Key Takeaways:

- Lululemon continues to deliver steady revenue growth, but momentum has slowed to 4.9% annually.

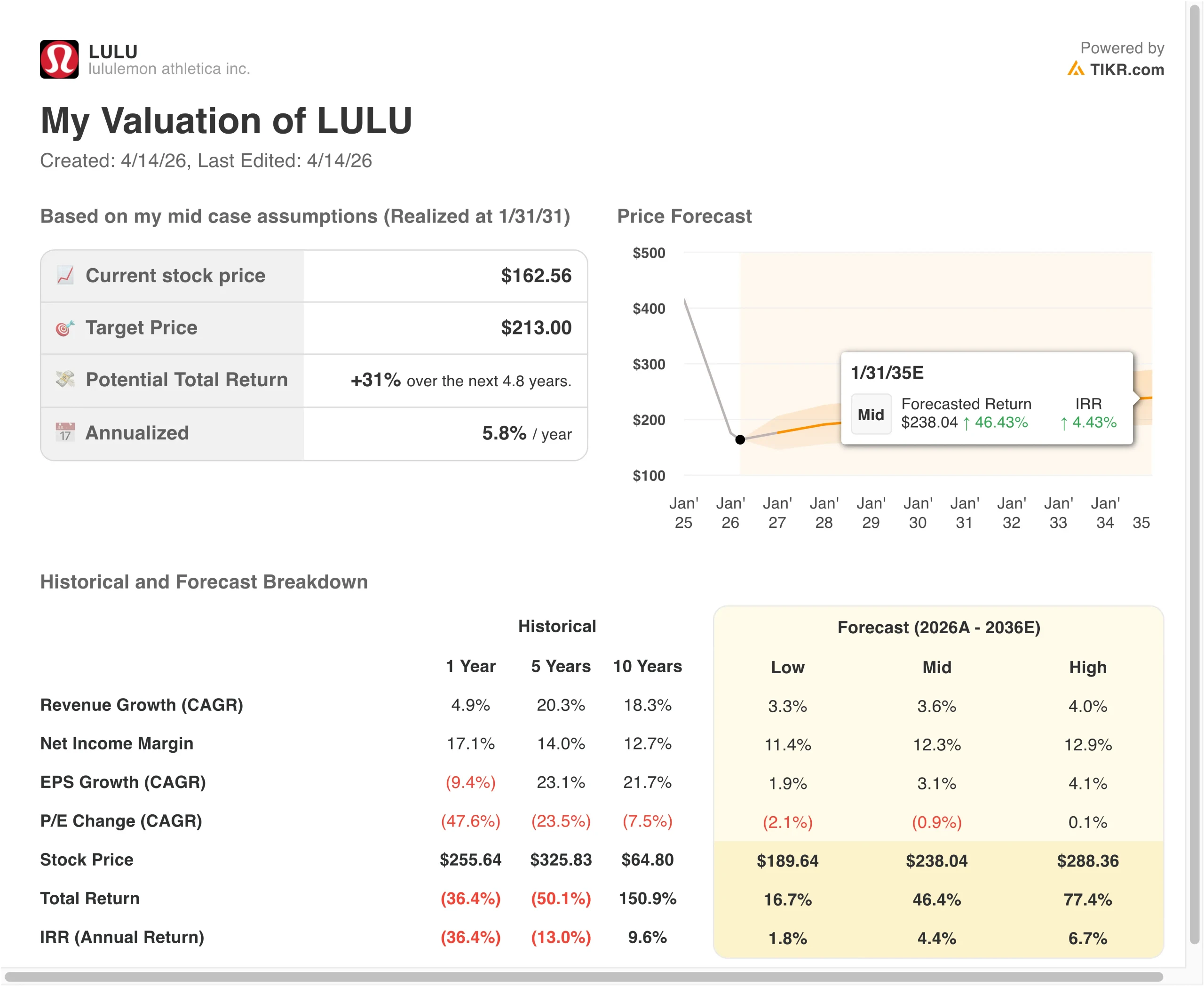

- LULU stock could reasonably reach $197 per share by early 2029, based on valuation assumptions.

- This implies a total return of 21.3% from today’s price of $163, with an annualized return of 7.1% over the next 2.8 years.

