Key Stats for Delta Air Lines Stock

- Current Price: $66.76

- Street Mean Target: $79.73

- Potential Upside to Street Target: +19.4%

- TIKR High Case Target: $111.40

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

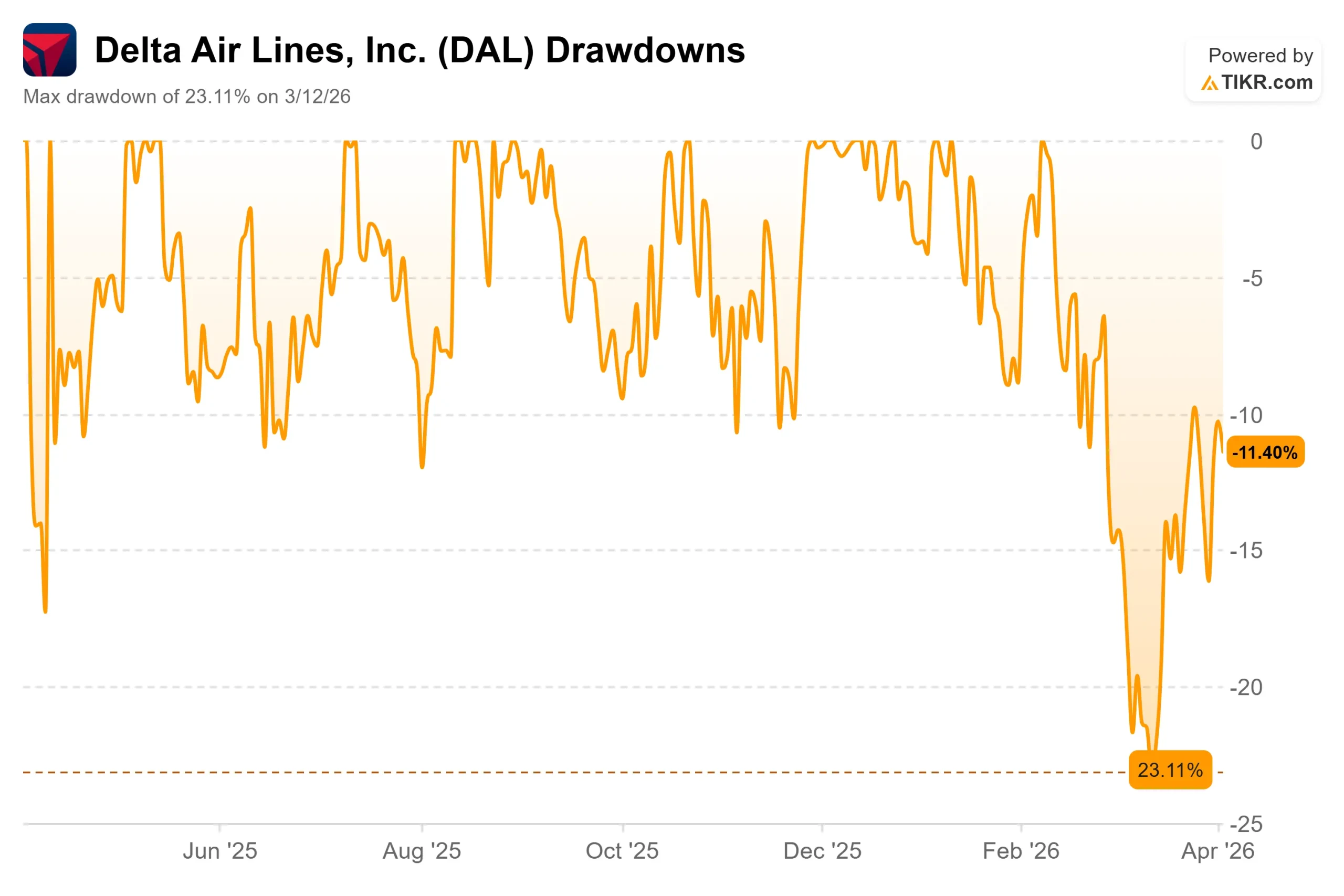

Delta Airlines (DAL) hit a max drawdown of -23.11% on March 12 and has not fully recovered. The Iran war sent jet fuel prices surging in late February, and airline stocks sold off across the board.

