Key Stats for Royal Gold Stock

- Current Price: $262.63

- Target Price (High Case): $402.83

- Street Target: $330.09

- Potential Total Return: +53.4%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

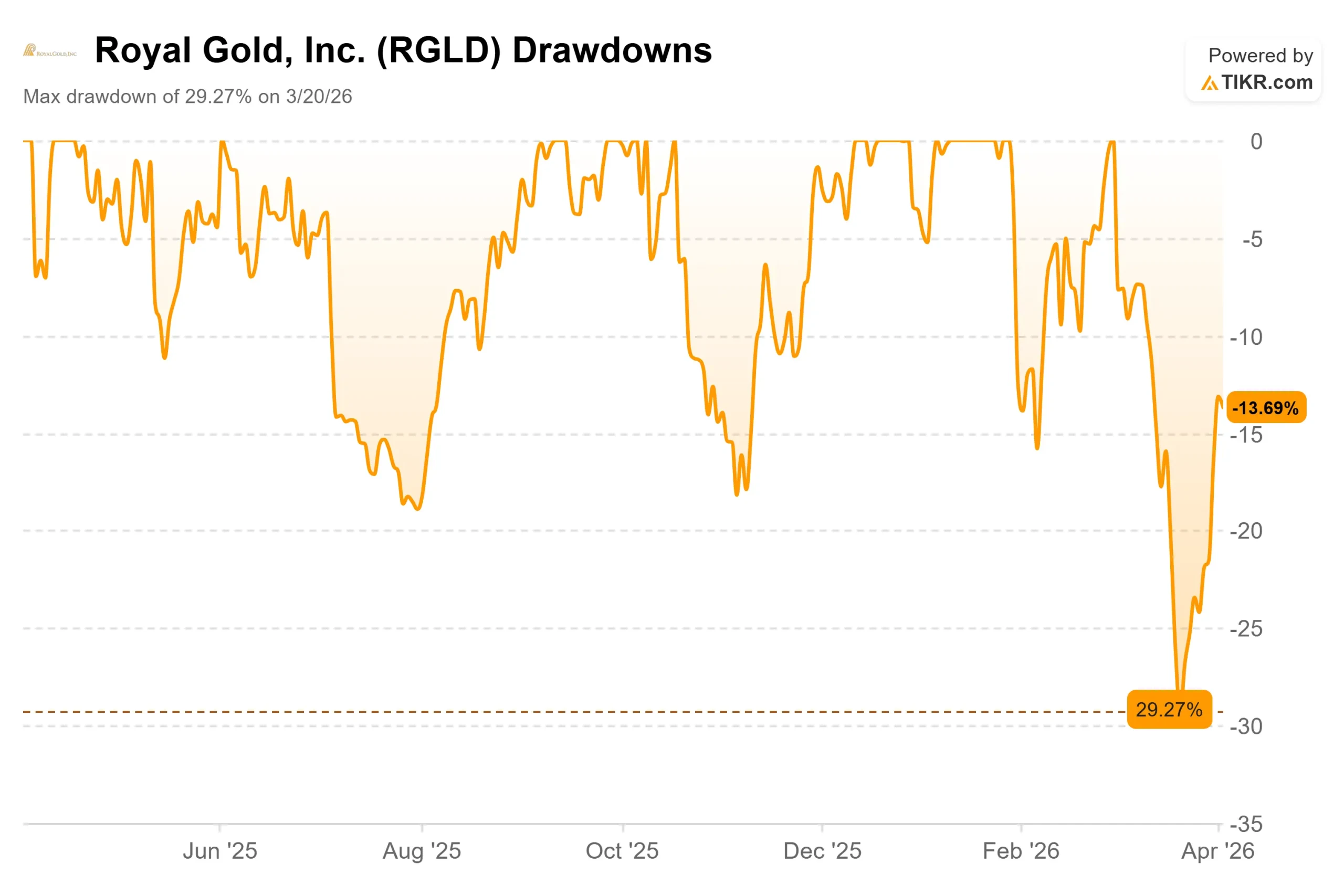

Royal Gold (RGLD) hit a 52-week high of $306.25 before falling nearly 30% to a March 20 low as gold prices pulled back and volatility swept through precious metals equities.

The stock has since recovered to $262.63, still 14% below that peak, and investors are asking whether the discount is an opportunity or a warning.

Bulls point to record full-year 2025 revenue of $1.03 billion, a portfolio reshaped by more than $5 billion in acquisitions, and a first-ever 5-year outlook released at the March 31 Investor Day projecting approximately 17% revenue growth through 2031 without any new deals required.

