Key Stats for Copart Stock

- 52-Week Range: $32.2 to $63.9

- Current Price: $33

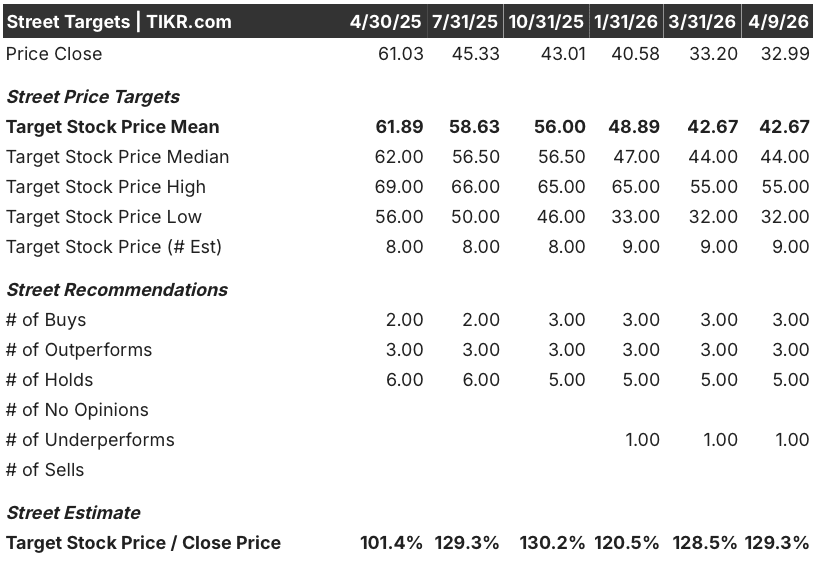

- Street Mean Target: $42.7

- Street High Target: $55

- TIKR Model Target (Jul. 2030): $45.2

What Happened?

Copart (CPRT), the global online vehicle auction platform connecting insurance carriers with buyers across 185 countries, sits at its 52-week low of $32.99 after second-quarter earnings revealed the first sustained revenue contraction in years.

The Q2 report released February 19 showed revenue falling 3.6% year over year to $1.12 billion, with EPS of $0.36 missing the $0.39 consensus estimate by 8.3% as vehicle volumes declined across both service and sales channels.

The volume softness traces to two converging pressures: insurance carriers retaining more vehicles internally as total-loss rates normalize, and consumers underinsuring amid inflation, which reduces the pool of totaled vehicles flowing into auctions.

Copart’s management noted on the Q2 earnings call that service revenue comparisons were distorted by one-time revenue from hurricanes Helene and Milton that boosted the year-ago fiscal 2025 quarter, creating an artificial basis that inflated the apparent year-over-year decline.

The company’s $1.25 billion unsecured revolving credit facility secured January 23, maturing 2031, alongside a $218.2 million share repurchase in the first half of fiscal 2026, signals confidence in cash generation even as volume headwinds persist into 2026.

Wall Street’s Take on CPRT Stock

The hurricane comparison distortion clears the books by Q3, but what replaces it determines whether Copart stock recovers from a 52-week low or grinds lower as soft insurance volumes prove structural rather than cyclical.

