Key Stats for Paramount Stock

- 52-Week Range: $8.6 to $20.9

- Current Price: $10.6

- Street Mean Target: $12.9

- Street High Target: $20

- TIKR Model Target (Dec. 2030): $13.1

What Happened?

Paramount Skydance (PSKY) stock represents a company at the center of the biggest media bet of 2026: PSKY, formed from the August 2025 merger of Paramount Global and Skydance Media under CEO David Ellison, agreed in February to acquire Warner Bros. Discovery for $110 billion in enterprise value, a deal that would combine CBS, Paramount+, CNN, HBO Max, and over 15,000 films into a platform serving more than 200 million direct-to-consumer subscribers worldwide.

The winning bid of $31 per share in cash defeated a rival offer from Netflix, which had initially secured a deal for Warner’s studio and streaming assets at $27.75 per share before declining to match Paramount’s final offer, stating the price was “no longer financially attractive.”

The transaction is funded by $47 billion in equity from the Ellison family and RedBird Capital Partners, plus $54 billion in debt commitments from Bank of America, Citigroup, and Apollo, leaving the post-merger entity with approximately $79 billion in net debt at close.

David Ellison stated on the March 2 merger announcement call that “by uniting our iconic studios, complementary streaming platforms with a global footprint, our cable and linear networks and our world-class IP, we have the opportunity to help shape the future and build a next-generation media and entertainment company.”

The deal is expected to close in Q3 2026 after regulatory clearance, with the Warner Bros. Discovery shareholder vote scheduled for April 23, and the combined company projecting over $6 billion in cost synergies within three years of closing, primarily from non-labor sources including streaming technology stack consolidation and corporate overhead reductions.

Independent proxy adviser Glass Lewis recommended on April 10 that Warner Bros. shareholders vote for the Paramount deal, citing favorable terms compared to prior alternatives, a concrete validation signal ahead of the April 23 vote.

Wall Street’s Take on PSKY Stock

The WBD deal reframes PSKY from a legacy media fixer-upper into a streaming-scale platform thesis, with 200 million combined subscribers at close and a $6 billion synergy plan that would represent the most aggressive cost restructuring in media history.

PSKY’s normalized EPS is projected at $0.77 for 2026, up 49.0% year-over-year, before accelerating to $0.94 in 2027 as the deal’s synergy pipeline begins flowing to the bottom line, tied directly to Ellison’s Q4 earnings call commitment to realizing more than $2.5 billion in run-rate efficiencies by end of 2026.

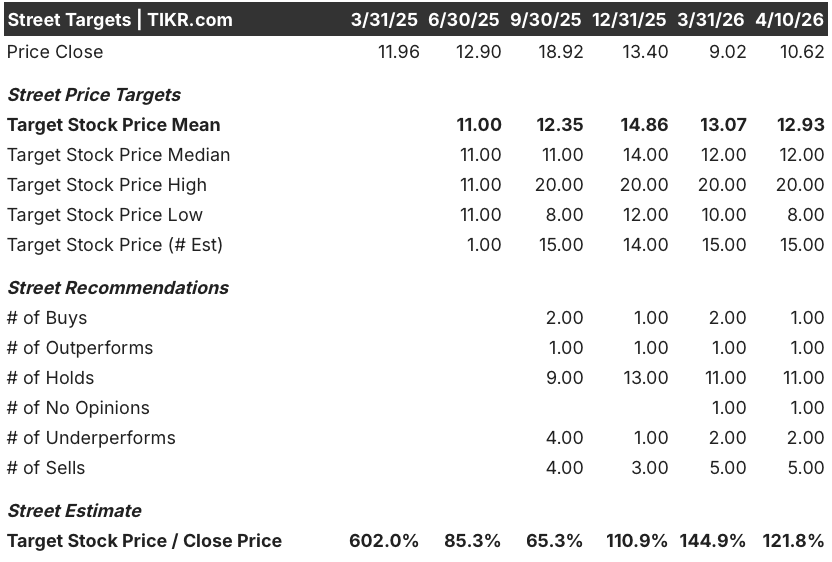

Fifteen analysts currently cover Paramount stock, with 1 Buy, 1 Outperform, 11 Holds, 2 Underperforms, and 5 Sells reflecting a sharply divided Street waiting on regulatory resolution; the mean price target of $12.93 implies 21.7% upside from the current $10.62, but the conviction is thin until the deal clears.

The target spread from $8 to $20 reveals a genuine binary debate: the $20 bull case prices in a clean Q3 close and full synergy realization, while the $8 floor reflects a California AG or DOJ-driven block that triggers Paramount’s $7 billion regulatory termination fee and substantially impairs standalone equity value.

