123, with an annualized return of 20.7% over the next 2.7 years.

What Happened?

Arista Networks (ANET) moved higher after its February results because investors saw both a clean earnings beat and stronger AI demand. Arista forecast annual revenue above Wall Street estimates, and the stock jumped more than 17% in extended trading after the release. That reaction made sense because Arista sells high-speed switches and routers that sit inside large cloud and AI data centers.

The quarter itself was strong, and the guidance was better. Arista reported Q4 2025 revenue of $2.49 billion, up 28.9% year over year, while adjusted EPS came in at $0.82 versus the Reuters-cited consensus of $0.76. Management also guided for about $2.6 billion of Q1 2026 revenue, plus a non-GAAP operating margin of about 46%, which reinforced the view that AI demand is still accelerating.

Investors are also paying attention to Arista’s newer AI networking products because they speak directly to the next bottleneck in AI infrastructure. In March, the company launched the XPO MSA, a liquid-cooled pluggable optics module format for AI data centers, and said it would debut with live demonstrations at OFC 2026.

That said, the stock is not moving on enthusiasm alone. Arista still trades at premium multiples, so investors are weighing strong growth and margins against already high expectations and insider selling disclosures in March.

Here’s why Arista stock could continue to command that premium through 2028 if AI networking demand, cloud spending, and execution stay strong.

What the Model Says for ANET Stock

We analyzed the upside potential for Arista stock using valuation assumptions based on its leadership in AI and cloud networking, rising deferred revenue, and strong execution across data center, campus, and routing markets.

Based on estimates of 23.0% annual revenue growth, 47.0% operating margins, and a normalized P/E multiple of 32.0x, the model projects Arista stock could rise from $123 to $206 per share.

That would be a 68% total return, or a 20.7% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ANET stock:

1. Revenue Growth: 23%

Arista’s revenue growth has remained unusually strong for a company of its size. Revenue rose 28.6% in 2025 to $9.0 billion, and Q4 revenue increased 28.9% year over year to $2.49 billion. That growth reflects continued demand from cloud and AI customers that need faster Ethernet switching and routing at scale.

The quality of that growth also matters. Deferred revenue climbed to $5.6 billion at year-end 2025, up sharply from the prior year, which suggests strong order visibility and larger customer commitments. Arista is also broadening the story beyond core switching through campus products, AVA software, and newer optical designs tied to AI infrastructure.

Based on analysts’ consensus estimates, we use a 23.0% revenue growth forecast. That assumption lines up with Arista’s current AI and cloud momentum, but it still sits below its 2025 growth rate, so it builds in some moderation as the company scales.

2. Operating Margins: 47%

Arista already operates at elite margins, and that is one reason the stock gets premium treatment. Its LTM EBIT margin is 42.8%, and management said Q4 delivered a 47.5% operating margin while quarterly net income topped $1 billion for the first time. Those figures show that Arista is not just growing quickly, but also converting that growth into substantial profit.

The underlying model helps explain why margins remain so strong. Gross margin held at 64.1% for full-year 2025, even as Arista kept investing heavily in R&D, which reached $1.24 billion for the year. At the same time, operating income rose 31.0% to $3.86 billion, so scale is still helping the business absorb higher spending.

Based on analysts’ consensus estimates, we use a 47.0% operating margin assumption. That reflects Arista’s demonstrated operating leverage, its software-rich networking model, and its exposure to large AI deployments, while still staying close to the margin range management outlined for early 2026.

3. Exit P/E Multiple: 32x

Arista’s multiple is high, but it is not random. The stock trades at 34.7x forward earnings based on the market data provided, and that premium reflects the company’s AI positioning, strong balance sheet, and very high profitability. Investors are effectively paying up for a business that combines hardware growth with software-like margins and significant free cash flow.

The balance sheet supports that premium as well. Arista ended 2025 with $10.7 billion in cash and short-term investments and net cash of about $10.7 billion. It also generated $4.25 billion of free cash flow in 2025, which gives the company room to invest, buy back stock, and stay flexible if demand shifts.

