Key Stats for Domino’s Stock

- 52-Week Range: $246.3 to $499.1

- Current Price: $376.2

- Street Mean Target: $476.1

- Street High Target: $601

- TIKR Model Target (Dec. 2030): $615.8

What Happened?

Domino’s Pizza (DPZ), the world’s largest pizza chain by store count, is trading near its 52-week low at $376.24 despite delivering 8.5% operating income growth in fiscal 2025 and guiding for another 8% in 2026.

The narrative shift began on February 23, when Domino’s reported Q4 U.S. same-store sales growth of 3.7%, beating the analyst estimate of 3.5% and driven by the Best Deal Ever promotion, a value-focused pricing initiative that lifted transaction counts without requiring a ticket increase.

Free cash flow of $671.5 million in fiscal 2025 — up 31.2% year-over-year — is the number the market has underpriced, as it funded a 15% quarterly dividend increase to $1.99 per share and $354.7 million in share buybacks with $459.7 million still remaining under authorization.

On April 1, Jubilant Foodworks, the operator of 3,594 Domino’s locations across India, Sri Lanka, and Bangladesh, renewed its exclusive 15-year franchise agreement with a 10-year extension option, locking in the two fastest-growing international markets in the system for the long term.

CEO Russell Weiner stated on the Q4 2025 earnings call that “I believe that Domino’s can double our retail sales from where they are today, double,” anchoring the claim to 11 consecutive years of U.S. market share gains and franchisee store-level EBITDA of approximately $166,000 per unit in 2025.

Domino’s Pizza stock enters 2026 with the Hungry for MORE strategy, a four-pillar growth framework covering food, value, operations, and scale, now targeting 175-plus U.S. net store openings, approximately 800 international net additions, and 3% U.S. same-store sales growth atop a $4.4 billion carryout business that has compounded at 10% annually since 2010.

Wall Street’s Take on DPZ Stock

The Q4 beat on U.S. same-store sales, combined with 31.2% FCF growth and a raised dividend, shifts DPZ from a value-story execution risk into a confirmed cash-generation compounder entering a year of accelerating store growth.

Domino’s Pizza stock carries consensus 2026 revenue of $5.28 billion, growing 6.9% year-over-year on a full-year DoorDash contribution and 175-plus domestic openings, with normalized EPS expected at $19.82 and advancing to $21.49 by 2027 as operating leverage takes hold.

Twenty analysts rate DPZ a buy or outperform against 12 holds and just 2 negative recommendations; the mean price target of $476.06 implies approximately 26.5% upside from current levels, with the consensus waiting specifically on Q1 2026 U.S. same-store sales to confirm whether the Best Deal Ever relaunch sustains momentum through the first half.

The target spread from $340 to $601 signals a live debate: the bear case anchors to continued DPE headwinds and a tepid delivery recovery, while the $601 bull case prices in DoorDash reach expanding to fair share and a re-rating of the forward multiple once double-digit FCF growth becomes undeniable.

Trading near 19x 2026 estimated EPS with FCF up 31.2% and a 15% dividend raise confirmed, DPZ is undervalued against a franchise system that has closed just 13 stores across the last two years on a base of over 7,000 U.S. locations.

Berkshire Hathaway’s 12.3% increase in its DPZ stake to 3.4 million shares in Q4 2025 adds institutional weight to the thesis that the stock’s current discount reflects category fear rather than fundamental deterioration.

If DPE, the Australian and European franchise operator currently underperforming the system, does not return to positive same-store sales under its new McDonald’s-veteran CEO Andrew Gregory, the international algorithm breaks and the 800-store growth target for 2026 becomes unreachable.

Q1 2026 earnings on April 27 are the immediate test: U.S. same-store sales need to confirm the 3% full-year guide is tracking despite weather-related disruption in January, and the DoorDash channel contribution needs to show meaningful step-up from mid-2025 partial-year levels.