Priced at 13.8x 2026 normalized EPS while projecting 49% earnings growth, Paramount stock appears undervalued relative to its recovery trajectory, with the discount reflecting regulatory uncertainty rather than deterioration in the underlying operational plan.

Glass Lewis’s April 10 recommendation for WBD shareholders to vote yes is the clearest signal yet that the April 23 vote passes, removing one layer of deal risk the market has been pricing in since February.

If the DOJ or California’s attorney general files to block the transaction, Paramount carries $13.7 billion in standalone net debt with no offsetting synergy benefit, a scenario where equity value could approach the $8 analyst floor.

The April 23 Warner Bros. Discovery shareholder vote is the single binary event to watch: a yes vote clears the path to Q3 close and unlocks the earnings recovery thesis, while a no or regulatory injunction resets the entire investment case.

Paramount Skydance Financials

Paramount Skydance’s revenue has contracted in three consecutive fiscal years, falling from $30.2 billion in 2022 to $28.9 billion in 2025, a 1.1% decline last year driven by accelerating cord-cutting in its TV Media segment, where subscriber losses are compressing both affiliate fee and advertising revenue faster than streaming growth can compensate.

The gross margin compression deepens the picture: gross profit declined from $10.8 billion in 2021 to $9.2 billion in 2025, pushing gross margins down from 37.9% to 31.8% as content investment, production overhead, and competitive streaming spend consumed a growing share of revenue across the four-year span.

Operating income has been the most volatile line on the income statement, declining from $4.0 billion in 2021 to $1.9 billion in 2025, with operating margins compressing to 6.5% as restructuring charges from the Skydance integration weighed on the year’s results.

These financials are not the bull case for PSKY. They are the reason the bull case is priced at $10.62: the WBD deal’s $6 billion synergy target represents more than three times last year’s operating income, meaning the thesis requires believing Ellison can engineer a structural transformation of a declining income statement through the most leveraged media acquisition in a generation.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $13.05 rests on a 13.8% EPS CAGR through 2030 and a net income margin recovery from 1.2% today toward 3.9%, assumptions tied directly to the WBD synergy realization creating operating leverage across a combined $69 billion revenue base once the deal closes.

PSKY appears undervalued at current levels, trading at 13.8x 2026 normalized EPS with 49% projected earnings growth and a mid-case model implying 22.9% total return to $13.05, a discount that prices in regulatory risk but not the scale advantage the combined platform would deliver if the deal closes as planned.

The spread between $10.65 and $15.29 across TIKR’s three scenarios captures precisely what makes PSKY one of the most polarizing setups in media right now: a deal that is either transformative or catastrophic, with almost no middle ground between those outcomes.

Low Case: $10.65 (0.3% total return)

- Revenue CAGR of 1.2% through 2030, barely above flat, reflecting a scenario where the WBD integration drags and linear TV declines faster than synergies offset

- Net income margin holds at 3.7%, with the $6 billion synergy target only partially delivered as cost actions meet union resistance and platform integration delays

- EPS CAGR of 12.0% still grows, but multiple compression of 7.6% annually keeps the stock pinned near current levels through 2030

- IRR of 0.1% annually: the low case is not a loss, but it is a four-year opportunity cost against any alternative

Mid Case: $13.05 (22.9% total return)

- Revenue CAGR of 1.3% paired with net income margin expansion to 3.9%, driven by deal synergies landing on schedule and DTC advertising growth accelerating as the combined platform scales

- EPS CAGR of 13.8% through 2030, absorbing both the 49% 2026 uplift and steady compounding as the $79 billion debt load is reduced toward the 3x leverage target within three years of close

- Multiple contracts 5.6% annually as the market transitions PSKY from a deal story to an operating earnings story, a reasonable assumption for a media business exiting a major integration

- IRR of 4.5% annually: modest absolute return, but meaningful if the deal clears the regulatory gauntlet cleanly

High Case: $15.29 (44.0% total return)

- Revenue CAGR of 1.4% with net income margin reaching 3.9%, identical margin to the mid case but with better revenue momentum from a faster DTC ramp and sports rights monetization across the NFL, UFC, and Olympics portfolio

- EPS CAGR of 15.1% through 2030, reflecting upside from subscriber growth on the combined platform closing the gap toward Netflix’s 325 million global subscribers

- Multiple compression moderates to 3.8% annually, implying the market re-rates PSKY as a scaled streaming competitor rather than a leveraged legacy media name

- IRR of 8.0% annually: the high case requires the deal to close cleanly, synergies to land ahead of schedule, and the DTC platform to demonstrate genuine competitive traction before 2028

Should You Invest in Paramount Skydance Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PSKY stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Paramount Skydance Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PSKY stock on TIKR for Free →