Key Takeaways:

- Circle is benefiting from rising stablecoin usage and payments adoption, helping drive strong revenue growth and renewed investor interest in 2026.

- CRCL stock is up 14.3% year-to-date, reflecting improving sentiment after strong earnings and continued expansion of its payments network.

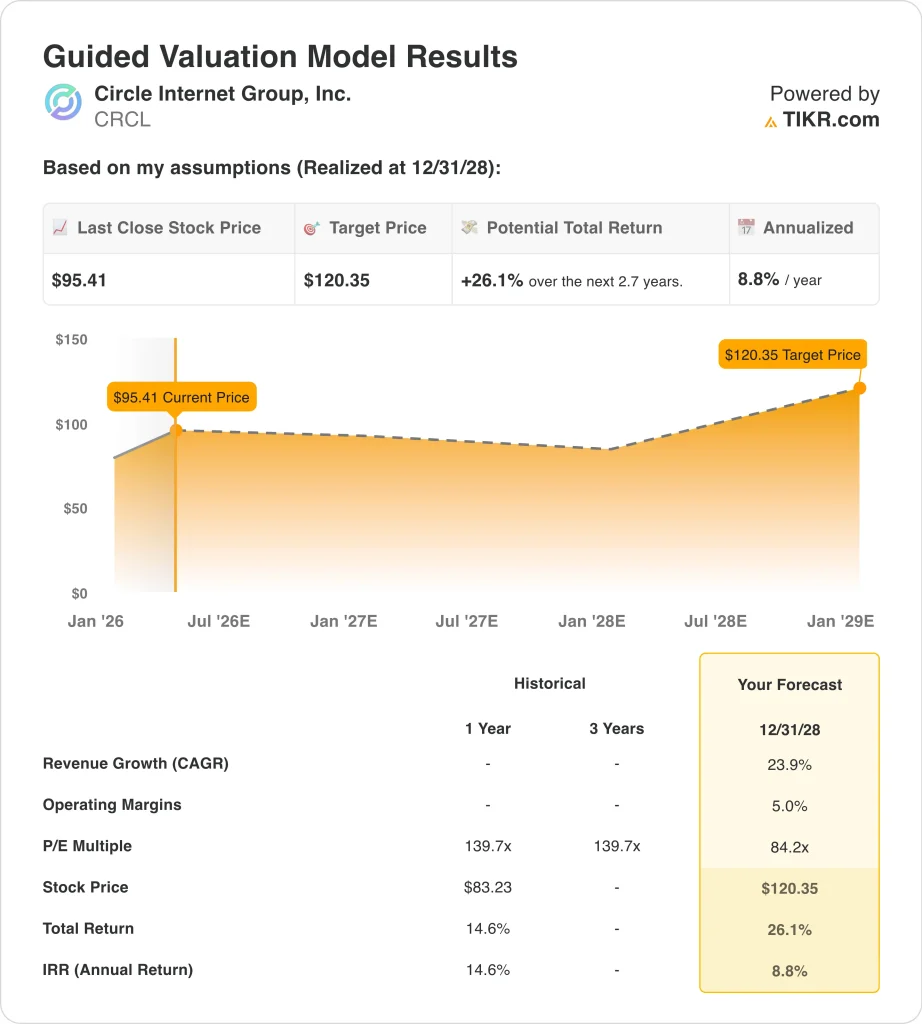

- Circle stock could reasonably reach $120 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 26.1% from today’s price of $95, with an annualized return of 8.8% over the next 2.7 years.

What Happened?

Circle Internet Group (CRCL) is gaining attention again as investors balance strong growth in stablecoins with rising regulatory uncertainty. The stock is up 14.3% year-to-date, showing a recovery after volatility earlier in the year.

That move reflects improving sentiment around Circle’s role in the global digital payments ecosystem. Investors are increasingly viewing the company as infrastructure rather than just a crypto-related name.

The company reported strong fourth-quarter 2025 results, with revenue and reserve income reaching $770 million, ahead of expectations. This was driven by higher USDC circulation and increased usage across trading and payments. Strong reserve income continues to be a major driver of profitability, especially as interest rates remain elevated. That dynamic has helped support the stock’s rebound in 2026.

However, regulatory headlines have also created pressure. Reports around a potential Clarity Act draft suggested limits on stablecoin yield payments, which caused Circle shares to pull back. This matters because stablecoin incentives and usage are closely tied to how products are regulated. Investors are still trying to understand how future rules could affect growth and monetization.

At the same time, Circle continues expanding globally through partnerships and product integrations. The company recently collaborated with Sasai Fintech to expand USDC access in Africa and added new capabilities to its payments network.

These moves support the long-term thesis that Circle is building a global payments layer. Here’s why Circle stock could remain volatile but trend with adoption, regulation clarity, and earnings consistency.

What the Model Says for CRCL Stock

We analyzed the upside potential for Circle stock based on its growth in stablecoin circulation, expanding payments infrastructure, and improving monetization potential.

Based on estimates of 23.9% annual revenue growth, 5.0% operating margins, and a normalized P/E multiple of 84.2, the model projects Circle stock could rise from $95 to $120 per share.

That would be a 26.1% total return, or a 8.8% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CRCL stock:

1. Revenue Growth: 23.9%

Circle’s revenue growth has been driven primarily by rising USDC adoption and reserve income. Total revenue increased from $1.6 billion in 2024 to $2.7 billion in 2025, representing 63.9% growth year over year. This reflects strong demand for digital dollar infrastructure across both crypto and traditional financial use cases. The company benefits directly when USDC circulation expands.

