Key Stats

- Current price: ~$258 (April 21, 2026)

- Q2 FY2026 revenue: $5.3B (+22% YoY)

- Full-year calendar 2025 revenue: $20.6B (+27% YoY)

- Full-year calendar 2025 non-GAAP EPS: $4.89 (+49% YoY)

- Q2 FY2026 non-GAAP EPS: $1.27 (above guidance range)

- Q3 FY2026 revenue guidance: ~$5.7B

- Q3 FY2026 EPS guidance: $1.35

- TIKR model price target: ~$279

- Implied upside over 4 years: ~8%

Lam Research Stock Q2 2026 Earnings Breakdown

Lam Research stock (LRCX) posted a record December quarter, with revenue of $5.3B rising 22% year over year and EPS of $1.27 coming in above the high end of guidance.

Foundry drove the headline: the segment accounted for 59% of systems revenue in Q2, up sharply from 35% in the year-ago period, reflecting accelerating investment at the leading edge alongside continued mature node spending in China.

DRAM was the standout within memory, generating a record 23% of systems revenue in Q2, up from 16% in the prior quarter, as high-bandwidth memory investment and 1B/1C node transitions continued to ramp.

NAND stepped back to 11% of systems revenue from 18% in September, in line with customer plans, with management noting upgrade momentum would be weighted toward the second half of 2026.

Gross margin of 49.7% and operating margin of 34.3% both exceeded the high end of guided ranges, according to Doug Bettinger, Executive Vice President and CFO, on the Q2 FY2026 earnings call.

The Customer Support Business Group contributed approximately $2B in revenue for the quarter, up 12% sequentially and 14% year over year, with Lam’s installed base crossing 100,000 chambers for the first time.

The sequential CSBG jump was driven primarily by Reliant Systems demand across both multinational and China-based customers, with management flagging that component as potentially lumpy quarter to quarter.

For the full calendar year 2025, Lam Research posted record revenue of $20.6B, record operating margin of 34.1%, and EPS of $4.89, up 49% year over year.

Looking into calendar 2026, management expects WFE to reach approximately $135B, up from roughly $110B in 2025, with growth constrained by available clean room space rather than end demand.

Advanced packaging is forecast to grow more than 40% for Lam in 2026, driven by HBM4 adoption and expanding complex packaging architectures in foundry and logic.

Lam guided Q3 FY2026 revenue to around $5.7B, gross margin to 49% and EPS to $1.35.

Lam repurchased approximately $1.4B in shares during the December quarter at an average price of ~$154 per share, and returned 85% of free cash flow across full-year 2025.