The core question is whether the market has correctly repriced Royal Gold for post-acquisition integration complexity, or whether it is simply slow to recognize a materially better company.

At the Investor Day, Alistair Baker, Senior Vice President of Investor Relations and Business Development, stated directly: “We believe there is a meaningful disconnect between the intrinsic value of our business and how it’s currently reflected in the market.”

See historical and forward estimates for Royal Gold stock (It’s free!) >>>

Is Royal Gold Undervalued Today?

Royal Gold trades at 13.19x NTM EV/EBITDA (enterprise value divided by forward EBITDA) and 20.45x NTM P/E.

Every major peer is more expensive: Wheaton Precious Metals at 16.98x, Franco-Nevada at 19.25x, Osisko Gold Royalties at 17.98x, and Triple Flag Precious Metals at 16.76x. The peer mean sits at 17.74x, putting Royal Gold at roughly a 26% discount despite managing 80 producing assets across 360 properties with just 39 employees.

The gap has a clear origin.

The Sandstorm acquisition closed in October 2025 as an all-share deal, bringing temporary dilution and a large retail shareholder base that was mostly liquidated post-close.

Baker noted at the Investor Day that institutional active holders have grown their positions by over 20% since closing.

The growth pipeline is specific and named. The 5-year outlook targets 430,000 to 480,000 gold-equivalent ounces (GEOs, meaning the full precious metals portfolio expressed in gold terms) annually by 2030. Robertson at Cortez begins production in 2027.

The Hod Maden royalty starts contributing in 2028. Kinross’s Great Bear in Ontario targets first production around the end of 2029. Warintza in Ecuador delivers its first gold in 2030.

Overlaid on those are expansions already funded by operating partners: a $900 million MMG program at Khoemacau in Botswana expected to raise Royal Gold’s silver deliveries by nearly 35%, and Platreef in South Africa, where Ivanhoe Mines achieved first ore processing in late 2025 and is ramping Phase 2 this year.

Three risks are real.

First, the Q4 earnings miss, even attributed to M&A accounting noise, created a credibility overhang that has not fully cleared.

Second, the Hod Maden joint venture (Royal Gold’s 30% ownership stake in the mine itself, separate from the royalty) is excluded entirely from the 5-year outlook because SSR Mining’s strategic review has delayed any conversion to a royalty structure. Heissenbuttel said at the Investor Day that the situation “might change what we’re able to achieve” on that timeline.

Third, roughly 80% of 2026 revenue is expected from gold alone, per Raffield’s Investor Day guidance, leaving the company directly exposed to any sustained metal price decline.

The structural offset is the business model itself.

As Heissenbuttel noted at the Investor Day, adjusted EBITDA runs at approximately 95% of net revenue, and TIKR data shows LTM EBITDA margins of 82.3%. Royalty and stream costs are contractually fixed at the mine level, meaning inflation, tariffs, and supply chain disruptions that hurt operating miners do not affect Royal Gold’s economics.

One asset not in the 5-year guidance also deserves attention.

Royal Gold holds a 1.6% gross smelter royalty (calculated on gross metal revenue before processing deductions) over Barrick’s Fourmile deposit in Nevada. Raffield described preliminary estimates of 600,000 to 750,000 ounces per year over a 25-year mine life, and said the royalty alone has the potential to generate 9,500 to 12,000 royalty ounces per year for roughly 25 years. Barrick is spending more than $200 million on Fourmile in 2026 alone.