United Airlines, JetBlue, and Southwest fell 17.8%, 21%, and 25%, respectively, from when the conflict began. Delta dropped only 5.7%. That gap is the whole story.

The clearest signal of why came at the JPMorgan Industrials Conference on March 17.

Even after absorbing an estimated $400 million fuel cost increase in Q1, CEO Ed Bastian was unequivocal on demand. “Healthy demand, it’s across all segments, covering corporate, covering international, covering premium leisure, covering main cabin, covering our domestic system. We’re seeing strength in every market that we look at,” he said.

Delta had seen eight of the top ten sales days in its history that quarter, with bookings running 25% above the prior year.

Delta raised Q1 revenue guidance to high-single-digit percentage growth while holding its adjusted EPS range of $0.50 to $0.90. “The higher revenue is offsetting the cost of not just the fuel, but we’ve also had a pretty tough winter season in terms of storms,” Bastian told CNBC.

“So you put that all together, we’re expecting to come in within the original guidance.”

Q1 results drop on April 8 before the opening bell.

See historical and forward estimates for Delta Air Lines stock (It’s free!) >>>

Is Delta Air Lines Undervalued Today?

At 10.38x NTM P/E and 6.62x NTM EV/EBITDA, the multiple is cheap for what Delta has built. The company generated $3.84 billion in free cash flow in 2025 and has spent three years aggressively paying down debt.

At the JPMorgan conference, Bastian said Delta ended 2025 with adjusted net debt at its lowest level since 2019.

Three structural advantages separate Delta from its peers in this environment.

First, the American Express co-brand partnership generated $8.2 billion in remuneration in 2025, and management has targeted $9 billion for 2026. That revenue is tied to cardholder spending, not seat demand, so it does not compress when fuel spikes.

Second, Delta’s subsidiary Monroe Energy operates the Trainer Refinery near Philadelphia, giving it partial insulation against the refining cost surges hitting fully unhedged carriers. Deutsche Bank analyst Michael Linenberg, who added DAL to his “fresh money” buy list on April 2, said Delta is “best positioned to navigate through a higher fuel price environment given its diversified revenue streams and investment-grade rated balance sheet.”

Third, the Amazon Leo satellite Wi-Fi deal announced March 31 will bring low-Earth orbit connectivity to 500 aircraft starting in 2028, while competitors United, Southwest, and Alaska have committed to rival Starlink. “This agreement gives us the fastest and most cost-effective technology available to better connect the world today,” Bastian said.

The bear case is fuel staying elevated.

BofA analyst Andrew Didora, who reiterated his Buy rating, described two scenarios: sustained high fuel prices that force low-margin airlines into capacity cuts, or a faster conflict resolution driving a strong earnings recovery.

See how Delta Air Lines performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

