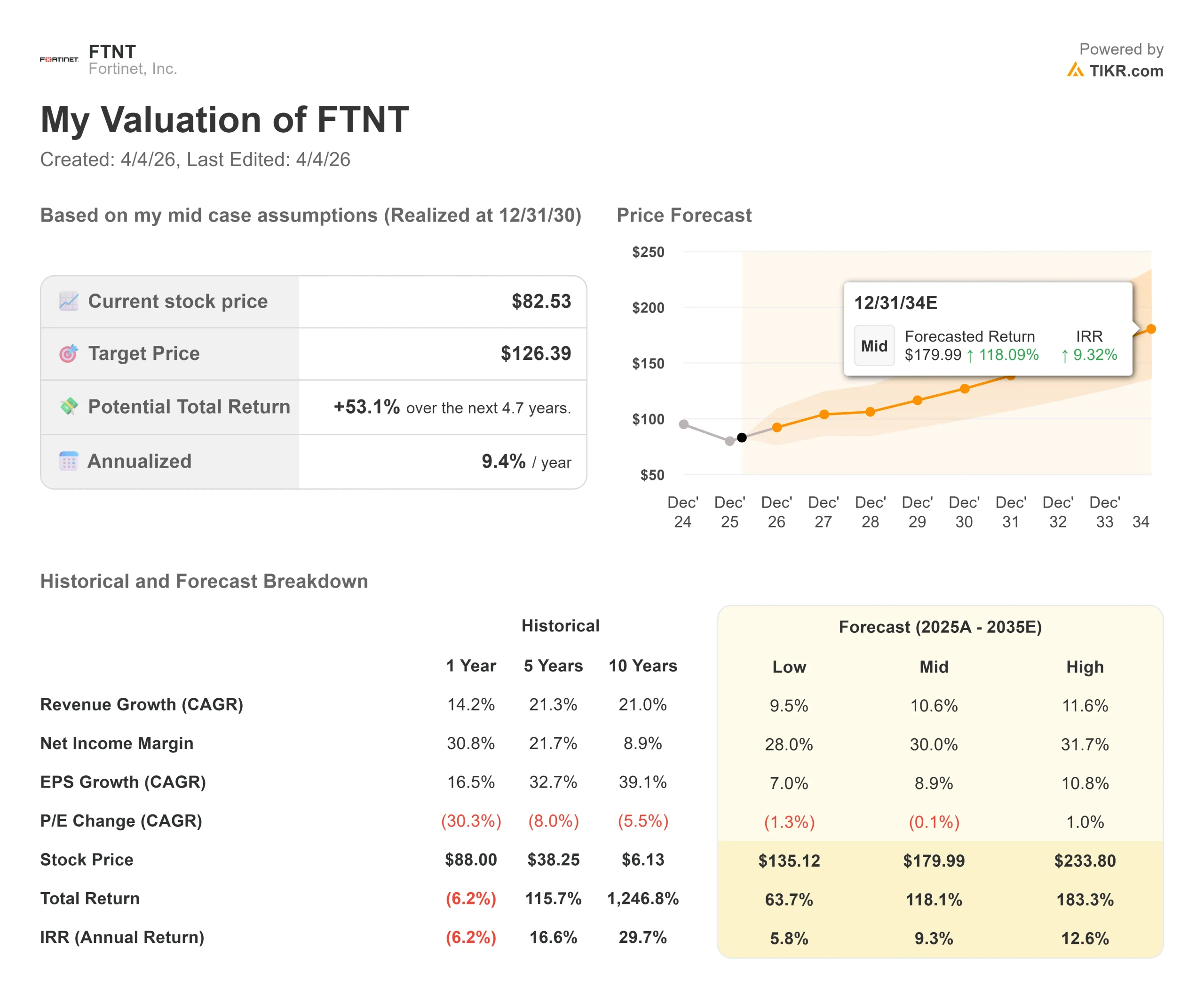

Key Stats for Fortinet Stock

- Current Price: $82.53

- Target Price (Mid): $126.39

- Street Target: $89.12

- Potential Total Return: +53.1%

- Annualized IRR: 9.40% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

