Key Takeaways:

- Chipotle is still growing sales and restaurant count, but weaker traffic and cautious 2026 guidance have pressured the stock.

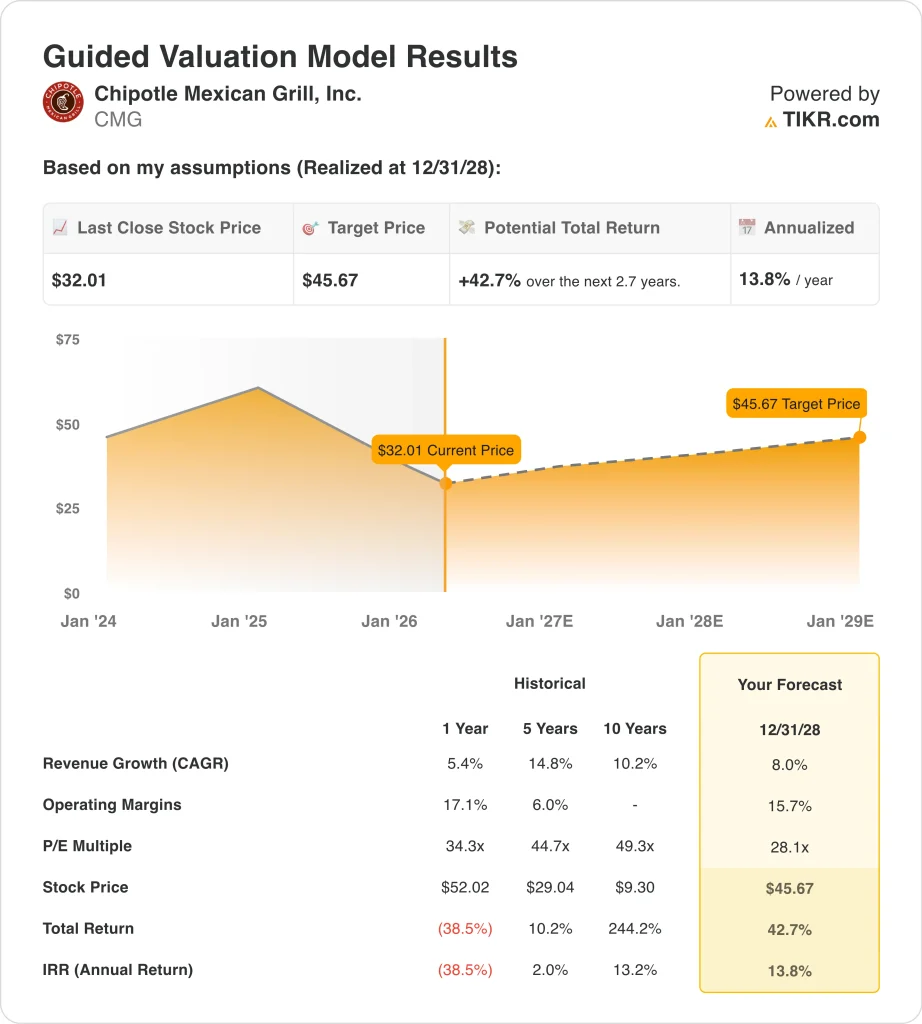

- CMG stock could reasonably reach $46 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 42.7% from today’s price of $32, with an annualized return of 13.8% over the next 2.7 years.

What Happened?

Chipotle Mexican Grill (CMG) is dealing with a very different market mood than it had a year ago. Investors are no longer focused only on unit growth and pricing power, because traffic has softened and management’s 2026 outlook came in below expectations.

Reuters reported that Chipotle guided fiscal 2026 same-store sales to be about flat, while analysts had expected growth, and that helped send the shares lower after the February results.

The market is also weighing external pressures on restaurant spending. Reuters said Chipotle and other restaurant stocks fell in March as oil prices surged, because higher fuel costs can squeeze consumers and lift delivery and input costs.

At the same time, Reuters noted that restaurants have remained a bright spot in U.S. job growth, which suggests demand has not collapsed, but consumers are still more selective and value-conscious than they were in earlier phases of the recovery.

Chipotle is still executing on long-term expansion, and that matters for valuation. The company finished 2025 with 4,056 restaurants and opened a record 334 company-owned locations during the year, including 257 with a Chipotlane, while management also announced first-quarter 2026 results will be released on April 29.

