Key Stats for Arthur Gallagher Stock

- Past-Week Performance: -3.6%

- 52-Week Range: $195 to $351.2

- Current Price: $216.6

What Happened?

Arthur J. Gallagher & Co. (AJG), the world’s fourth-largest insurance brokerage and risk management firm, delivered its 23rd consecutive quarter of double-digit adjusted EBITDAC growth in Q4 2025, posting 30% growth in that metric alongside 6% full-year organic revenue growth, even as its stock trades at $216.58 — down 16.2% year-to-date and well below its 52-week high of $351.23.

On March 24, BMO Capital Markets upgraded AJG to “outperform” from “market perform” and raised its price target to $278 from $275, arguing the market is pricing in organic growth misses while failing to credit the productivity tailwinds from AI deployment across the firm’s brokerage, claims, and back-office operations over the next 12 to 24 months.

The firm’s combined adjusted EBITDAC reached $4.782 billion in 2025 on $13.8 billion in adjusted revenue, with underlying margins expanding 70 basis points on a comparable basis and every point of the 6% organic growth rate supported by positive net new business spread across property casualty retail, wholesale, reinsurance, and employee benefits — a breadth of performance that stands in contrast to peer Brown & Brown, which reported organic revenue contraction of 2.8% in the same quarter.

Furthermore, on March 18, CFO Douglas Howell stated at the firm’s quarterly investor meeting that “AI can accelerate analysis, accelerate revenue growth and create efficiency, but it does not negotiate tailored covered, advocate claims, assume professional liability, or even take responsibility for risk decisions,” directly anchoring the firm’s AI investment thesis to its $1.5 billion annual technology budget and the 40,000 employees already using AI tools generating 1.6 million self-serve prompts per month.

Gallagher’s $10 billion M&A war chest, $160 million in AssuredPartners synergies targeted by year-end 2026 scaling to $300 million by early 2028, an active pipeline of nearly 40 merger targets representing $250 million in annualized revenue, and a $1.5 billion share repurchase authorization — of which $250 million was deployed opportunistically in Q1 2026 — position the firm to compound its two-pronged organic-plus-acquisition growth strategy well into the decade while its smaller competitors lack the capital and data infrastructure to match its AI deployment pace.