Domino’s Pizza Financial Performance

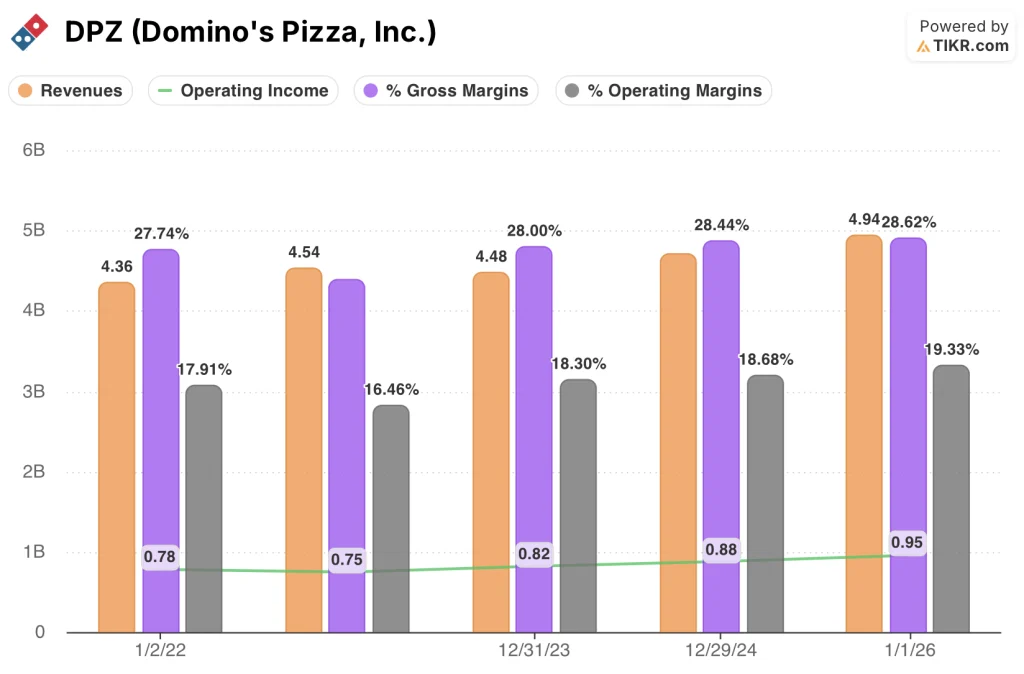

Domino’s Pizza grew total revenues from $4.71 billion in fiscal 2024 to $4.94 billion in fiscal 2025, a 5.0% increase that marks the third consecutive year of top-line growth after a brief contraction in fiscal 2023.

The operating income expansion from $880 million to $954 million, driven by supply chain procurement gains and higher franchise royalties from Best Deal Ever and Parmesan Stuffed Crust volume, pushed DPZ’s operating margin from 18.7% in fiscal 2024 to 19.3% in fiscal 2025.

Operating margins at Domino’s have now expanded from 16.5% in fiscal 2022 to 19.3% in fiscal 2025, a 280-basis-point improvement over three years that reflects the compounding benefit of a royalty-heavy, asset-light franchise model scaling against a relatively fixed SG&A base of $460 million.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $615.77 by December 2030, built on a 4.6% revenue CAGR and net income margins expanding to 13.3%, is the kind of number the current price makes no room for — at $376.24, the market is pricing in permanent impairment that eleven years of market share data and a 31% FCF surge simply do not support.

A 63.7% total return over 4.7 years at an 11% annualized IRR puts DPZ firmly in undervalued territory,particularly for a franchise system that has grown more profitable per unit every year of the strategy’s execution.

The Real Question for Domino’s Pizza Stock:

Whether the mid-case return materializes depends almost entirely on one variable: whether the international business, dragged down by DPE, can return to the system’s historical algorithm without requiring a multi-year turnaround.

Low Case (4.1% revenue CAGR, 12.7% net income margin): If DPE continues underperforming and DoorDash growth plateaus near current levels, the model returns $507 by December 2030, implying 34.8% total return and a 6.5% IRR.

Mid Case (4.6% revenue CAGR, 13.3% net income margin): With U.S. SSS at 3%, DPE stabilizing under Gregory, and DoorDash reaching fair share by 2027, the model targets $616 by December 2030, implying 63.7% total return and an 11.0% IRR.

High Case (5.0% revenue CAGR, 13.7% net income margin): If DPE returns to growth, Domino’s doubles its carryout share, and menu innovation accelerates unit economics, the model reaches $725 by December 2030, implying 92.8% total return and a 14.9% IRR.

The mid case requires 3% U.S. SSS maintained across 2026 and 2027 and no multiple contraction beyond the (3.5%) P/E CAGR already built into the model — no heroic re-rating, just operational execution the company delivered in fiscal 2025.

Domino’s Pizza stock is tracking that execution right now: Q4 U.S. SSS came in at 3.7%, the loyalty program grew to 37.3 million active users, the new e-commerce platform is live and outperforming its predecessor, and Best Deal Ever relaunched on February 23 as the primary 2026 comp driver.

Should You Invest in Domino’s Pizza, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DPZ stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Domino’s Pizza, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DPZ stock on TIKR for Free →