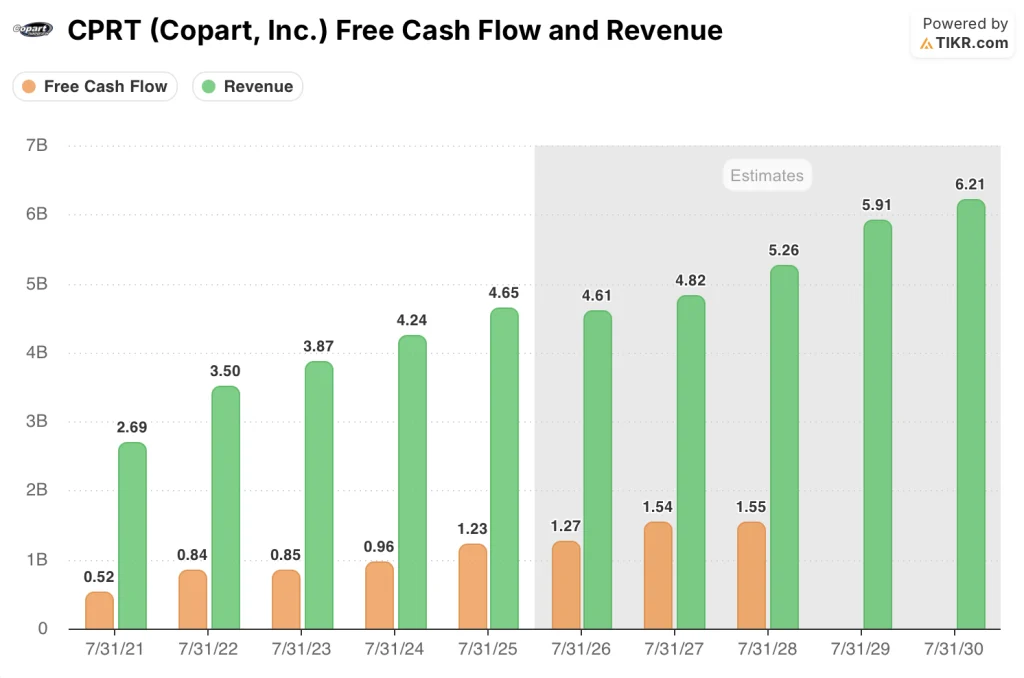

CPRT’s FCF reached $1.23 billion in fiscal 2025 and is estimated at $1.27 billion in fiscal 2026, backed by the platform’s asset-light auction model, even as revenue consensus sits at $4.61 billion with a projected 0.9% decline before returning to 4.7% growth in fiscal 2027.

Six of 12 analysts covering Copart stock hold buy or outperform ratings against five holds and one underperform, with a mean price target of $42.67, implying 29.3% upside from current levels, with the Street waiting on volume recovery data from the hurricane-clean comparison quarters.

The target spread between $32 and $55 reflects a genuine debate: bears see the low end as fair value if insurance carriers permanently internalize more volume, while bulls see $55 if Copart’s international expansion and used-car dealer network absorb the domestic softness.

Trading at roughly 21x forward earnings against a P/E of 25x just three months ago, with FCF margins projected to expand from 26.5% in fiscal 2025 toward 27.6% in fiscal 2026, Copart stock appears undervalued at current prices given that the near-term earnings pressure reflects a non-recurring hurricane comparison, not a permanent impairment of the platform’s economics.

If the next two quarters confirm that volume is recovering as the hurricane base effect washes out, the forward multiple re-rating alone could close much of the 29% gap to the mean analyst target.

Continued underinsurance trends or sustained carrier internalization of total-loss vehicles would structurally shrink the addressable auction pool and compress the revenue base permanently.

Q3 service revenue volume data, particularly unit trends in the U.S. where revenue fell 5.6% year over year in Q2, is the single figure to watch for confirmation that the volume floor is behind Copart.

Copart Stock Financials

Copart’s operating income reached $1.75 billion in fiscal 2025, a 37.7% operating margin representing the highest level in four fiscal years as platform scale absorbed cost growth faster than revenue growth decelerated.

The 9.7% revenue growth in fiscal 2025 to $4.65 billion drove an 11.4% increase in operating income, confirming that CPRT’s auction network operates with genuine operating leverage when unit volumes run at normal levels.

Gross margins expanded from 45.8% in fiscal 2024 to 47.2% in fiscal 2025, reflecting a mix shift toward higher-fee service revenue relative to lower-margin vehicle sales as the platform attracted more insurance carrier volume.

The Q2 operating income decline to $388.7 million, down 8.8% from the prior year, introduces a visible near-term tension: if service revenue volumes do not recover in the back half of fiscal 2026, the operating leverage that drove margin expansion to 37.7% will work in reverse.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $45.24, reached by fiscal 2030, assumes a 5.8% revenue CAGR and net income margins recovering toward 31.5%, both inputs supported by Copart’s $5.1 billion cash position and a buyback program that reduces the share count even in a soft volume year.

At $32.99, near the 52-week low of $32.20, CPRT is undervalued against a platform whose FCF generation of $1.27 billion in fiscal 2026 is essentially unaffected by the hurricane comparison headwinds that drove the Q2 selloff.

The gap between CPRT’s 52-week low and a $54.60 high-case target comes down entirely to one question: whether the current volume softness is a temporary base-effect problem or the beginning of structural carrier internalization.

Low Case (2.4% IRR, $37 target): Insurance carriers permanently internalize a larger share of total-loss vehicles, keeping revenue growth at 5.2% CAGR. Net income margins stabilize near 29.3%, below the fiscal 2025 level. Total return of 10.8% over the forecast period, roughly in line with holding cash.

Mid Case (7.6% IRR, $45 target): Hurricane base effects clear and volume normalizes, supporting 5.8% revenue CAGR with net income margins recovering to 31.5%. EPS grows at a 5.4% CAGR. Total return of 37.1% over 4.3 years, with no multiple expansion required.

High Case (12.4% IRR, $55 target): International expansion accelerates and used-car dealer network volumes absorb domestic softness, driving 6.4% revenue CAGR with margins reaching 33.3%. EPS CAGR of 7.1% delivers a 65.5% total return.

The mid case requires service revenue volume to stabilize as the hurricane comparison washes out of the fiscal 2026 base, with no multiple expansion assumed from the current 21x forward P/E.

Copart repurchased 5.5 million shares in the first half of fiscal 2026 at an average of $39.82, confirming management’s own view that current prices represent buyable value against a $5.1 billion cash reserve.

Should You Invest in Copart, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CPRT stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CPRT alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CPRTr stock on TIKR for Free →