Wall Street’s Take on AJG Stock

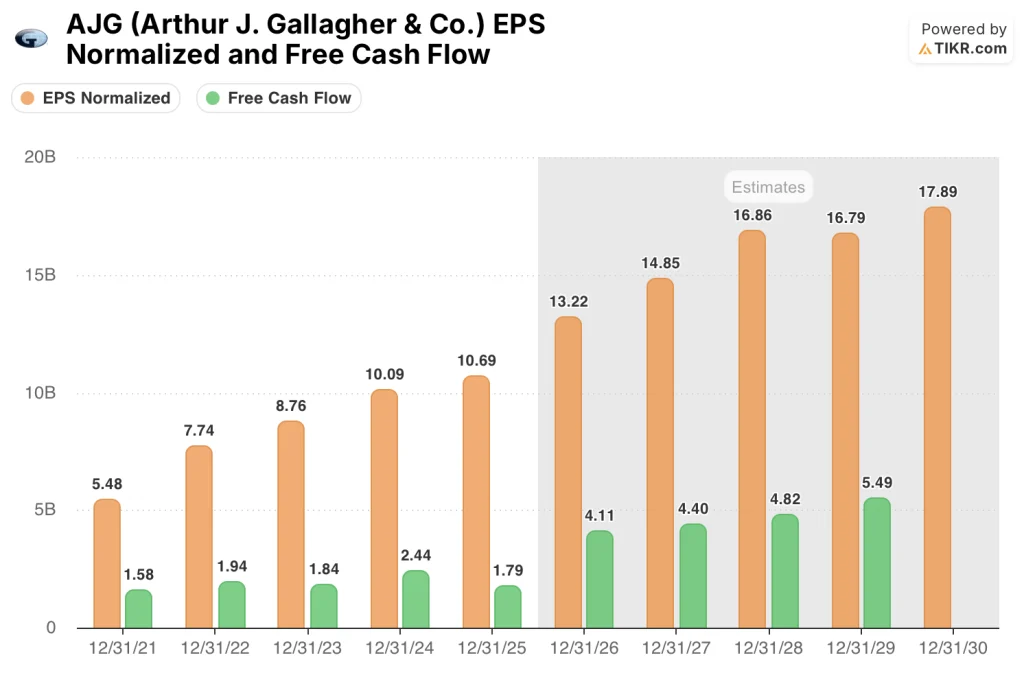

BMO’s upgrade and $278 price target directly connect to the same AI productivity thesis Gallagher management has been building toward since 2004, when the firm began standardizing its processes — and as TIKR estimates 23.7% normalized EPS growth to $13.22 in 2026, that thesis is now showing up in the forward numbers.

The fundamental case rests on two concurrent acceleration vectors: AssuredPartners synergies scaling from $160 million by year-end to $300 million by early 2028, and free cash flow expanding from $1.79 billion in 2025 to an estimated $4.11 billion in 2026, a 130.5% surge as the drag from holding acquisition capital dissipates.

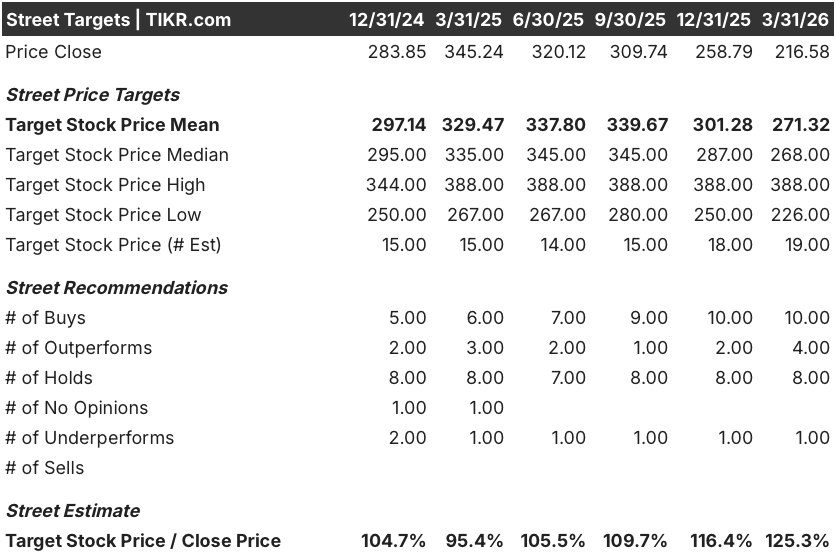

A Wall Street growing increasingly constructive on the name — 10 buys, 4 outperforms, 8 holds, and 1 underperform across 23 analysts, with a mean price target of $271.32 implying 25.3% upside from $216.58 — reflects the broadening consensus that the AI disruption discount embedded in the stock is disproportionate to the actual exposure.

The spread between the Street’s low target of $226 and high of $388 captures the binary embedded in the AI narrative: the low anchors on organic growth misses as pricing softens in property lines, while the high reflects full credit for the estimated 600 basis points of long-run EBITDA margin upside CFO Howell outlined at the March 18 investor meeting.

What Does the Valuation Model Say?