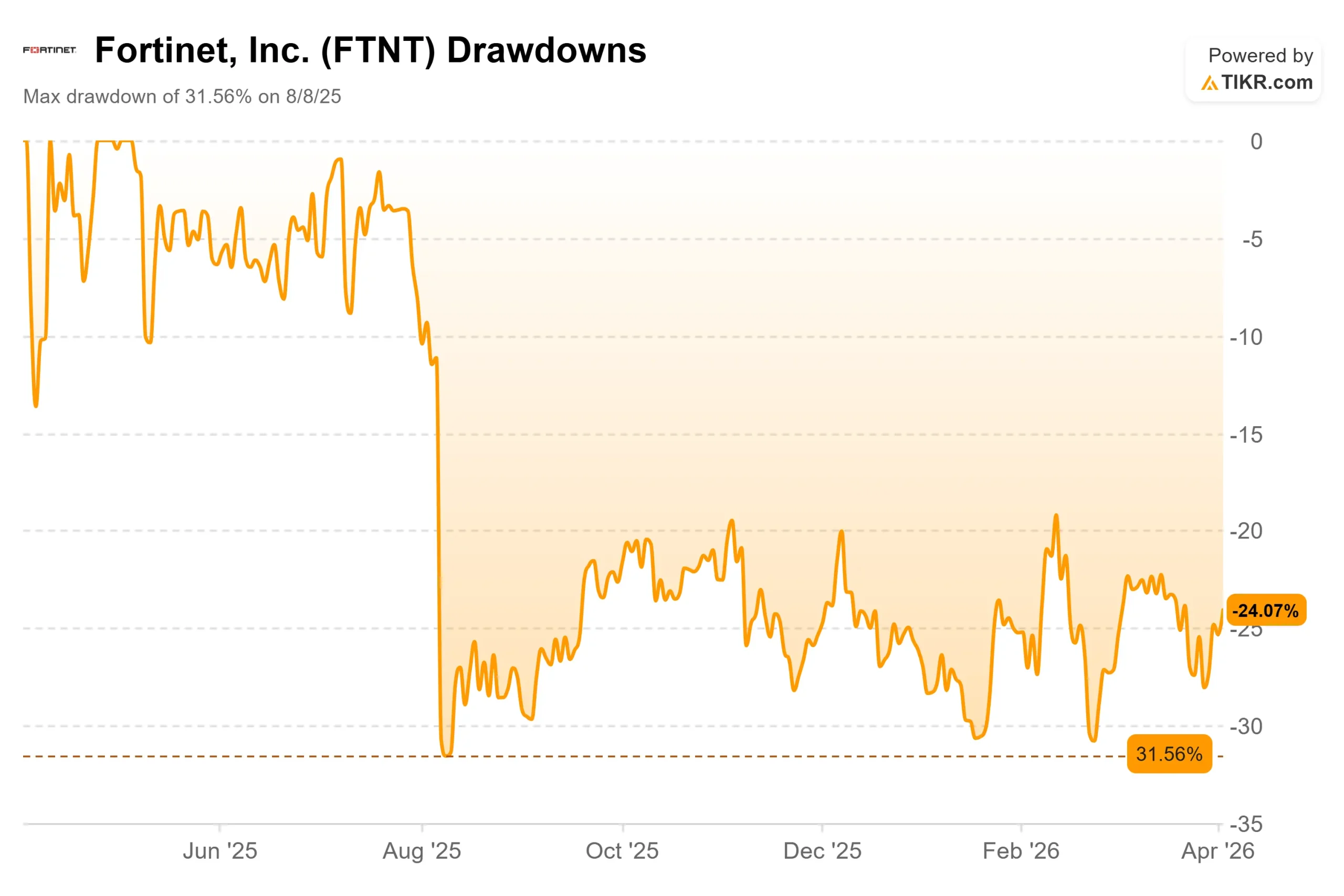

Fortinet (FTNT) is stuck between a strong business and a struggling stock. Shares sit at $82.53, down roughly 24% from their 52-week high of $109.33 and below the 200-day moving average.

