Key Stats for PACCAR Stock

- 52-Week Range: $84.7 to $131.9

- Current Price: $118.2

- Street Mean Target: $127

- Street High Target: $150

- TIKR Model Target (Dec. 2030): $150

What Happened?

PACCAR Inc (PCAR), the manufacturer of Kenworth, Peterbilt, and DAF heavy-duty commercial trucks, enters 2026 with a structural earnings floor that didn’t exist a decade ago — parts and financial services, the two segments that generate recurring profit regardless of new truck demand, now contribute 71% of total company profit, up from 43% in 2014.

The Q4 2025 earnings report, released January 27, confirmed the depth of the cycle trough: revenue fell to $6.8 billion from $7.9 billion a year earlier, and net income dropped to $557 million as a sluggish U.S. freight market and tariff-driven production disruptions compressed truck-segment margins to 12% — but PACCAR Parts delivered record quarterly revenue of $1.7 billion, up 4% year over year, proving the durability of the aftermarket business even in a down cycle.

The tariff picture shifted materially in November 2025, when Section 232 truck tariffs — a U.S. national security trade measure that imposes duties on imported commercial vehicles — took effect, advantaging PACCAR directly: the company’s North American manufacturing footprint, spread across plants in Chillicothe (Ohio), Denton (Texas), and Sainte-Therese (Canada), qualifies for more than 50% relief on tariff exposure while most competitor trucks assembled outside the U.S. face new cost burdens, a dynamic Morgan Stanley flagged on January 14 when it raised its price target on PCAR to $102 from $93.

Preston Feight, Chief Executive Officer, stated on the Q4 2025 earnings call that “we ended last year with tariff and emissions clarity,” and tied that directly to the company’s Q1 2026 guidance of 12.5% to 13% gross margins, a step up from the 12% posted in Q4 2025 as factory transition costs from the local-for-local production shift fade.

PACCAR stock, trading at $118.20, sits 40% above its 52-week low of $84.65 as freight spot rates recover, Parts guides to 4% to 8% revenue growth in 2026, the EPA’s confirmation of the 35-milligram NOx standard for 2027 accelerates a prebuy cycle in heavy-duty trucks — where Class 8 industry volume is forecast at 230,000 to 270,000 units — and the company’s $9.3 billion in cumulative R&D and capital investment since 2016 positions it with the newest truck lineup in the industry.

Wall Street’s Take on PCAR Stock

The Q4 beat on revenue — $6.8 billion versus the $6.3 billion consensus — combined with management’s Q1 margin guidance of 12.5% to 13% shifts the forward picture from “trough survival” to “cycle acceleration,” with earnings expected to recover from $5.01 adjusted in 2025 to $5.61 in 2026 and $6.77 in 2027 as volume, tariff tailwinds, and Parts growth compound simultaneously.

PACCAR stock’s 2026E revenue of $27.7 billion and 2026E EPS of $5.61 are both anchored to confirmed operational drivers: the local-for-local manufacturing shift that removes competitor tariff parity, Parts guided to 4% to 8% annual growth, and an order intake that management described as “significant overbuild rate” entering January 2026.

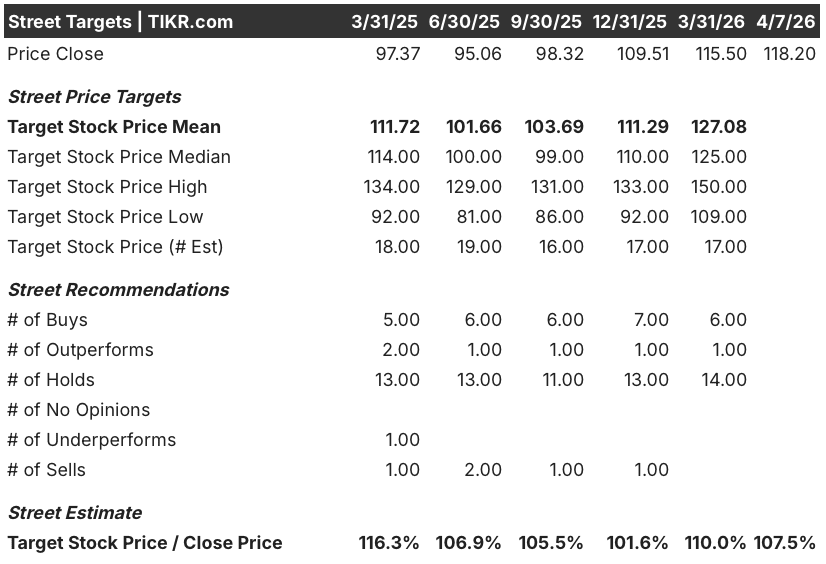

Seven of 21 analysts rate PCAR a buy or outperform — a minority position — while 14 hold, reflecting Wall Street’s wait-and-see posture on freight recovery and prebuy magnitude; the mean price target of $127.08 implies about 7.5% upside from $118.20, with the bull end at $150.00 and the bear end at $109.00.

