Key Stats for Biogen Stock

- Current Price: $177.34

- Street Target (Mean): $207.33

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Biogen (BIIB) stock fell roughly 4% the day the deal was announced and has not recovered. That reaction captures the market’s read precisely: a $5.6 billion check at a 140% premium to spot price, for a company whose flagship drug posted a revenue decline in 2025.

Bulls argue that CEO Christopher Viehbacher spent more than a year studying Apellis and waited deliberately until the company’s forecasts came back in line with reality before engaging. Bears say SYFOVRE (pegcetacoplan injection), the geographic atrophy drug accounting for roughly 85% of Apellis revenue, is a slow-growth asset in a difficult market, and the premium is hard to justify on near-term numbers alone.

Biogen agreed to pay $41 per share in cash, more than double Apellis’s prior close, plus a non-transferable CVR (contingent value right, meaning a conditional future payment) of up to $4 per share tied to SYFOVRE global sales milestones.

On the call, Viehbacher laid out four acquisition criteria: post-Phase III assets, strategic fit within immunology and rare disease, no balance sheet stretch, and a price that still creates shareholder value.

“We’ve looked at a whole range of companies,” he said.

“You can pretty much assume that anything under $5 billion of market cap, we have looked at, and we believe that this was the best opportunity that really fits strategically with Biogen.”

CFO Robin Kramer confirmed the deal is expected to become increasingly accretive to non-GAAP diluted EPS beginning in 2027, with full debt repayment by year-end 2027.

According to Biogen’s press release, EMPAVELI and SYFOVRE generated $689 million in combined 2025 net product revenue and are expected to grow at a mid-to-high teens rate through at least 2028.

The deal is expected to close in Q2 2026, subject to regulatory approval.

See historical and forward estimates for Biogen stock (It’s free!) >>>

Is Biogen Undervalued Today?

The strategic logic here is easier to defend than the price. SYFOVRE held approximately 60% of the U.S. geographic atrophy market in 2025, but its $587 million in revenue represented a 4% decline from the prior year, a sign of pricing and payer pressure that Biogen now inherits.

Alisha Alaimo, Biogen’s President of North America, acknowledged on the call that around 50% of patients in the geographic atrophy space discontinue treatment, a structural challenge she described as “a leaky bucket” requiring sustained patient education investment.

Viehbacher said Biogen is “probably slightly conservative” relative to street estimates on SYFOVRE, flagging explicitly that no near-term inflection is expected.

The more compelling part of the deal is EMPAVELI. The drug received FDA approval in 2025 for two rare kidney diseases, C3 glomerulopathy (C3G) and primary immune complex membranoproliferative glomerulonephritis (IC-MPGN), conditions where abnormal immune deposits progressively damage the kidneys, and its launch is still in early stages.

Stifel noted that if Apellis reaches analyst consensus of roughly $1.5 billion in 2030 revenue, Biogen will have paid approximately 3.5 times that figure, calling it “not crazy at all” while flagging that the target requires a durable SYFOVRE re-acceleration and EMPAVELI exceeding $600 million in annual sales.

The deeper rationale is felzartamab, a CD38-targeting antibody (a molecule designed to clear disease-causing immune cells in the kidney) currently in Phase 3 trials for three kidney diseases, with the first readout expected in the first half of 2027.

Viehbacher stated explicitly on the call that felzartamab revenue was not included in the acquisition valuation model, and the kidney optionality comes at no additional cost.

The Apellis commercial team of roughly 350 people, with established nephrology center relationships, gives Biogen a foundation for that launch it could not build organically before the readout. BMO Capital Markets wrote that successful execution “could start to meaningfully change how investors think about the revenue growth story” for Biogen.

