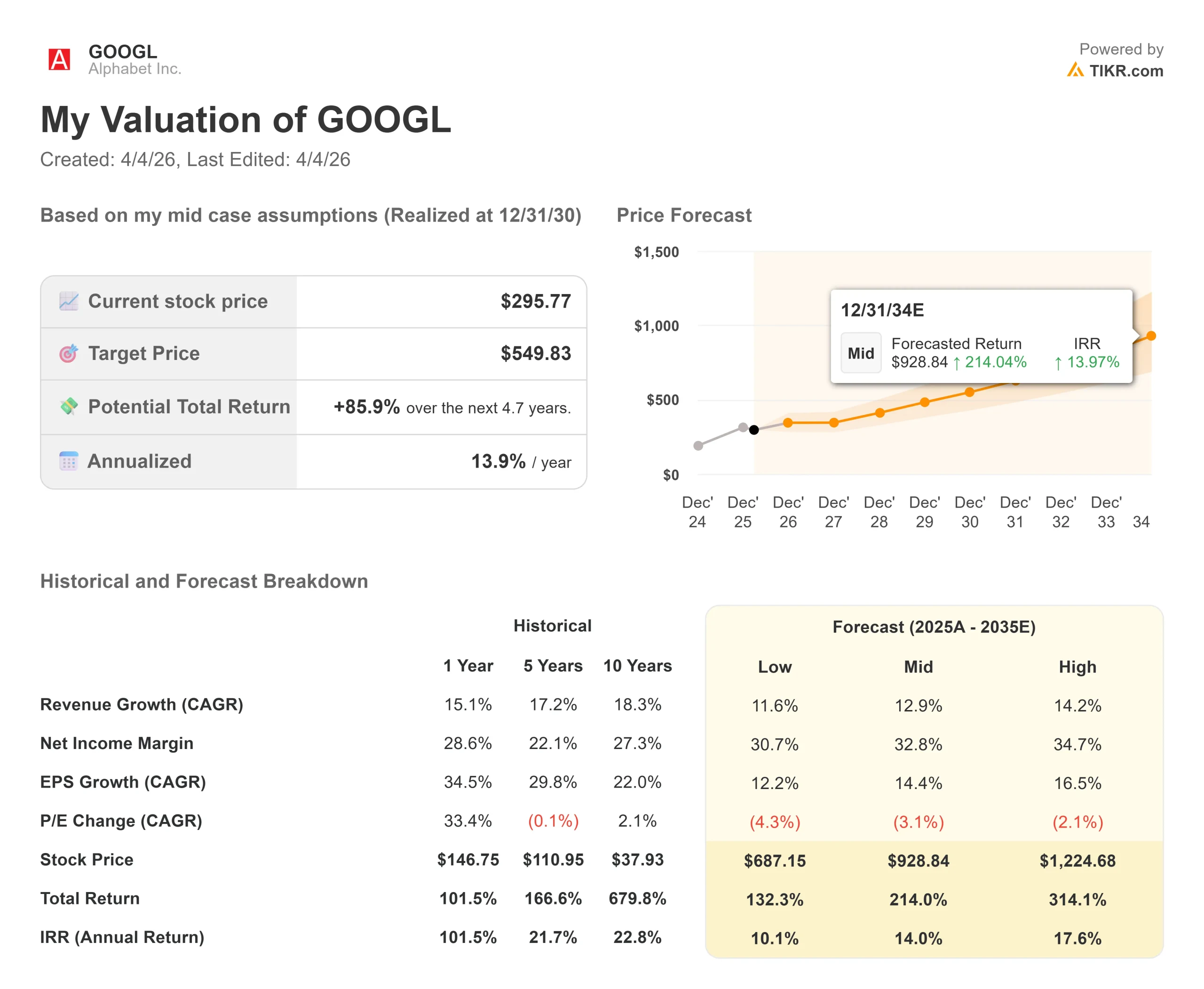

Key Stats for Alphabet Stock

- Current Price: $295.77

- Target Price (Mid): $549.83

- Street Target: $376.29

- Potential Total Return: +85.9%

- Annualized IRR: 13.90% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

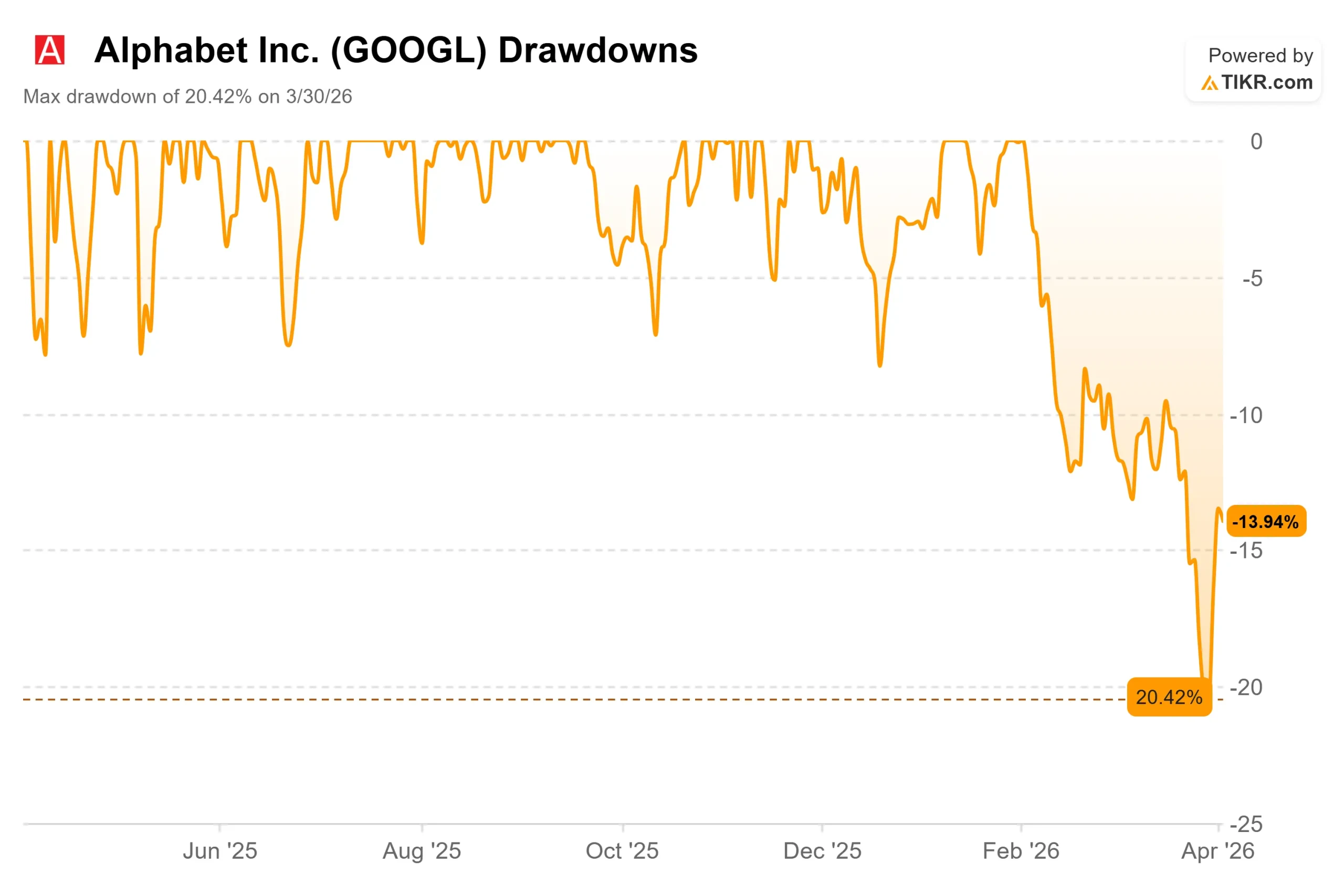

Alphabet (GOOGL) hit an all-time high of $349 in early February, then fell 20.42% to a trough on March 30. At $295.77, the stock sits well below where bulls expected it to be entering 2026, and the market is divided on whether the drop reflects a real problem or a sentiment overreaction to one number.

