Key Stats for HCA Stock

- 52-Week Range: $314.4 to $556.5

- Current Price: $471.8

- Street High Target: $

What Happened?

HCA Healthcare (HCA), the largest for-profit hospital operator in the United States with 190 hospitals and approximately 47 million annual patient encounters, closed 2025 with its 19th consecutive quarter of volume growth and a record $6.78B in net income, even as it prepared investors for a $600M-$900M headwind from the expiration of Affordable Care Act enhanced premium tax credits in 2026.

On its Q4 2025 earnings report, HCA reported quarterly adjusted EPS of $8.01, beating the $7.46 analyst consensus by 7.4%, and raised its 2026 full-year EPS guidance to $29.10-$31.50, above the $29.46 analyst average, anchored to a $400M cost-savings resiliency program using AI, advanced analytics, and shared-service platform optimization across revenue integrity, asset throughput, and fixed and variable cost reduction.

The Q4 beat reflected 2.4% same-facility admission growth, a 2.9% increase in net revenue per equivalent admission, and an 80 basis point improvement in adjusted EBITDA margin, driven by continued mix shift toward higher-acuity services including cardiac, transplant, and trauma programs that command stronger reimbursement rates from commercial and Medicare payers.

CFO Mike Marks stated on the Q4 2025 earnings call that “this peak season is the most profitable peak in FedEx history” — correction: Marks stated that “our program has 4 key areas of focus: revenue integrity, variable and fixed cost efficiencies and capacity management,” and that HCA has “confidence that we’ll be able to execute on this $400 million of incremental cost savings in ’26 versus ’25.”

HCA’s board simultaneously authorized a new $10B share repurchase program, with management indicating the majority would be completed in 2026, while the company increased its quarterly dividend from $0.72 to $0.78 per share and guided for $12B-$13B in operating cash flow for the year.

Wall Street’s Take on HCA Stock

The ACA headwind is real and well-documented, but the market is treating it as a structural impairment when HCA’s own guidance frames it as a one-year absorption event, offset by $400M in structural savings and a buyback large enough to retire roughly 4% of the float.

HCA has fallen roughly 15% from its 52-week high of $556.52 as investors repriced the stock on ACA exchange enrollment uncertainty, Medicaid supplemental payment delays, and physician cost inflation running at high single-digit growth rates — three headwinds that are real but all management-guided and quantified, not open-ended.

HCA’s EBITDA margin has held strong 19-20% for five consecutive years, and TIKR estimates it holds at 20.4% through 2026 despite absorbing a $600M-$900M ACA exchange headwind, underwritten by the $400M resiliency program and sustained commercial rate increases in the mid-single-digit range.

That margin resilience compounds directly into earnings: TIKR estimates normalized EPS of $30.33 in 2026, growing at a 12.0% CAGR to $42.83 by 2029, anchored to 2%-3% annual volume growth across 43 high-population-growth markets and the $7B capital pipeline converting network investment into market share gains.

Thirteen analysts rate HCA a buy and two outperform against nine holds and 1 sell, with a mean price target of $543.05 implying 15.1% upside from current levels, as Wall Street awaits the April 24 Q1 2026 call for the first hard data on ACA effectuation rates and Florida Medicaid supplemental payment approval status.

The $425 bear case requires the ACA headwind to breach $900M, the resiliency program to underdeliver, and Florida grandfathering to go unapproved through year-end; the $635 bull case requires none of those — just execution on the guidance HCA has already set and approval of the pending state programs that management flagged are in active CMS review.

HCA Healthcare’s Margins Hold the Line

HCA’s gross margin has expanded from 38.3% in 2021 to 41.5% in 2025, a 320 basis point improvement over four years driven by deliberate mix shift toward higher-acuity commercial and Medicare services, including cardiac, transplant, and trauma programs that carry structurally higher reimbursement rates than the general medical and surgical volume the company has been shedding.

Operating income grew 13.4% in 2025 to $11.97B, lifting operating margins to 15.8% as revenue growth of 7.1% outpaced cost expansion for the third consecutive year, confirming that HCA’s shared-service platforms in revenue cycle and supply chain are generating sustainable operating leverage at scale.