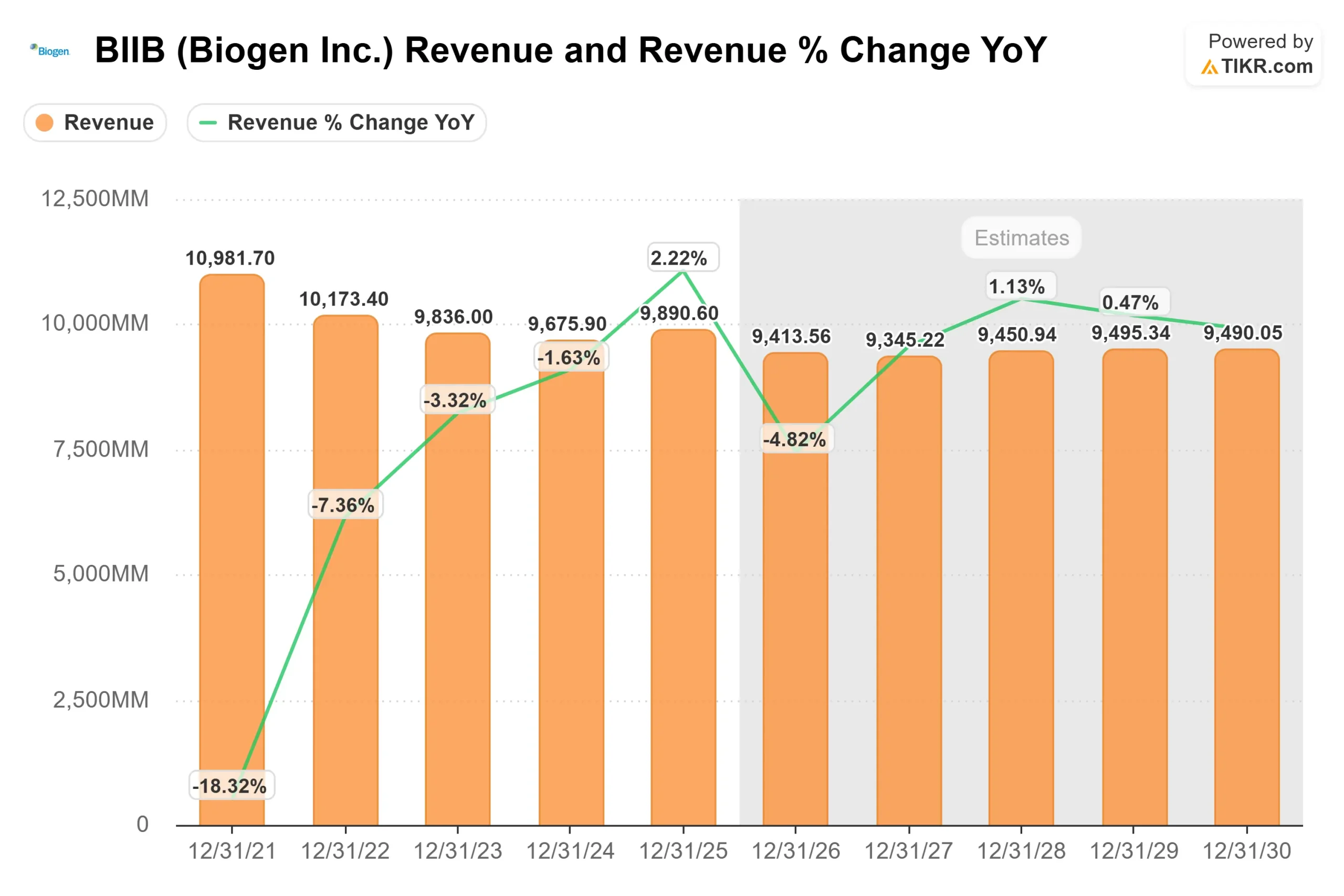

BIIB trades at 8.82x NTM EV/EBITDA and 11.28x NTM P/E, at a discount to Amgen (AMGN) at 11.00x EV/EBITDA and Gilead Sciences (GILD) at 11.16x EV/EBITDA. That discount reflects the market pricing in near-term revenue headwinds: Biogen’s 2026 standalone guidance implies a mid-single-digit revenue decline, consistent with the TIKR forward estimate of $9,413.56 million for 2026.

