Key Takeaways:

- AMAT is still executing well. In fiscal Q1 2026, Applied reported revenue of $7.01 billion, non-GAAP EPS of $2.38, record DRAM revenue in Semiconductor Systems, and record services and spares revenue in Applied Global Services.

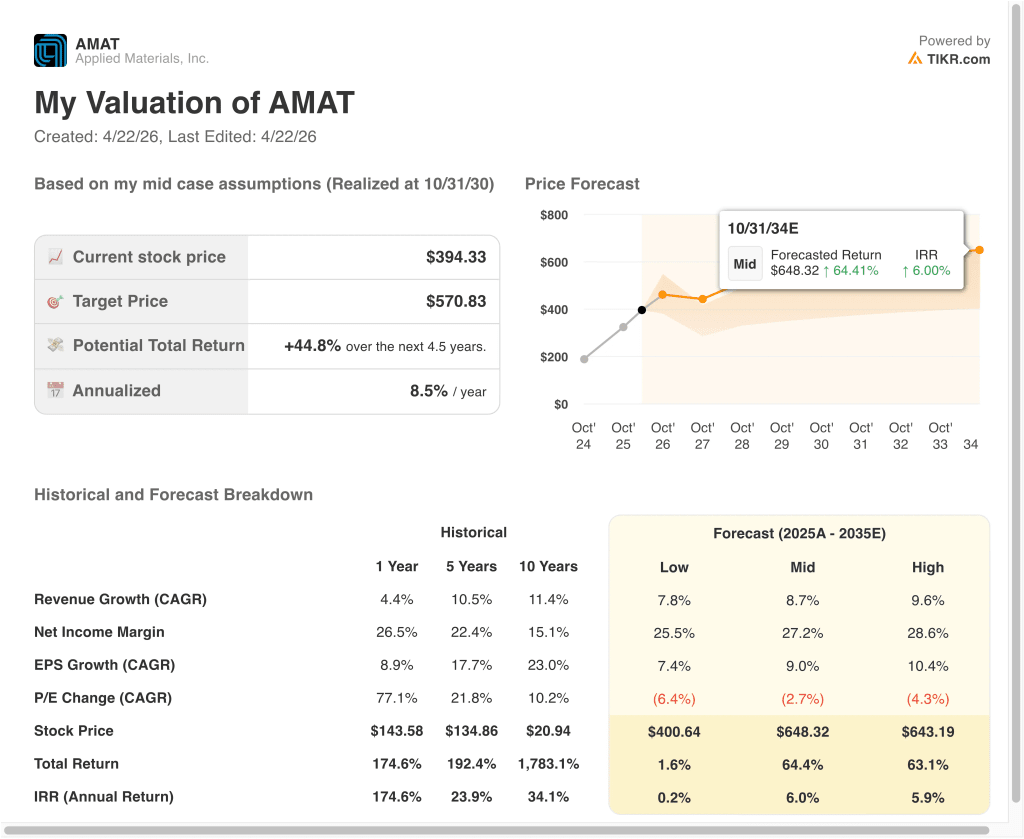

- Applied Materials’ stock could reasonably reach around $439 per share by late 2028, based on the valuation model.

- That implies about an 11% total return from the current price of $394, or roughly 4% annualized over the next 2.5 years.

What Happened?

Applied Materials (AMAT) is in focus because the market is still rewarding companies tied to the AI semiconductor buildout. On April 21, the company said Advantest would become an innovation partner for its EPIC platform in Silicon Valley, with the two companies working together to connect front-end semiconductor manufacturing and back-end testing more closely.

This comes after another important AI-related announcement in March. Reuters reported that Applied partnered with Micron and SK Hynix to develop next-generation memory chips for AI and high-performance computing, and those companies are becoming founding partners at the company’s EPIC Center.

The last earnings report also reinforced that theme. Applied said Q1 fiscal 2026 revenue was down 2% year over year to $7.01 billion, but non-GAAP EPS still came in at $2.38, ahead of estimates cited by Reuters, while Gary Dickerson said AI computing is accelerating investment in leading-edge logic, high-bandwidth memory, and advanced packaging. He also said Applied expects to grow its semiconductor equipment business by more than 20% in calendar 2026.