See how Royal Gold performs against its peers in TIKR (It’s free!) >>>

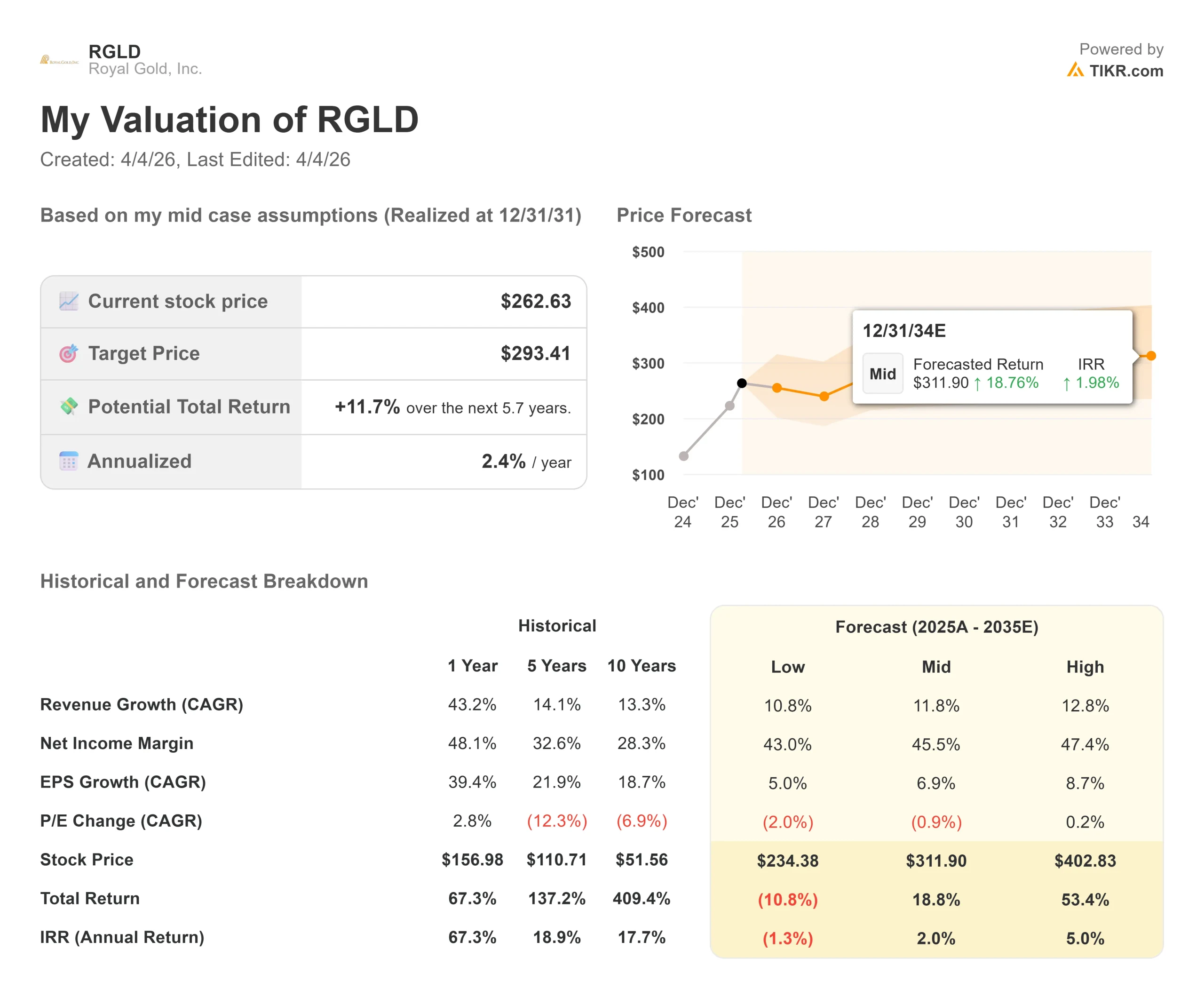

TIKR Advanced Model Analysis

- Current Price: $262.63

- Target Price (High Case): $402.83

- Potential Total Return: +53.4%

- Annualized IRR: 5.00% / year

See analysts’ growth forecasts and price targets for Royal Gold stock (It’s free!) >>>

The TIKR model runs three scenarios through December 31, 2034. The high case is used here because the named 5-year pipeline, Fourmile optionality, and current gold pricing all support assumptions at the upper end of the range. The mid-case IRR of 1.98% does not capture the growth trajectory management outlined at the Investor Day.

The high case targets $402.83, implying +53.4% total return and a 5.00% annualized IRR. The two primary revenue drivers are new production from Robertson, Great Bear, the Hod Maden royalty, and Warintza across the five-year window, and expansion of existing streams at Khoemacau and Platreef, where operating partners are funding the capital entirely. The margin driver is scaled on a near-zero incremental cost base, with high-case net income margins reaching 47.4%.

The downside is real but bounded. TIKR’s low case prices the stock at $234.38, a -10.8% total return and -1.3% annualized IRR through 12/31/34, reflecting a sustained gold price decline with no multiple expansion.

Conclusion: Watch Mount Milligan gold deliveries at the Q1 2026 earnings report on May 6. Centerra extended the mine life to 2045 and is permitting tailings capacity well beyond that. If production holds within the guided 140,000 to 155,000 ounces for 2026, it confirms that Royal Gold’s largest single revenue asset is performing as described and removes one of the few remaining near-term execution risks.

Royal Gold is a structurally superior gold business trading at a structurally inferior multiple. The March 31 Investor Day gave investors the clearest roadmap yet for why that should change.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Royal Gold?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Royal Gold, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Royal Gold alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Royal Gold on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!