Key Takeaways:

- In Q1 fiscal 2026, Starbucks reported global comparable sales up 4%, with North America and U.S. comparable sales also up 4%, helped by a 3% increase in comparable transactions.

- Investors are seeing better traffic trends, a cleaner China structure, and a still-valuable global brand, but they are also seeing weaker profitability and slower top-line growth than in past cycles.

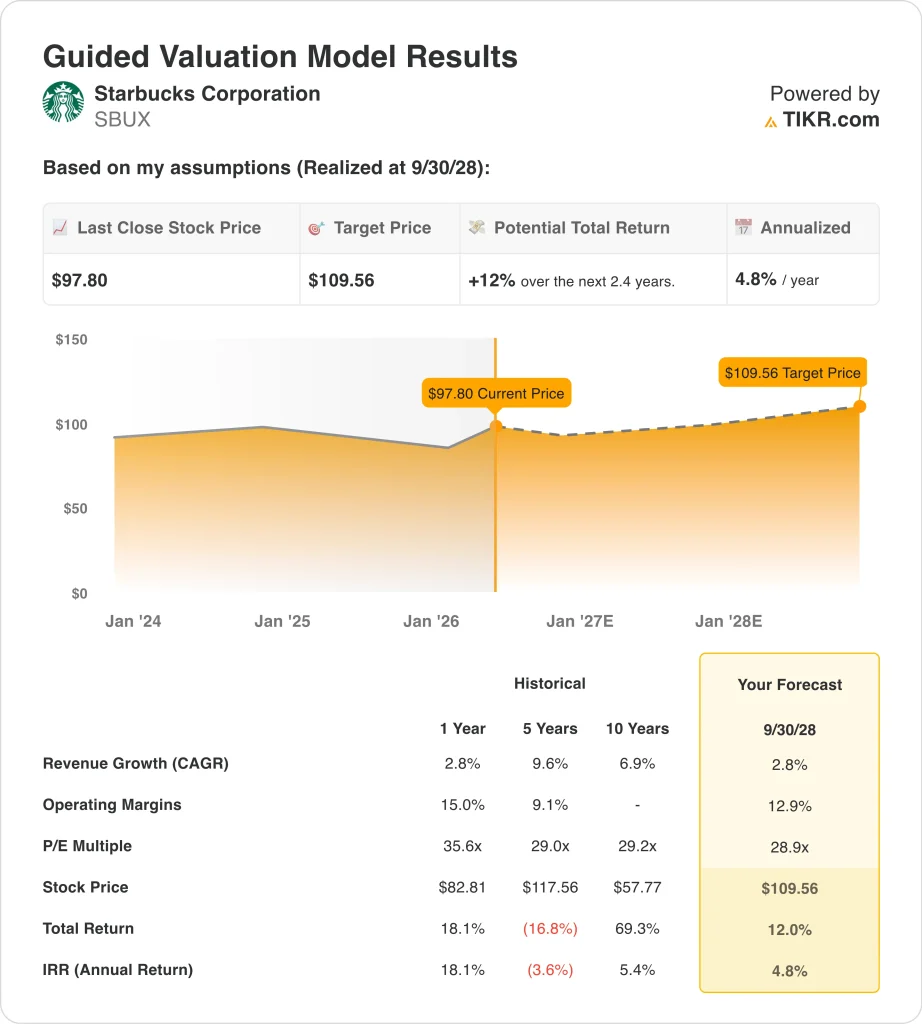

- Starbucks stock could reasonably reach around $110 per share by late 2028, based on the valuation model.

- That implies about a 12% total return from the current price of $98, or roughly 4.8% annualized over the next 2.4 years.

What Happened?

Starbucks Corporation (SBUX) is relevant this week because the company keeps adding new pieces to its turnaround story ahead of its April 28 earnings report. On April 21, it was reported that Starbucks would invest $100 million to establish a corporate office in Nashville, Tennessee, with plans to bring 2,000 support jobs there over the next five years.

The company has also been active in partnerships and shareholder returns. Reuters reported on April 21 that Keurig Dr Pepper and Nestlé USA extended their agreement to manufacture and distribute Starbucks-branded coffee products in the U.S. and Canada.

A few days earlier, Starbucks announced another quarterly cash dividend of $0.62 per share, payable on May 29, 2026, to shareholders of record on May 15, 2026.