What Happened?

Lululemon athletica inc. (LULU) has been under pressure in 2026 as investors reassess its growth trajectory following a sharp slowdown in revenue expansion and rising operational risks. The stock now trades near $163, significantly below its 52-week high of $340, reflecting a reset in expectations after years of premium growth.

Recent news has added to investor caution. In April 2026, Texas regulators launched a probe into potential “forever chemicals” in Lululemon products, creating uncertainty around compliance and brand perception. At the same time, insider activity showed mixed signals, with executives both buying and selling shares, suggesting uncertainty even within leadership.

Earnings and corporate developments have also shaped sentiment. The company reported Q4 revenue of $3.6 billion, slightly above expectations, but operating income declined year-over-year, with margins compressing to 19.9%. Meanwhile, activist investor Elliott built a $1 billion stake, and founder Chip Wilson publicly pushed for board changes, highlighting governance tensions.

Operationally, Lululemon continues expanding globally, including opening its 100th store in EMEA. However, macro pressures like consumer spending shifts and higher costs have slowed growth, while the company transitions staffing models in North America. Investors are now questioning whether Lululemon can sustain its historical premium valuation.

Here’s why lululemon stock could remain range-bound as growth moderates and investors wait for clearer margin recovery.

What the Model Says for LULU Stock

We analyzed the upside potential for lululemon stock using valuation assumptions based on its slowing revenue growth, still-strong margins, and a more normalized valuation multiple after the recent decline.

Based on estimates of 4.3% annual revenue growth, 17.4% operating margins, and a normalized P/E multiple of 13.2x, the model projects lululemon stock could rise from $163 to $197 per share.

That would be a 21.3% total return, or a 7.1% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for LULU stock:

1. Revenue Growth: 4.3%

Lululemon’s revenue growth has slowed materially, declining from 42% in 2022 to just 4.9% in the latest period. This reflects both tougher comparisons and a maturing core business in North America. Growth is increasingly reliant on international expansion and product innovation.

The company continues to expand globally, including new store openings in Europe and Asia. However, same-store sales growth has slowed to around 2%, indicating softer demand in existing markets. This shift suggests the brand is transitioning from hyper-growth to a more mature phase.

Based on analysts’ consensus estimates, we use a 4.3% growth rate, reflecting continued international expansion but slower domestic demand and macro headwinds.

2. Operating Margins: 17.4%

Lululemon has historically delivered strong margins, but recent results show pressure. Operating margins declined from 23.7% to 19.9%, driven by higher SG&A expenses and increased investments in growth initiatives.

Cost pressures are evident across the business. Selling, general, and administrative expenses rose to over $4 billion, while gross margins declined to 56.6%. These trends reflect both inflationary pressures and strategic spending on digital and international growth.

Based on analysts’ consensus estimates, we use a 17.4% margin assumption, reflecting continued investment and modest margin compression relative to historical peaks.

3. Exit P/E Multiple: 13.2x

Lululemon’s valuation has compressed significantly, with its P/E ratio now around 12.3x on a trailing basis. This is well below historical averages, reflecting lower growth expectations and increased uncertainty.

The company still maintains strong returns on capital, including ROIC above 32% and ROE of 34%. However, slower earnings growth and macro risks have reduced investor willingness to pay a premium multiple.

Based on analysts’ consensus estimates, we use a 13.2x exit multiple, reflecting a balanced view between Lululemon’s strong brand and profitability versus its slower growth outlook.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for LULU stock through 2031 show varied outcomes based on growth recovery, margin execution, and valuation trends (these are estimates, not guaranteed returns):

- Low Case: Growth slows further, and margins compress → 1.8% annual returns

- Mid Case: Stable growth and steady margins → 4.4% annual returns

- High Case: Strong international expansion and margin recovery → 6.7% annual returns

Lululemon’s future performance will depend on its ability to reignite growth while maintaining profitability. The company remains financially strong, with minimal net debt and solid cash generation, but its premium growth narrative is being tested. Investors are likely to focus on upcoming earnings and international performance as key indicators of long-term value.

See what analysts think about LULU stock right now (Free with TIKR) >>>

Should You Invest in lululemon athletica inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LULU, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track LULU alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze lululemon athletica stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!