Key Stats for WEC Energy Stock

- 52-Week Range: $100.6 to $118.5

- Current Price: $117.6

- Street High Target: $140

What Happened?

WEC Energy Group (WEC), a regulated electric and natural gas utility serving 4.7 million customers across Wisconsin, Illinois, Michigan, and Minnesota, is executing a $37.5 billion capital buildout through 2030 anchored to 3.9 gigawatts of new data center demand, with shares trading at $117.58 near their 52-week high of $118.53.

The Q4 2025 earnings release confirmed the catalyst: WEC posted FY2025 adjusted earnings per share of $5.27, up 8% year-over-year, beating the LSEG consensus of $1.40 on a Q4 basis, while simultaneously announcing a $1 billion capital plan increase tied to Microsoft’s decision to expand its Mount Pleasant, Wisconsin data center campus by 15 additional buildings.

Underlying that expansion, WEC’s Wisconsin segment, the company’s core regulated utility business and primary earnings engine, delivered net income of $1.05 billion in FY2025, up 22.2% year-over-year, while total retail electric deliveries in the state rose 2.2% and large commercial and industrial demand is forecast to grow 5.8% in 2026 alone as data center load ramps.

In January, WEC’s Board approved a 6.7% dividend increase to an annualized $3.81 per share, the company’s 23rd consecutive annual dividend raise, and WEC also priced $400 million in 4.75% senior notes on February 23 to support its accelerating infrastructure financing needs.

Scott Lauber, President and CEO, stated on the Q4 earnings call that “we are projecting long-term earnings per share growth of 7% to 8% a year on a compound annual basis between 2026 and 2030,” with acceleration to the upper half of that range beginning in 2028 as Oak Creek, Paris, and renewable projects enter service.

WEC’s competitive position through 2030 rests on three converging forces: the $12.6 billion renewable buildout adding 6,500 megawatts of generation capacity, a Vantage Data Centers site at Port Washington with near-term demand of 1.3 gigawatts and long-term potential of 3.5 gigawatts, and a proposed Wisconsin rate case filing in April covering forward test years 2027 and 2028 that will formalize data center customers paying their full allocated share of infrastructure costs.

Wall Street’s Take on WEC Stock

The $37.5 billion capital cycle driving WEC’s data center buildout maps directly onto the TIKR consensus EPS ramp, with normalized EPS forecast to grow from $5.27 in 2025 to $6.50 by 2028, a 7.3% CAGR that matches management’s stated 7%–8% long-term growth target.

Underpinning that trajectory, TIKR estimates EBITDA margin expanding from 40.1% in 2025 to 48.7% by 2028 as the Wisconsin segment, which already delivered 22.2% net income growth in 2025, absorbs the fixed-cost leverage of the Oak Creek combustion turbine and Paris RICE generation projects entering service.

Wall Street’s current positioning reflects cautious optimism rather than conviction: 7 buys, 1 outperform, 10 holds, and 1 sell across 19 analysts produce a mean price target of $123.09, implying only 4.7% upside from $117.58, with analysts anchored to near-term Illinois regulatory drag rather than the 2028 acceleration WEC’s management has explicitly guided toward.

The target spread tells a more revealing story, with the high target of $140.00 representing analysts pricing in the full Microsoft and Vantage data center ramp, while the $108.00 floor reflects a scenario where the Illinois rate case and settlement bill credits structurally pressure FFO-to-debt metrics beyond management’s current guidance.