See how Biogen performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

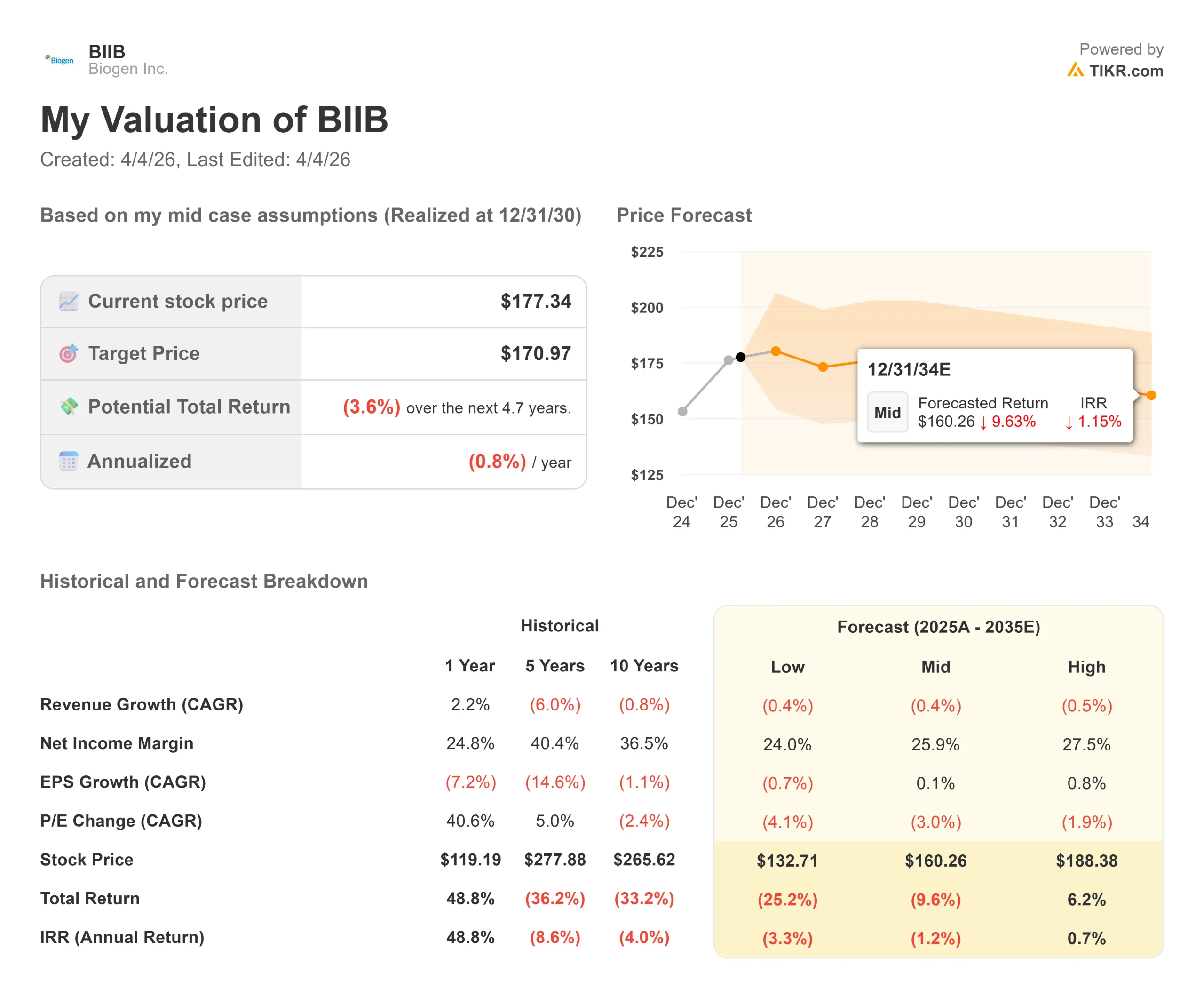

- Current Price: $177.34

- TIKR Mid-Case Target: $170.97

- TIKR Mid-Case Total Return: (3.6%)

- TIKR Mid-Case IRR: (0.8%) / year

See analysts’ growth forecasts and price targets for Biogen stock (It’s free!) >>>

The TIKR mid-case model points to $170.97 by 12/31/30, a total return of (3.6%) and an IRR of (0.8%) per year from $177.34. The model was built before the Apellis acquisition closed, so it does not incorporate SYFOVRE or EMPAVELI revenue. That matters: if those products deliver mid-to-high teens growth through 2028 as management projects, the model’s revenue assumptions are conservative.

Two drivers could push BIIB above the mid-case: EMPAVELI’s rare kidney disease ramp and a successful felzartamab Phase 3 readout in H1 2027. The margin driver is cost discipline. Kramer flagged integration savings within the Apellis commercial organization on the call. The primary risk is SYFOVRE. A continued revenue decline in geographic atrophy, or the entry of a better-tolerated competitor, would validate the mid-case or push lower. The model’s message is clear: this is not a stock that rewards passive holding at today’s price. Execution is required.

Conclusion: Watch Biogen’s Q1 2026 earnings report for updated full-year guidance incorporating Apellis. Any upward revision above Biogen’s previously implied standalone 2026 range would be the first signal that the combined revenue trajectory is ahead of plan. The thesis in a sentence: Biogen paid a full price, the TIKR model shows a slightly negative return at current levels without the Apellis contribution, but the nephrology infrastructure and unpriced felzartamab optionality give this deal a second act that the market has not yet credited.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Biogen?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Biogen, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Biogen alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!