Another key driver is the expansion of Circle’s payments network. The company is positioning itself as a global settlement layer for remittances, cross-border payments, and enterprise financial flows. Partnerships like Sasai Fintech help extend reach into emerging markets, where digital dollar usage is growing rapidly. This supports long-term transaction volume growth beyond trading activity.

Circle is also diversifying its revenue sources beyond reserve income. New integrations and payment capabilities are designed to drive recurring usage across businesses and institutions. Based on analysts’ consensus estimates, we use a 23.9% revenue growth forecast, reflecting continued adoption but moderating from recent spikes.

2. Operating Margins: 5%

Circle’s profitability remains inconsistent despite strong revenue growth. The company reported a negative EBIT margin of -3.5% and a net loss in 2025, highlighting ongoing cost pressures. Much of this is tied to stock-based compensation and investments in scaling the platform. This explains why the stock still trades as a growth story rather than a profitability story.

However, there are signs of operating leverage emerging. As USDC circulation increases, reserve income scales with relatively lower incremental costs. This creates the potential for margin expansion if growth continues at a steady pace. The fourth quarter showed improved adjusted profitability, suggesting underlying momentum.

The key challenge is balancing growth investments with cost discipline. Operating expenses have increased significantly as Circle expands globally and builds infrastructure. Based on analysts’ consensus estimates, we assume a 5.0% operating margin, reflecting gradual improvement but still conservative relative to long-term potential.

3. Exit P/E Multiple: 84.2x

Circle trades at a premium valuation due to its exposure to stablecoin growth and digital payments infrastructure. The forward P/E multiple of 84.2 reflects expectations for strong long-term growth and market positioning. Investors are assigning a higher multiple because Circle operates in a rapidly evolving financial technology space. This valuation implies confidence in execution and adoption trends.

The company’s strategic positioning supports this premium. Circle is building a platform that connects traditional finance with blockchain-based payments, which could expand its addressable market significantly. Products like Circle Payments Network and USDC integrations strengthen its role in global finance. This narrative supports higher valuation multiples compared to traditional fintech companies.

At the same time, the multiple introduces risk. Regulatory uncertainty and earnings volatility can lead to sharp repricing if expectations change. Based on analysts’ consensus estimates, we maintain an 84.2 exit P/E multiple, assuming the market continues to value Circle as a high-growth infrastructure player.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

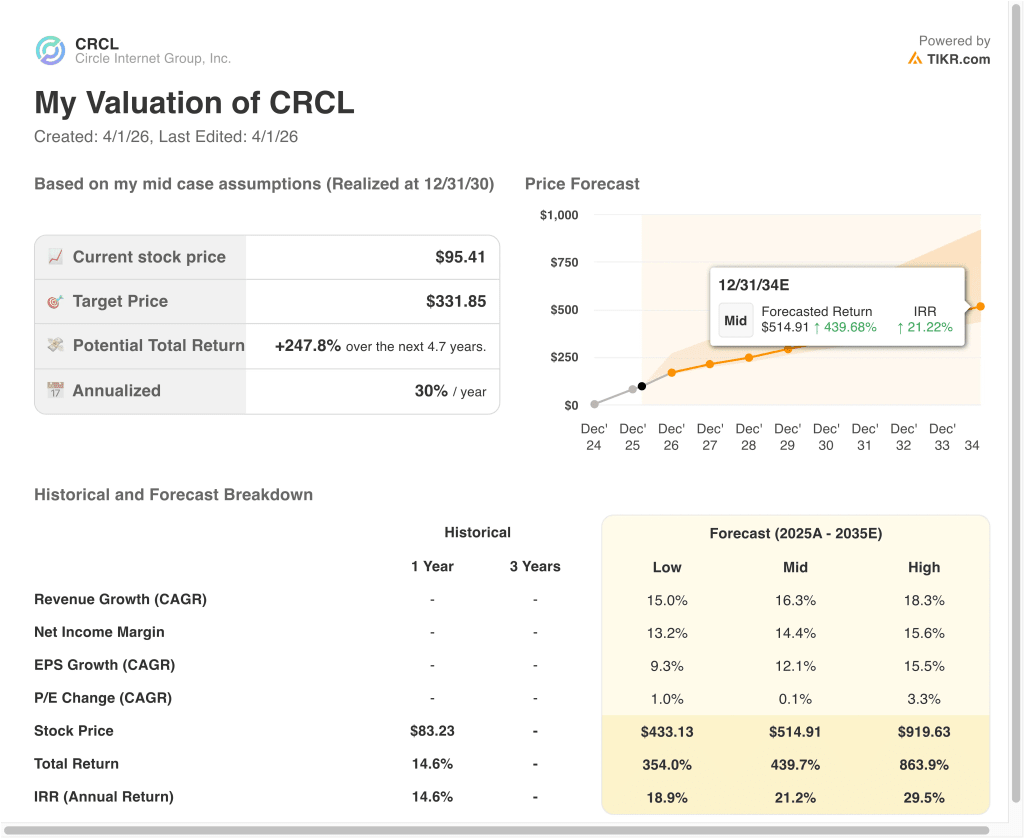

Different scenarios for CRCL stock through 2035 show varied outcomes based on stablecoin adoption, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Growth slows, and regulatory pressure limits monetization → 18.9% annual returns

- Mid Case: Circle scales USDC and payments network steadily → 21.2% annual returns

- High Case: Strong adoption and improving margins drive sustained expansion → 29.5% annual returns

Circle’s stock will likely continue to move with both adoption trends and policy developments. Stronger earnings consistency could support higher valuation stability over time. However, regulatory clarity remains a key variable that could influence how investors price the business going forward.

See what analysts think about VRT stock right now (Free with TIKR) >>>

Should You Invest in Circle Internet Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRCL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRCL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Circle Internet Group stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!