There is still another side to the story. In February, Applied agreed to pay $252 million to resolve allegations of illegal chip-equipment exports to China, and Reuters reported in November that stricter U.S. export curbs were expected to reduce China’s wafer fab equipment spending in 2026.

Here’s why Applied Materials stock could stay sensitive from here: investors are balancing real AI-driven demand against China exposure, regulation, and the fact that the stock has already moved a long way.

What the Model Says for AMAT Stock

We analyzed the upside potential for Applied Materials stock using valuation assumptions based on continued semiconductor demand, high margins, and a still-premium earnings multiple.

Based on estimates of around 7% annual revenue growth, around 30% operating margins, and a normalized P/E multiple of around 33x, the model projects Applied Materials’ stock could rise from $394 to $439 per share.

That would be an 11.3% total return, or a 4.3% annualized return over the next 2.5 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for AMAT stock:

1. Revenue Growth: 7%

Applied has already built a very large revenue base. Fiscal 2025 revenue reached $28.4 billion, up 4% year over year, and the company described that as its sixth consecutive year of growth. That matters because it shows Applied is still expanding even after a huge multi-year run in semiconductor capital spending.

The segment mix helps explain why growth has held up. In fiscal 2025, Semiconductor Systems produced about $20.8 billion of revenue, while Applied Global Services added about $6.4 billion, and management said recurring services and parts delivered another year of double-digit growth. That gives Applied both capital equipment exposure and a more durable service stream tied to its installed base.

Based on analysts’ consensus estimates, we use around 7% annual revenue growth. That is below the company’s expected semiconductor equipment growth for calendar 2026, but it reflects a more normalized pace over time after a strong AI-driven spending cycle. It also captures the reality that China’s demand may be weaker even while leading-edge logic, memory, and packaging stay strong.

2. Operating Margins: 30%

Applied is already a very profitable business. In Q1 fiscal 2026, non-GAAP operating margin was 30.0%, and the latest trailing EBIT margin in the materials you provided is 29.9%. That tells us the model is not assuming a heroic margin breakout, but more of a continuation of current performance.

The margin profile is supported by product mix and service revenue. Gross margin was 49.1% on a non-GAAP basis in Q1, and management said record DRAM revenue plus record services and spares revenue helped support results.

Based on analysts’ consensus estimates, we use around 30% operating margins. That fits both the current operating profile and the company’s positioning in higher-value areas like high-bandwidth memory and advanced packaging. It also avoids assuming that every part of the business improves at once.

3. Exit P/E Multiple: 33x

The exit multiple is where the model stays somewhat demanding. The current valuation materials show AMAT trading at about 32.6x next-twelve-month earnings, while the model uses a normalized P/E of around 32.6x as well.

There is a reason for that. Reuters reported that analysts tracked by the street lifted targets materially as AI demand improved, and the latest mean target in the materials you provided sits around $423, with the high target at $500. That shows the market is still willing to award Applied a premium multiple because it is tied to one of the strongest capital spending themes in tech.

Based on analysts’ consensus estimates, we use an exit P/E multiple of around 33x. That reflects Applied’s leadership in semiconductor equipment, its strong cash generation, and its direct exposure to AI infrastructure demand. But it also means a lot of optimism is already embedded in the stock, which helps explain the modest expected return in the base case.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for Applied Materials stock through 2035 show varied outcomes based on AI semiconductor demand, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI-related spending cools, China remains a larger drag, and valuation compresses faster → 0.2% annual returns AI-related spending cools, China remains a larger drag, and valuation compresses faster -> 0.2% annual returns

- Mid Case: Applied keeps benefiting from leading-edge logic, memory, and services demand → 6.0% annual returns

- High Case: Revenue and margins beat the base case, but valuation still compresses → 5.9% annual returns

Going forward, the stock will likely move with each new read on AI infrastructure demand, memory spending, export controls, and whether customers keep prioritizing advanced packaging and high-bandwidth memory.

See what analysts think about AMAT stock right now (Free with TIKR) >>>

Should You Invest in Applied Materials, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMAT, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMAT alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Applied Materials stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!