Here’s why Chipotle stock could recover through 2028 if traffic stabilizes, new stores keep compounding, and margins hold up better than the market now expects.

What the Model Says for Chipotle Stock

We analyzed the upside potential for Chipotle stock using valuation assumptions based on its steady unit expansion, resilient restaurant-level economics, and continued ability to generate cash even in a slower consumer environment.

Based on estimates of 8.0% annual revenue growth, 15.7% operating margins, and a normalized P/E multiple of 28.1x, the model projects Chipotle stock could rise from $32 to $46 per share.

That would be a 42.7% total return, or a 13.8% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CMG stock:

1. Revenue Growth: 8%

Chipotle’s top-line story is still solid, but it has clearly slowed. Revenue rose 5.4% in 2025 to $11.9 billion, and the company said that the increase was driven primarily by new restaurant openings rather than same-store sales growth. That matters because it shows the brand can still expand, but near-term demand at existing stores is softer than before.

Store growth remains the main engine. Chipotle opened a record 334 company-owned restaurants in 2025, and 257 of those included a Chipotlane, which management has long viewed as an important convenience and throughput driver. More units support revenue growth even when comps are muted, and they also widen the brand’s national footprint.

The challenge is traffic. Comparable restaurant sales declined 1.7% in 2025, and fourth-quarter comps fell 2.5%, so the business needs either a traffic recovery or stronger new-store productivity to reaccelerate.

Based on analysts’ consensus estimates, we use an 8.0% revenue growth forecast, which reflects continued expansion but also respects the slower demand backdrop management described for 2026.

2. Operating Margins: 15.7%

Chipotle remains a strong operator, but margins are no longer expanding the way they did in prior years. Operating margin was 16.9% in 2025, down from 17.3% in 2024, and fourth-quarter operating margin slipped to 14.1% from 14.6%. Reuters said part of the concern is that modest menu price hikes may not fully offset labor and food inflation in 2026.

Even so, the underlying model is still attractive. Restaurant-level operating margin was 25.4% for full-year 2025, and adjusted diluted EPS still rose in the quarter despite softer comps. That tells investors Chipotle still has meaningful pricing power, scale benefits, and disciplined cost control relative to many restaurant peers.

Margins will likely depend on whether traffic improves enough to absorb inflation and brand spending. Management said it remains confident in its 2026 strategic plan when it announced leadership transitions in January, but the market wants proof in the numbers.

Based on analysts’ consensus estimates, we use a 15.7% operating margin assumption, which is below the latest LTM level and therefore builds in some pressure rather than assuming a quick snapback.

3. Exit P/E Multiple: 28.1x

Chipotle still trades at a premium multiple, but that premium is lower than it used to be. The stock’s forward P/E is about 28.1x in the market data provided, while the historical valuation in the guided model was materially higher. That reset helps explain why a stock that has fallen can still show decent modeled returns without requiring aggressive assumptions.

Investors still pay up for Chipotle because the brand has a strong unit-growth runway, a differentiated menu position, and substantial cash generation. The company generated about $1.45 billion of free cash flow in 2025, even after capital spending rose to roughly $666 million. That combination of growth and cash flow helps support a premium relative to many restaurant names.

There is still valuation risk if traffic remains weak. Reuters also reported that Pershing Square dissolved its Chipotle position during the quarter, which reinforced the idea that some high-profile investors see better near-term opportunities elsewhere.

Based on analysts’ consensus estimates, we maintain a 28.1x exit P/E multiple, which reflects Chipotle’s quality but also a more restrained market view than in earlier years.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CMG stock over the next 12 months show varied outcomes based on traffic trends, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Traffic stays soft, and investors keep discounting slower same-store sales growth → 10.5% annual returns

- Mid Case: Chipotle keeps expanding restaurants, and demand gradually stabilizes → 14.2% annual returns

- High Case: Transactions recover faster, and margin pressure eases while sentiment improves → 17.7% annual returns

Looking ahead, CMG stock will likely be trading on a few specific questions. Investors will want to see whether traffic improves, whether menu pricing remains disciplined, and whether new restaurant openings keep supporting revenue growth.

The next earnings report on April 29 should be especially important because it will give the market a clearer read on consumer demand, margin stability, and whether Chipotle can regain momentum after the recent reset.

See what analysts think about CMG stock right now (Free with TIKR) >>>

Should You Invest in Chipotle Mexican Grill, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CMG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CMG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Chipotle Mexican Grill stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!