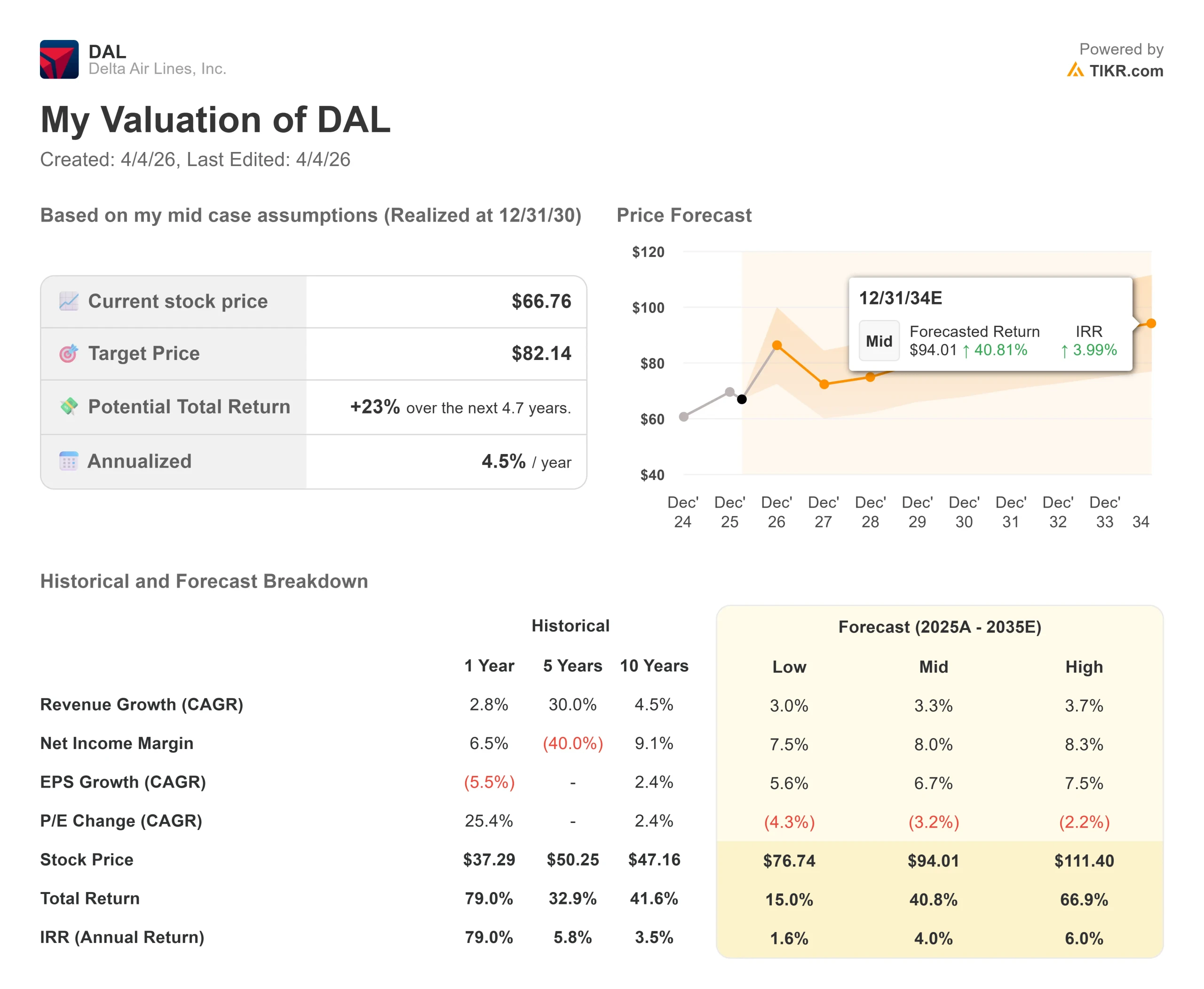

- Current Price: $66.76

- TIKR Target Price (High Case): $111.40

- Potential Total Return (High Case): +66.9%

- Annualized IRR (High Case): 6.00% / year

See analysts’ growth forecasts and price targets for Delta Air Lines stock (It’s free!) >>>

The TIKR high-case model reaches $111.40 by December 31, 2030, a 66.9% total return at 6.00% annualized. The mid-case lands at $82.14, a 23% total return at 4.5% IRR. The high case assumes a 3.7% revenue CAGR and an 8.3% net income margin, both within Delta’s demonstrated range.

Two revenue drivers support the model: premium and loyalty revenue anchored by the AmEx partnership’s $9 billion 2026 target, and international capacity recovery, with Atlantic revenue at $10.77 billion and Pacific at $3.36 billion in 2025. The margin driver is declining debt service: interest expense fell from $834 million in 2023 to $679 million in 2025, with TIKR estimates projecting a further drop to $575 million in 2026.

The downside scenario prices DAL at $76.74, a 15% total return at 1.6% annualized through 12/31/30. That scenario assumes the fuel shock persists and compresses TIKR’s 2026 normalized EPS estimate of $6.43.

Conclusion: Watch Q2 revenue guidance on April 8. If Delta guides above 5% year-over-year growth, the premium mix thesis holds. If guidance is cut or withdrawn, the recovery gets pushed back. The call begins at 10 a.m. ET.

Delta is a structurally stronger airline trading at a commodity carrier’s multiple. The fuel crisis created that discount. April 8 will show whether it starts to close.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Delta Air Lines?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Delta Air Lines, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Delta Air Lines alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Delta Air Lines on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!