The $41-point spread between the high and low targets reflects a genuine debate: bulls price in a strong 2027 prebuy ahead of EPA27 NOx compliance plus Parts share gains in the $33 billion second-owner aftermarket, while bears worry that the current 21x forward multiple already prices in the recovery before freight conditions fully confirm it.

At roughly 21x 2026E EPS against a historical P/E range that sat closer to 14x to 17x at comparable cycle stages, PACCAR stock is fairly valued — the elevated multiple is partially earned by the structural shift in earnings quality (Parts and Financial Services now at 71% of profit) and partially a bet on the magnitude of the 2027 prebuy that hasn’t yet materialized in order data.

Feight’s statement on the Q1 2026 outlook — that “Q2 should be an acceleration from Q1” — reframes the cadence: the margin recovery is not a point-in-time event but a sequential build through the year, making 2026E EPS of $5.61 a floor rather than a ceiling.

The model breaks if U.S. freight market recovery stalls and truckload carriers defer purchases again, which would compress both truck volumes and Parts growth simultaneously.

Q2 2026 gross margin, Parts revenue growth cadence, and Class 8 order intake in April and May are the specific numbers to watch — confirmation of sequential improvement from the 12.5% to 13% Q1 guide would validate the recovery thesis.

PACCAR’s Financial Picture

PACCAR’s total revenues contracted 15.5% in 2025 to $28.4 billion, the steepest single-year decline since the 2020 trough, driven by a 16.9% drop in truck revenues as North American Class 8 deliveries fell to 144,200 units from a higher prior-year base amid soft freight market conditions.

Gross profit fell 32.8% to $4.0 billion in 2025, but the compression reflects cyclical truck-segment margin pressure rather than structural deterioration — Parts, which carries roughly 30% gross margins and posted record revenue of $6.9 billion, insulated total profitability in a way PACCAR’s 2014 equivalent could not have.

The operating margin trajectory tells the structural story most clearly: PCAR averaged 9% operating margins over the five years ending 2016, improved to 10% over the following five years, and averaged 12% over the five years ending 2025 — a step-change improvement that reflects Parts and Financial Services absorbing an increasing share of the cost base across cycles.

The tension is real: 2025 operating income of $3.1 billion on $28.4 billion in revenue implies a 10.8% operating margin, a meaningful step back from the 14.8% posted in 2024, and the question for 2026 is whether margin recovery follows volume recovery fast enough to justify a 21x forward multiple.

What Does the Valuation Model Say?

The TIKR mid-case model targets $150.44 by year-end 2030, built on a 6.4% revenue CAGR and 12.1% net income margins — assumptions grounded in the Parts business’s confirmed $70 billion total addressable market and PACCAR’s five-year track record of doubling cycle-over-cycle earnings from trough to trough

PCAR is fairly valued at $118.20 — trading at roughly 21x 2026E earnings, the multiple reflects the structural improvement in earnings quality but leaves limited margin of safety until the 2027 prebuy cycle confirms in order data.

The real question for PACCAR stock isn’t whether earnings recover — the Parts flywheel and tariff advantage make some recovery near-certain — but whether the magnitude of the 2027 EPA27 prebuy, combined with Parts share gains in the $33 billion second-owner aftermarket, can push EPS toward the $11 consensus estimate for 2029 and re-rate the stock toward the $150 model target.

Base Case

- Parts revenue grows 4% to 8% in 2026 as guided, accelerating through the year as freight activity picks up and the 380,000 PACCAR engines past the five-year mark consume higher wear-related parts

- Section 232 tariff tailwinds provide more than 50% relief on PACCAR’s tariff exposure while competitors importing into the U.S. absorb new cost burdens, supporting truck pricing power through 2026

- EPA27 confirmation triggers a prebuy in Class 8 heavy-duty trucks, driving North American industry volume toward the top of the 230,000 to 270,000 unit guidance range

- 2026E EPS of $5.61 acts as a floor; 2027E EPS of $6.77 represents the first full-year benefit of prebuy volume and tariff normalization

Downside Risk

- Freight market recovery stalls before truckload carrier profitability recovers enough to release deferred truck purchases, compressing both truck deliveries and Parts growth below guidance

- USMCA renegotiation, expected later in 2026, introduces new tariff uncertainty that narrows the manufacturing cost advantage PACCAR built through the local-for-local production shift

- Forward P/E at 21x leaves minimal cushion if 2026 gross margins fail to sustain the Q1 guide of 12.5% to 13%, since any shortfall would compress both earnings and the multiple simultaneously

Should You Invest in PACCAR Inc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PCAR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PACCAR Inc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PCAR stock on TIKR for Free →