Lam Research Stock: Financials

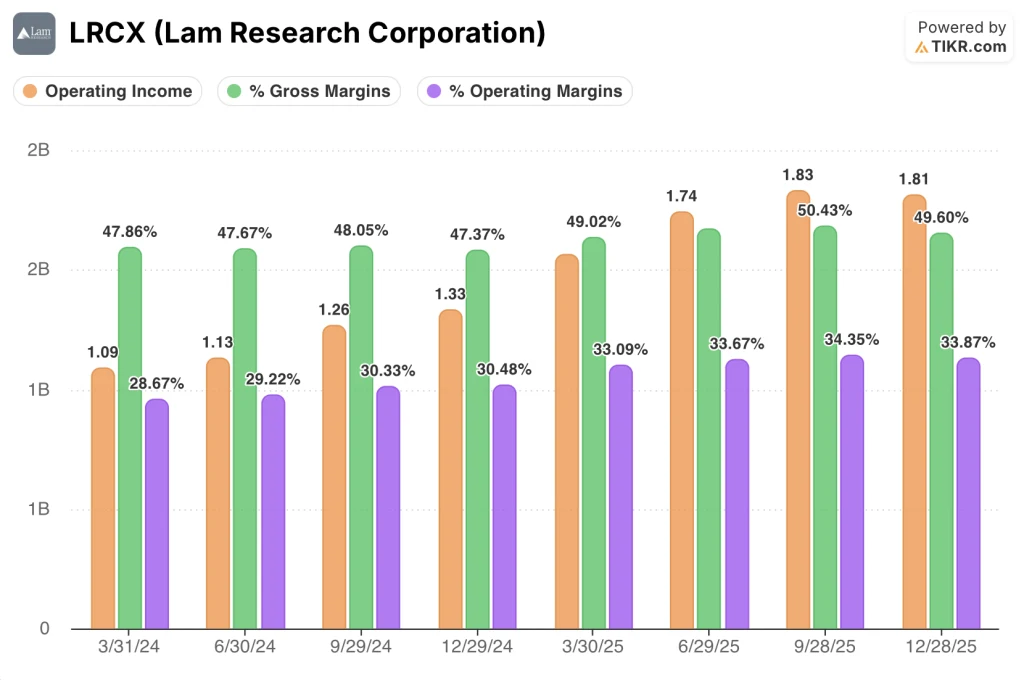

Lam Research stock is executing a sustained operating leverage story: ten consecutive quarters of revenue growth while gross and operating margins hold near cycle highs.

Q2 gross margin came in at 49.6%, roughly in line with the prior quarter’s 50.4% and up from 47.4% in the year-ago period.

Q2 operating income was $1.81B, up 35.7% year over year.

Q2 operating margin was 33.9%, down modestly from 34.4% in September but up sharply from 30.5% in the year-ago December period.

The trailing four-quarter operating margin range of 33.1% to 34.4% compares to a range of 28.7% to 30.5% one year prior, reflecting broad-based improvement at scale.

Q3 operating margin is guided to ~34%, suggesting margins hold near current levels as revenue steps up to ~$5.7B.

Valuation Model Take

The TIKR model prices Lam Research stock at ~$279, implying roughly 8% total return from the current price of ~$258 over the next four years.

The mid-case assumptions are revenue CAGR of 10% and net income margin of 28.2%, consistent with a business growing at a measured pace after delivering 27% revenue growth in 2025.

Critically, the model assumes P/E multiple compression of 5.4% annually through 2030, meaning the $279 target is not a “new normal” for AI-exposed semis — it is a mean reversion scenario where a premium multiple gradually deflates even as earnings grow.

The Q2 report supports the earnings side of that equation: a record quarter, guidance stepping up to $5.7B in Q3, and 85% free cash flow returned to shareholders.

Where the model reflects caution is on the multiple: with the high case implying 51.5% total return and the low case implying a 10.1% loss, the range of outcomes is wide, and the mid case sits close to today’s price precisely because it assumes the market pays less per dollar of earnings over time.

The investment case is intact after this quarter, but Lam Research stock needs continued WFE share gains and margin trajectory to offset the multiple compression the model is already pricing in.

The central tension in Lam Research stock: a multi-year AI-driven demand wave is clearly accelerating, but the stock is priced close to model fair value today, making the upside case contingent on outperformance that goes beyond what the current demand environment already implies.

What Has to Go Right

- WFE grows from $110B in 2025 toward $135B in 2026, with Lam gaining WFE share for a second consecutive year across all three device segments, as management guided on the Q2 FY2026 earnings call

- Gate-all-around adoption adds $1B of incremental SAM per 100,000 wafer starts per month, with backside power delivering the same step-up in a subsequent node, setting up a multi-year SAM expansion runway

- Advanced packaging revenue grows 40%+ in 2026 through HBM4 adoption and TSV etch intensity in Syndion and SABRE 3D, reinforcing Lam’s near-total market share in the drill-and-fill process steps

- CSBG sustains high-single-digit to low-double-digit growth with 102,000 chambers in the installed base and results-based service contracts driving dollar growth above installed base unit growth

What Could Still Go Wrong

- China represented 35% of Q2 revenue and is expected to decline as a percentage of total in 2026, removing a tailwind that has supported both systems revenue and Reliant demand in recent quarters

- Q3 gross margin is guided to 49%, with management citing customer mix headwinds as the largest customers (who receive the most favorable pricing) drive a growing share of systems revenue

- Clean room constraints capping WFE at $135B in 2026 could limit Lam’s ability to fulfill customer pull-in requests, deferring first-half revenue and compressing near-term results below what demand alone would support

- The TIKR model’s low case produces a 10.1% total loss by mid-2030, a realistic outcome if foundry/logic investment softens or NAND greenfield additions are pushed further into 2027 and 2028 than currently expected

Should You Invest in Lam Research Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LRCX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lam Research Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LRCX stock on TIKR for Free →