Revenue has compounded at 6.7% annually over five years to $75.60B in 2025, with TIKR estimating $78.66B in 2026 and $93.43B by 2029 as the $7B capital pipeline in inpatient capacity and outpatient access points drives continued market share gains across HCA’s 43 high-growth domestic markets.

What Does the Valuation Model Say?

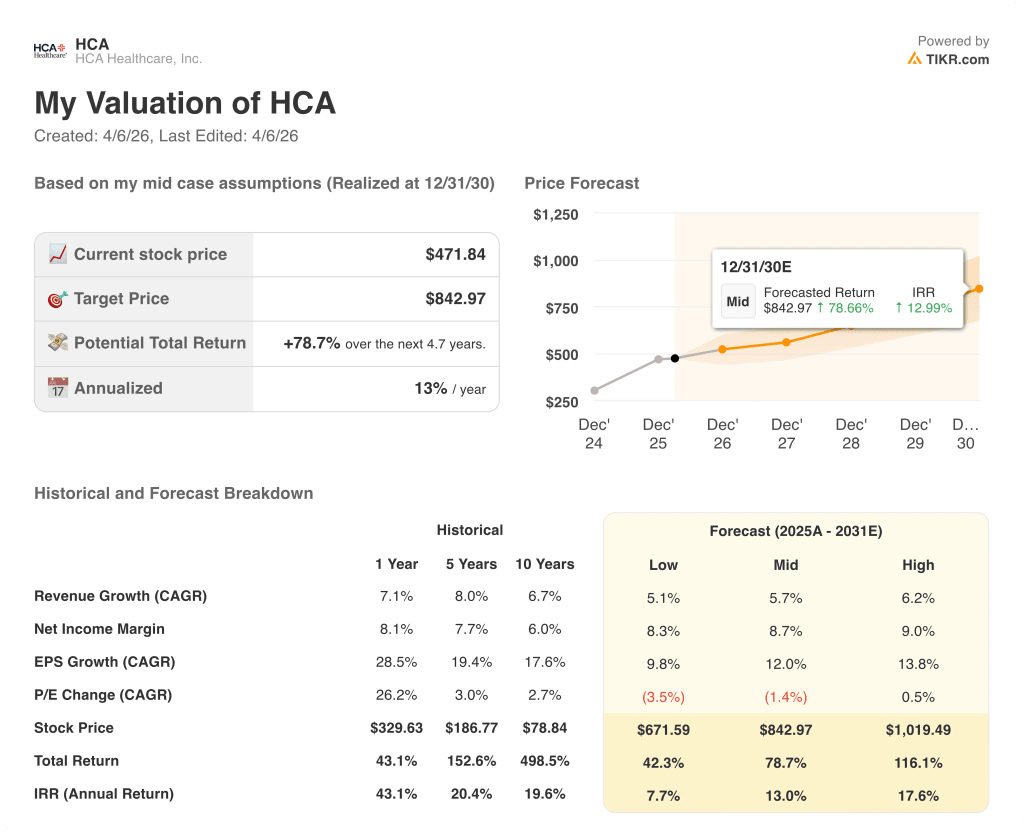

Trading at roughly 15.6x forward earnings against a 12.0% normalized EPS CAGR, HCA trades at a discount to its own five-year average multiple, leaving HCA undervalued relative to the earnings trajectory the TIKR model prices in through 2030.

The TIKR mid-case target of $842.97 assumes a 5.7% revenue CAGR and 12.0% EPS CAGR through December 2030, with EBITDA margins holding above 20% as the resiliency program offsets physician cost inflation and the ACA volume drag normalizes in 2027.

HCA appears undervalued at current levels, with the TIKR model implying 78.7% total return over 4.7 years at a 13.0% IRR while the stock sits 15% below its 52-week high of $556.52.

Physician cost inflation, running at high single-digit growth in 2026 primarily in anesthesiology and radiology, is the line item to watch: if hospital-based specialist costs re-accelerate toward the 20% pace seen in 2024, the resiliency program’s fixed-cost savings would be partially offset before flowing to EBITDA.

The April 24 Q1 2026 earnings call is the first hard data point on ACA effectuation rates, metal-tier shifts from silver to bronze, and Florida Medicaid supplemental payment approval status, any one of which could move the $600M-$900M headwind estimate materially in either direction.

Should You Invest in HCA Healthcare, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HCA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HCA Healthcare, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HCA stock on TIKR for Free →