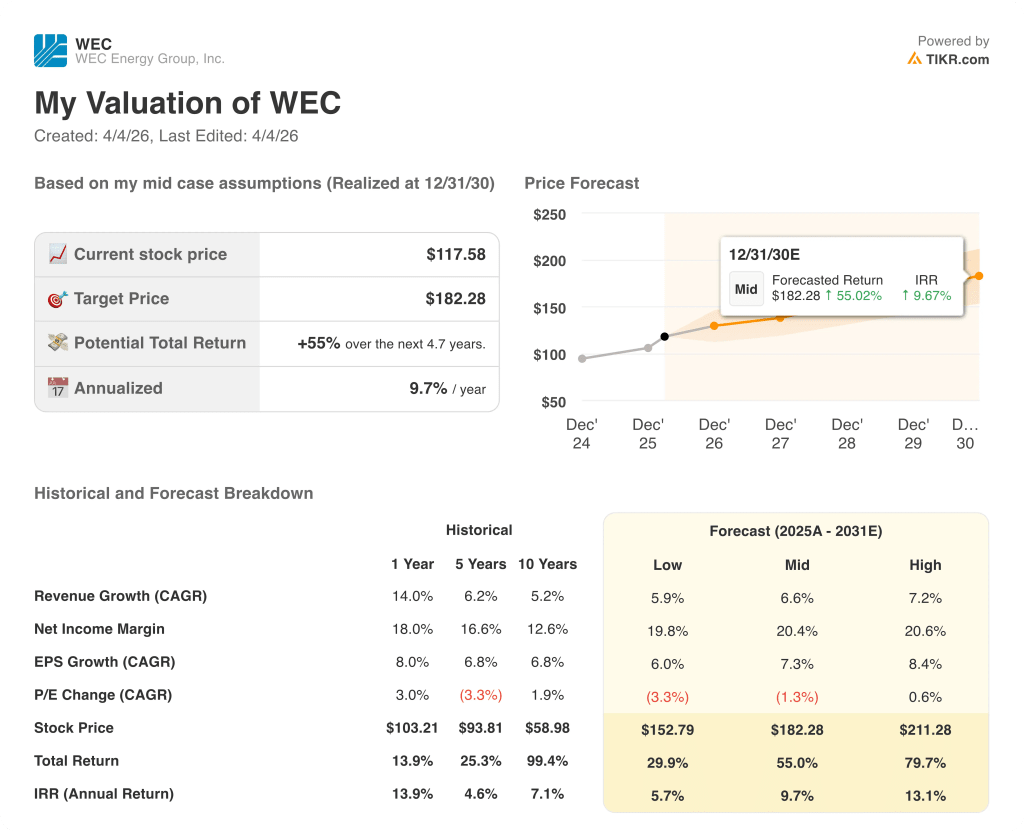

What Does the Valuation Model Say?

The TIKR mid-case model, assuming 6.6% revenue CAGR and 20.4% net income margins through 2030, produces a price target of $182.28, a 55% total return at a 9.7% annualized IRR, justified by 3.9 gigawatts of contracted demand growth that no peer utility in WEC’s Midwest footprint can currently match at equivalent regulatory visibility.

At 21x forward earnings on FY2026E normalized EPS of $5.60, WEC stock trades in line with its own historical forward multiple despite carrying a materially superior growth outlook than the prior five-year period, when EPS grew at 6.8% annually with no comparable demand catalyst, making WEC stock fairly valued on near-term consensus but meaningfully undervalued against the 2028 inflection point that management has dated and quantified.

The operational justification for that inflection is already in motion: Wisconsin’s large commercial and industrial segment is forecast to grow 5.8% in 2026 alone, Vantage broke ground in December 2025, and the TIKR model’s $182.28 target assumes only mid-case EPS of $7.62 by 2030, a number management’s own 7%–8% CAGR guidance from the $5.27 base implies is achievable without any upside from Point Beach replacement generation or additional hyperscaler signings.

CEO Scott Lauber’s statement on the February 5 earnings call that growth will “accelerate to the upper half of the range starting in 2028” is the signal the TIKR model is pricing: this is not a cheap utility, it is a utility whose growth rate is being systematically underpriced by a consensus still anchored to the pre-data center version of WEC.

The primary risk is Illinois: if the Commerce Commission rejects or materially modifies the proposed $205 million settlement terms or the 2027 forward rate case, the $130 million prospective rate base reduction could deepen, directly pressuring the normalized EPS base the entire model rests on.

WEC’s April 2026 Wisconsin general rate case filing, covering forward test years 2027 and 2028, is the single most important near-term datapoint: the allocated cost structure for data center customers will either validate or challenge management’s claim that hyperscalers absorb their full share of the $37.5 billion capital plan without burdening residential rates.

Should You Invest in WEC Energy Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WEC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track WEC Energy Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WEC stock on TIKR for Free →