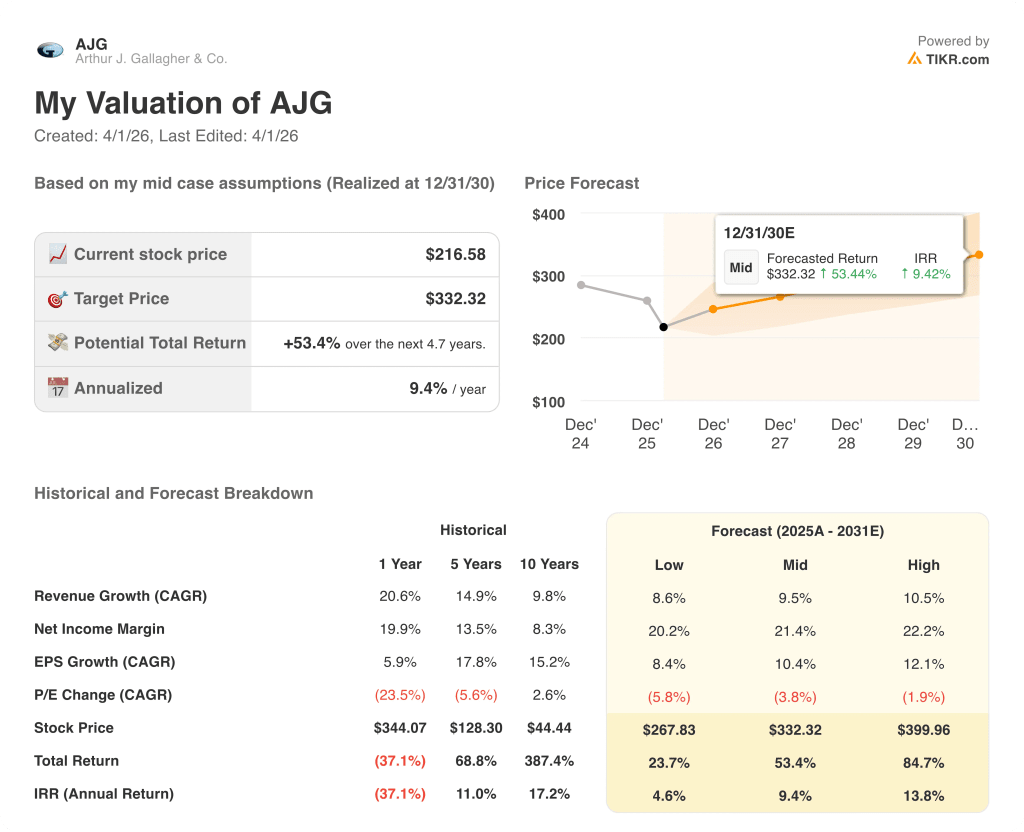

The TIKR mid-case model targets $332.32 by December 2030, embedding a 9.5% revenue CAGR and 21.4% net income margin expansion, directly supported by the AssuredPartners integration, $10 billion in M&A capacity, and AI-driven back-office efficiency already measurable in the firm’s 60,000 annual process workflows.

At $216.58, AJG trades at approximately 16.4x TIKR’s 2026 normalized EPS estimate of $13.22 — a meaningful discount to its own 5-year historical forward P/E of roughly 28-30x, at a moment when EPS growth is actually accelerating from 5.9% in 2025 to an estimated 23.7% in 2026, marking this stock as deeply undervalued relative to its own earnings trajectory.

The TIKR model’s core 9.5% revenue CAGR assumption is grounded in Gallagher’s confirmed 5.5% full-year 2026 organic growth target, 7 acquisitions already closed year-to-date, and a pipeline of nearly 40 merger targets representing $250 million in annualized revenue — all disclosed at the March 18 investor meeting; TIKR’s mid-case price target of $332.32 reflects this compounding growth path at a still-compressed multiple.

CFO Douglas Howell’s disclosure that 40,000 employees are executing 1.6 million AI prompts monthly confirms this is an operational transformation already in motion, not a management aspiration — the productivity gains are being measured in minutes per workflow across 60,000 annual processes, not projected in strategy decks.

The one development that breaks TIKR’s model is a sustained casualty pricing reversal: if the 7-8% casualty rate increases underpinning 2026 organic guidance compress toward flat, Gallagher’s brokerage segment commission growth decelerates and the $13.22 EPS estimate moves out of reach.

The April 2026 Q1 earnings call is the first concrete checkpoint: watch the brokerage segment organic growth figure against the 4.5% estimate and any updated casualty renewal premium data, since both directly validate whether the 5.5% full-year organic target and TIKR’s 2026 EPS estimate of $13.22 remain intact.

Should You Invest in Arthur J. Gallagher & Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AJG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Arthur J. Gallagher & Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AJG stock on TIKR for Free →