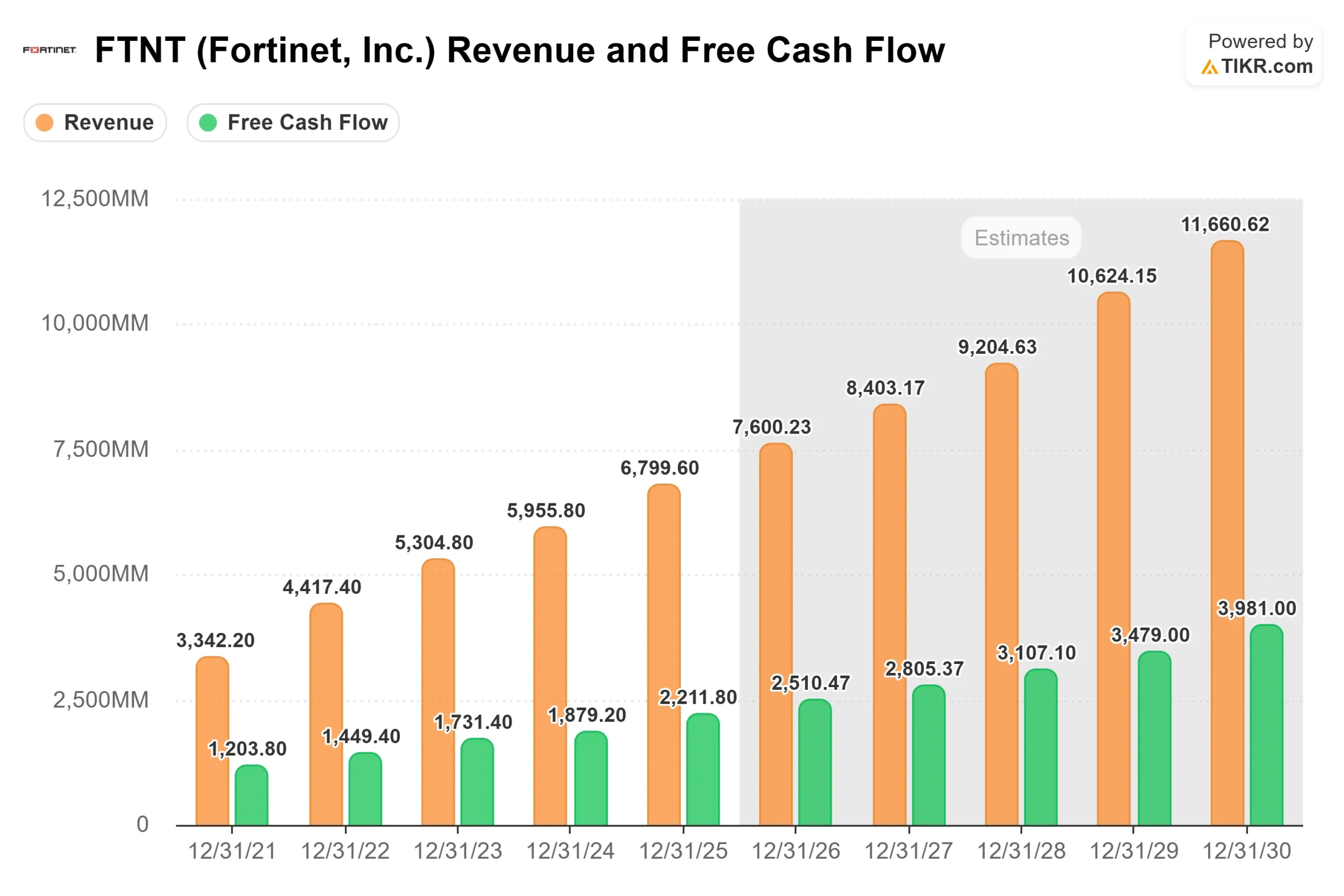

At the same time, full-year 2025 free cash flow hit a record $2.21 billion, and the company beat earnings estimates in all four quarters of 2025.

Bulls argue Fortinet is cheap relative to its cash generation and that Unified SASE (secure access service edge, which combines networking and security into a single cloud-delivered platform) is only beginning to scale.

Bears point to the appliance-heavy installed base as a structural risk as security spending migrates toward pure-cloud vendors, and to Q1 2026 operating margin guidance of 30-32%, a step down from Q4 2025’s 37.3%, as evidence that near-term earnings pressure is real.

The unresolved question: can SASE momentum compound fast enough to re-rate the stock?

“We are pleased with our strong finish to the year, highlighted by an excellent fourth quarter driven by broad-based demand across our portfolio, which drove billings above the high end of our guidance,” said Ken Xie, Founder, Chairman, and Chief Executive Officer of Fortinet, in the Q4 2025 earnings release.

On March 10, Fortinet launched FortiOS 8.0 at its Accelerate 2026 conference in Las Vegas, adding AI-driven security controls, next-generation SASE capabilities, and quantum-safe cryptography across its Security Fabric platform.

The stock gained just 0.47% that day. That muted reaction to a substantive product launch is exactly why this stock is frustrating to own and potentially interesting to buy.

And just this week, Fortinet hosted an APAC Demo Day on April 1, showcasing Unified SASE in live technical scenarios. Presenters walked through how FortiSASE blocks employees from leaking sensitive data to generative AI platforms like ChatGPT and DeepSeek in real time, using data loss prevention (DLP, meaning automated content inspection that detects and blocks unauthorized data transfers).

