Key Stats for Western Digital Stock

- 52-Week Range: $33.4 to $348

- Current Price: $338.8

- Street Mean Target: $331.8

- Street High Target: $440

- TIKR Model Target (Jun 2030): $749

What Happened?

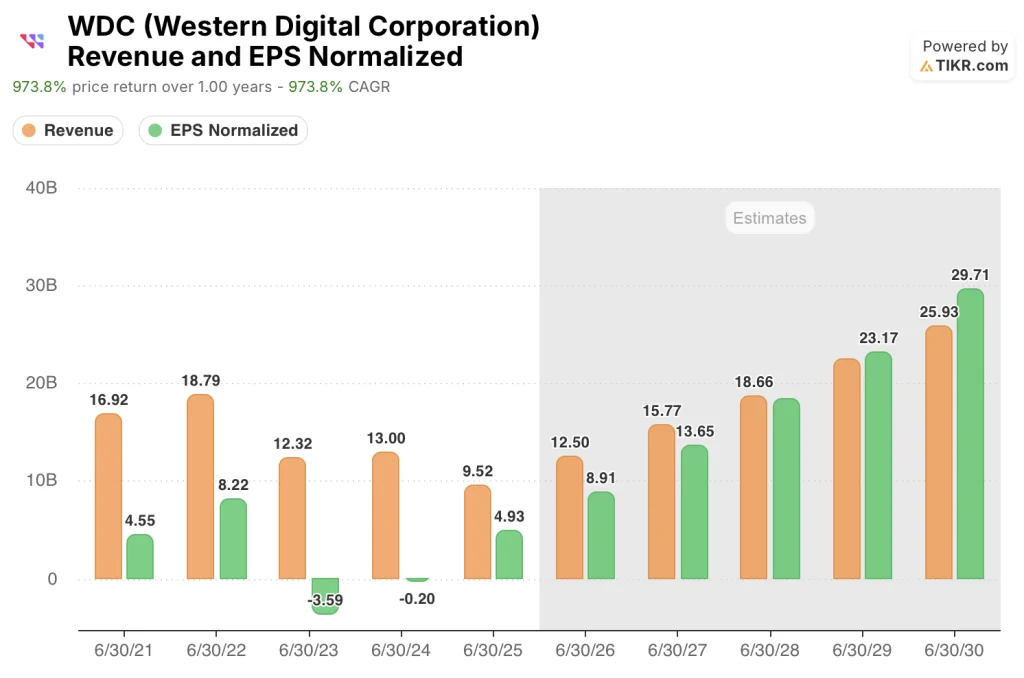

Western Digital (WDC), a hard disk drive manufacturer that has quietly become one of the most concentrated AI infrastructure plays in public markets, delivered 50.7% revenue growth in fiscal 2025 and operating income of $2.14 billion after posting a loss just two years earlier.

The rerating accelerated on February 3, when WDC hosted its Innovation Day in New York, unveiling a 40-terabyte ePMR drive, the world’s first, already in customer qualification, alongside HAMR drives offering a roadmap to 100 terabytes by 2029 — HAMR being a heat-assisted magnetic recording technology that uses laser energy to achieve far higher data densities per platter than conventional drives.

The number that changes the investment frame is not capacity but contract visibility: WDC secured firm purchase orders from its top seven hyperscale customers through all of calendar 2026, plus long-term agreements with three customers extending through 2027 and 2028, a structure that has never existed in the HDD industry’s history.

CEO Irving Tan stated on the Q2 fiscal 2026 earnings call that “we have firm purchase orders with our top seven customers through calendar year 2026,” anchoring that commitment to 215 exabytes delivered in the quarter, up 22% year-over-year, with cloud customers representing 89% of total revenue.

Western Digital stock enters the second half of fiscal 2026 with HAMR qualification underway at two separate hyperscale customers, a $4 billion share repurchase authorization approved in February on top of $484 million remaining from the prior $2 billion program, and a CFO-stated long-term target of greater than $20 in earnings per share as the company operates at 90% cloud and AI revenue concentration.

Wall Street’s Take on WDC Stock

The combination of firm purchase orders through 2026, mid-to-high single digit ASP per terabyte increases across all four quarters of calendar 2026, and a HAMR ramp pulling forward six months reframes WDC from a cyclical recovery into a multi-year earnings compounder with an unusual degree of revenue visibility.

WDC’s consensus FY2026 revenue estimate of $12.50 billion, growing 31.3% on locked hyperscaler POs and continued nearline exabyte shipment growth, supports normalized EPS of $8.91 — then accelerating to $13.65 in FY2027 and $18.40 in FY2028 as HAMR reaches scale and operating leverage compounds through a model CFO Kris Sennesael has described as targeting greater than 40% operating margins.