Based on analysts’ consensus estimates, we maintain a 32.0x exit P/E multiple. That is slightly below the current forward multiple, and it reflects the idea that Arista can stay premium valued while still facing some normalization as expectations remain high.

Build your own Valuation Model to value any stock (It’s free!) >>>

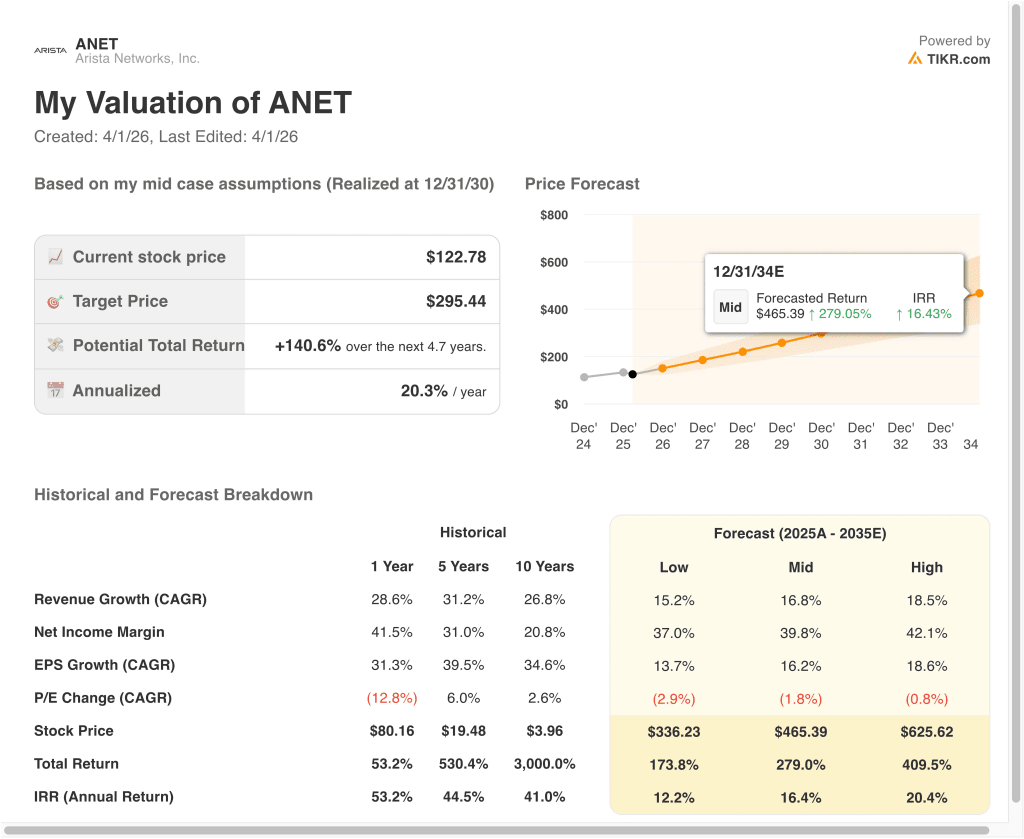

What Happens If Things Go Better or Worse?

Different scenarios for Arista stock through 2035 show varied outcomes based on AI infrastructure demand, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI data center spending cools, and valuation compresses faster → 12.2% annual returns

- Mid Case: Arista keeps scaling cloud and AI networking across large customer deployments → 16.4% annual returns

- High Case: Orders, margins, and AI network adoption remain exceptionally strong → 20.4% annual returns

Even in the conservative case, Arista stock offers positive returns supported by its strong AI networking position, high-margin operating model, and substantial free cash flow generation.

Arista’s next move will likely depend on whether it can keep converting AI enthusiasm into sustained bookings, revenue, and margins. The next major checkpoint is its expected Q1 2026 results in early May, when investors will look for confirmation that demand remains healthy. If management keeps executing across cloud, campus, and AI networking, the stock could remain volatile but still trade like a premium infrastructure name.

See what analysts think about ANET stock right now (Free with TIKR) >>>

Should You Invest in Arista Networks, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ANET, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ANET alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Arista Networks stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!