One demo intercepted a credit card data upload in under a second. Another enforced keyword-based policy on prompts sent to ChatGPT while permitting others.

This is the AI-era security use case enterprises are actively asking for, and Fortinet is shipping it now.

See historical and forward estimates for Fortinet stock (It’s free!) >>>

Is Fortinet Undervalued Today?

At 7.70x NTM EV/Revenue and 21.19x NTM EV/EBITDA, Fortinet trades at a clear discount to its cybersecurity peers. Palo Alto Networks (PANW) trades at 10.10x NTM EV/Revenue and 33.09x NTM EV/EBITDA. CrowdStrike (CRWD) trades at 16.40x NTM EV/Revenue and 55.54x NTM EV/EBITDA.

Both peers are growing faster, which justifies some premium. But the scale of Fortinet’s discount is wider than the growth differential alone explains.

The free cash flow picture is the more compelling argument.

LTM free cash flow stands at $1.783 billion, placing the stock at 24.32x NTM market cap to free cash flow. That is a different conversation from a high-multiple growth stock. The board added $1.0 billion to the share repurchase authorization in February, bringing the total to $10.25 billion through February 28, 2027, per the Q4 2025 earnings release.

Management also reaffirmed full-year 2026 revenue guidance of $7.5-$7.7 billion, implying approximately 12% growth at the midpoint.

The SASE acceleration is the growth argument.

According to the Q4 2025 earnings call, Unified SASE billings grew 40% in the quarter and now represent 27% of total billings. FortiSASE ARR, the cloud-delivered component, grew over 90%. CFO Christiane Ohlgart noted that service pricing is structured as a percentage of product list price, meaning recent product revenue acceleration is a leading indicator for service revenue growth in the second half of 2026.

That pull-through lag means the Q1 margin step-down may not be the run rate.

On the Q4 earnings call, Ken Xie stated that Fortinet has “probably doubled the total addressable market in the SASE market with Sovereign SASE,” an on-premises deployment option that lets regulated enterprises and government customers host SASE infrastructure inside their own data centers.

Pure-cloud competitors like Zscaler cannot serve this segment.

At the April 1 APAC Demo Day, Product Marketing Director Alexandra Mehat noted that FortiGuard Labs has applied AI and machine learning to threat detection for over 15 years, with more than 500 AI patents, creating a threat intelligence depth that newer entrants cannot replicate quickly.

See how Fortinet performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $82.53

- Target Price (Mid): $126.39

- Potential Total Return: +53.1%

- Annualized IRR: 9.40% / year

See analysts’ growth forecasts and price targets for Fortinet stock (It’s free!) >>>

The TIKR mid-case model assumes a 10.6% revenue CAGR through December 31, 2030, and a 30.0% net income margin. The two revenue drivers are continued Unified SASE adoption across the installed base and product revenue growth from FortiOS upgrade cycles. Management’s full-year 2026 guidance of $7.5-$7.7 billion is consistent with this trajectory. The primary risk is macro-driven delay in enterprise refresh decisions, which would slow the service revenue pull-through that underpins margin expansion.

The high case (11.6% CAGR, 31.7% net income margin) produces $233.80 by 12/31/30, representing a 183.3% total return and a 12.6% annualized IRR. That requires FortiSASE enterprise penetration to accelerate well beyond the current 16% of large enterprise customers reported on the Q4 2025 earnings call. The low case (9.5% CAGR, 28.0% net income margin) still produces $135.12 by 12/31/30 and a 63.7% total return, suggesting the cash flow base provides a reasonable downside floor.

The mid-case 9.40% annualized IRR is not a screaming buy. But for a business generating $1.783 billion in LTM free cash flow, trading 24% below its 52-week high with its fastest-growing segment at 40% billings growth, the setup is more interesting than 29 Hold ratings suggest.

Conclusion: The single metric to watch at Fortinet’s Q1 2026 earnings call on May 6 is Unified SASE billings growth. In Q4 2025, it grew 40%. Sustaining above 35% signals the acceleration is durable. A sharp drop below 30% gives the bears their clearest evidence yet. That number, more than EPS or headline revenue, sets FTNT’s re-rating timeline.

Fortinet is a cash-generating platform business trading 24% below its 52-week high, with its fastest-growing segment still accelerating and its newest OS embedding it deeper into every AI-era security workflow enterprises are building.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Fortinet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Fortinet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fortinet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Fortinet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!