That number is management’s 2026 capital expenditure guidance of $175 billion to $185 billion, disclosed on the Q4 2025 earnings call on February 4.

The stock fell 0.54% on reporting day anyway. Bulls believe the capex is the price of AI infrastructure dominance and that Google Cloud’s acceleration makes it worthwhile.

Bears argue that the spend will compress free cash flow for years while regulatory risk accumulates, the DOJ’s pending adtech case could force a divestiture of Google’s Ad Exchange (AdX, Alphabet’s digital advertising marketplace), and a European antitrust damages verdict is due April 15.

See historical and forward estimates for Alphabet stock (It’s free!) >>>

Is Alphabet Undervalued Today?

At $295.77, GOOGL trades at 25.56x NTM P/E and 16.10x NTM EV/EBITDA.

As recently as December 31, 2025, those multiples sat at 29.40x and 18.22x, respectively. The business accelerated. The multiple contracts. That gap is where the valuation case lives.

The capex concern is not unfounded.

TIKR’s forward estimates show 2026 free cash flow compressing to approximately $22.0 billion before recovering to $49.3 billion in 2027 and $94.8 billion in 2028 as the infrastructure investment cycles through depreciation. The near-term pain is real.

Google Cloud is the reason to believe the recovery follows.

Per TIKR’s Segments data, Cloud revenue grew from $43.2 billion in 2024 to $58.7 billion in 2025, a 35.8% increase, while operating income more than doubled from $6.1 billion to $13.9 billion in the same period.

According to Alphabet’s Q4 2025 earnings call, Cloud backlog reached $240 billion after a 55% sequential increase, driven by enterprise demand for AI infrastructure and Gemini-powered services, and customer demand continues to outpace available capacity.

That is the context behind the $180 billion capex commitment.

Interactive Media and Services peer group trading at a mean NTM EV/EBITDA of 6.99x and a median of 4.95x. Alphabet’s 16.10x reflects a quality premium, not a value trap. Reddit (RDDT), the closest domestic peer by business model, trades at 17.73x NTM EV/EBITDA on a fraction of Alphabet’s revenue base and margins.

Among the Magnificent Seven (the seven largest U.S. tech companies), GOOGL trades at the lowest NTM P/E multiple in the group.

The discount to its own recent multiple is what creates the entry point.

The legitimate bear case is regulatory.

The 2025 DOJ search ruling imposed behavioral remedies rather than a structural breakup, a template the market read as favorable. Whether the pending adtech remedies ruling follows the same pattern or forces an AdX divestiture is the open question hanging over the stock.

See how Alphabet performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $295.77

- Target Price (Mid): $549.83

- Potential Total Return: +85.9%

- Annualized IRR: 13.90% / year

See analysts’ growth forecasts and price targets for Alphabet stock (It’s free!) >>>

The TIKR mid-case targets $549.83 by December 31, 2030, using a 12.9% revenue CAGR and a 32.8% net income margin. The two primary growth drivers are Google Cloud acceleration and resilient Search advertising. The margin assumption already embeds the near-term capex pressure and the subsequent recovery as Cloud operating leverage compounds.

Even the low case, an 11.6% revenue CAGR and a 30.7% net income margin, implies a 10.1% annualized IRR from today’s price. In the cautious scenario, Alphabet still generates positive double-digit annual returns. The risk that breaks the model is a forced AdX divestiture that removes material advertising revenue, or a sustained Cloud deceleration that makes the infrastructure spend look like an overshoot.

Conclusion: Watch Google Cloud revenue growth at Q1 2026 earnings on April 21. If Cloud growth holds near the 35.8% annual rate achieved in 2025 and operating margins continue expanding, the capex fear narrative loses its grip. That is the one metric worth tracking between now and then.

Alphabet is a $402.8 billion revenue business, confirmed by TIKR’s LTM Revenue figure, trading at its lowest earnings multiple in over a year. The selloff looks like sentiment, not fundamentals.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alphabet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alphabet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!