Twenty-one analysts rate WDC a buy or outperform against just five holds and zero sells; the mean target of $331.82 sits fractionally below current levels, but the consensus was set before the stock’s 8.6% session gain on April 8, and the median target of $335 and high of $440 suggest targets have not yet caught up with the April move.

The $182 to $440 target spread reveals a live debate worth understanding: the low end reflects genuine fear that Google’s TurboQuant compression algorithm, which claims to reduce AI memory requirements significantly, could eventually compress nearline HDD demand, while the $440 bull case prices in HAMR ramping on schedule and WDC re-rating to a secular growth multiple as FY2028 EPS of $18.40 becomes visible.

Trading at roughly 25x FY2027 estimated EPS of $13.65 with gross margins expanding from 22.2% two years ago to 38.8% last fiscal year and a long-term model pointing above 50%, Western Digital stock is undervalued for a business whose 90% cloud revenue concentration and locked purchase order book makes it structurally different from the cyclical storage company the market spent a decade pricing.

If the HAMR qualification timeline slips or early-ramp yields disappoint, the FY2027 and FY2028 EPS estimates that anchor the bull case do not materialize, and the current multiple becomes indefensible.

Q3 fiscal 2026 earnings, expected in late April or May, are the critical test: the $3.2 billion revenue midpoint guidance and 47% to 48% gross margin target need to hold, and any commentary on HAMR qualification progress with the two hyperscale customers currently in qualification will determine whether the FY2027 earnings ramp is tracking.

Western Digital Financial Performance

Western Digital’s revenue recovered from $6.26 billion in fiscal 2023 to $9.52 billion in fiscal 2025, a 50.7% increase in one year that reflects the inflection point when AI-driven hyperscaler demand for nearline HDD storage reached critical mass.

The operating income swing from a $380 million loss in fiscal 2023 to $2.14 billion in fiscal 2025 reflects two compounding forces: the SanDisk flash business spinoff removing the drag of the volatile NAND segment, and the rapid mix shift toward higher-capacity nearline drives that carry structurally better unit economics per terabyte shipped.

Western Digital’s gross margin expanded from 22.2% in fiscal 2023 to 38.8% in fiscal 2025, and LTM data shows that expansion continuing to 42.7%, a trajectory that management attributes to pricing stability, UltraSMR adoption crossing 50% of nearline shipments, and cost per terabyte declining approximately 10% annually as areal density improves.

What Does the Valuation Model Say?

The TIKR mid-case target of $749 by June 2030, built on a 19.9% revenue CAGR and net income margins expanding to 33.7%, is a number that requires no heroic assumptions — it essentially asks whether a business with locked hyperscaler POs, a CFO-stated EPS target above $20, and 90% data center revenue can sustain the growth trajectory already confirmed over the last four quarters.

At roughly 25x FY2027 earnings on a model pointing toward $18+ EPS by FY2028, WDC is undervalued for what is no longer a cyclical storage company but a secular AI infrastructure compounder with gross margins crossing 40% and rising.

Whether WDC earns a secular re-rating or snaps back to cyclical multiples depends on one thing: whether HAMR qualification converts to volume ramp on schedule and the $20+ EPS path holds through fiscal 2028.

Low Case (17.9% revenue CAGR, 31.4% net income margin): If HAMR ramp delays or exabyte demand growth moderates from mid-20s to high-teens, revenue grows more slowly and margins lag the model, targeting $553 by June 2030 for a 63.1% total return and 12.3% IRR.

Mid Case (19.9% revenue CAGR, 33.7% net income margin): With HAMR ramping in first half of calendar 2027 as guided and nearline exabyte CAGR holding at mid-20s through fiscal 2028, the model targets $749 by June 2030 for a 121.1% total return and 20.6% IRR.

High Case (21.9% revenue CAGR, 35.6% net income margin): If video AI workloads accelerate adoption faster than expected, pricing moves above stable into low-single-digit annual increases, and the new WD platform innovations (high-bandwidth drives, dual-pivot) reach 20%-plus of shipments, the model targets $987 by June 2030 for a 191.2% total return and 28.7% IRR.

The mid-case requires WDC to grow revenue at roughly 20% annually, a rate already exceeded in fiscal 2025 at 50.7% and already embedded in FY2026 consensus at 31.3%, meaning the mid-case assumes meaningful deceleration from current trends, not acceleration.

Western Digital stock is tracking well ahead of that bar right now: Q2 fiscal 2026 gross margins of 46.1% already exceed the model’s long-term target of greater than 50% by less than 4 percentage points, Bernstein upgraded the stock on April 1 citing the Google TurboQuant selloff as a buying opportunity, and Q3 guidance of $3.2 billion revenue midpoint would put full-year fiscal 2026 revenue on pace to reach or exceed the $12.50 billion consensus.

Should You Invest in Western Digital Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WDC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Western Digital Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WDC stock on TIKR for Free →