The market is still reacting to Starbucks’ last earnings report as well. In Q1 fiscal 2026, revenue rose 6% to $9.9 billion, global comparable sales increased 4%, and the company guided fiscal 2026 non-GAAP EPS to $2.15 to $2.40. But Reuters also noted that the midpoint of that profit outlook sat below analyst expectations, which helped keep investor enthusiasm in check even as U.S. traffic improved.

China remains another major part of the story. Starbucks finalized its joint venture with Boyu Capital in early April, with Boyu-managed funds now holding 60% of Starbucks China retail operations and Starbucks keeping 40%, while the venture oversees about 8,000 stores and carries a long-term goal of expanding to as many as 20,000 locations.

Here’s why Starbucks stock could keep moving from here: investors are weighing whether better U.S. traffic, a reset China structure, and brand strength can offset margin pressure, labor issues, and slower earnings growth.

What the Model Says for Starbucks Stock

We analyzed the upside potential for Starbucks stock using valuation assumptions that reflect modest revenue growth, some margin recovery, and a more normalized earnings multiple.

Based on estimates of around 3% annual revenue growth, around 13% operating margins, and a normalized P/E multiple of around 29x, the model projects Starbucks stock could rise from $98 to $110 per share.

That would be a 12% total return, or a 4.8% annualized return over the next 2.4 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SBUX stock:

1. Revenue Growth: 3%

Starbucks is no longer in a phase where investors expect fast revenue growth every year. Fiscal 2025 revenue was about $37.2 billion, up 2.8% from fiscal 2024, according to the annual report and the figures you provided. That is growth, but it is a much slower pace than Starbucks delivered in earlier expansion periods.

The business is still large enough to grow through multiple channels. Starbucks said fiscal 2025 segment revenue was led by North America at $27.4 billion, followed by International at $7.8 billion and Channel Development at $1.9 billion.

Q1 fiscal 2026 gave investors a better near-term read on demand. Revenue rose 6% to $9.9 billion, global comparable sales increased 4%, and the company ended the quarter with 41,118 stores after opening 128 net new stores.

Based on analysts’ consensus estimates, we use around 3% annual revenue growth because that fits the guided valuation, the company’s mature footprint, and the current mix of steady demand and slower expansion.

2. Operating Margins: 13%

Margins are where the debate becomes more important. Starbucks’ Q1 fiscal 2026 North America operating margin fell to 11.9% from 16.7% a year earlier, while management cited labor investments, tariffs, and elevated coffee pricing as key reasons. That helps explain why the market has treated better traffic with some caution.

There are still parts of the business with stronger profitability. In Q1 fiscal 2026, International operating margin improved to 13.7% from 12.7%, and Channel Development remained highly profitable with a 41.3% operating margin even after a year-over-year decline. Those businesses do not fully offset North America, but they do show Starbucks still has profitable engines inside the broader company.

Based on analysts’ consensus estimates, we use around 13% operating margins. That is close to the guided valuation assumption and implies some improvement from current levels, but not a full return to the stronger margins Starbucks posted before recent restructuring, coffee cost, and labor pressures.

3. Exit P/E Multiple: 29x

The exit multiple in this model stays relatively full because Starbucks remains a premium global consumer brand. Even after the company’s profit pressure, the street mean target in the figures you provided is about $101, and the guided valuation uses a normalized P/E multiple around 29x.

There is also a reason not to be too aggressive. Reuters reported that Starbucks’ fiscal 2026 non-GAAP EPS outlook came in below expectations at the midpoint, and Jefferies lifted its rating only to hold in April on signs of U.S. stabilization and reduced global risk.

Based on analysts’ consensus estimates, we use an exit P/E multiple of around 29x. That multiple recognizes Starbucks’ brand, store base, and dividend profile, while also reflecting that earnings growth has slowed and the turnaround still has more to prove.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for Starbucks stock through 2035 show varied outcomes based on U.S. traffic recovery, China execution, margin rebuilding, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: U.S. sales improve slowly, margin recovery stays limited, and the valuation compresses faster → 5.9% annual returns

- Mid Case: Starbucks stabilizes traffic, rebuilds margins gradually, and grows steadily across stores and partnerships → 8.7% annual returns

- High Case: The turnaround gains traction faster, China execution improves, and earnings compound more efficiently → 11.1% annual returns

The company still has global scale, a valuable brand, and recurring demand, but the market wants proof that traffic gains can rebuild profitability. The next few quarters will likely matter most on U.S. margin trends, China execution under the Boyu venture, and whether “Back to Starbucks” produces more durable earnings progress.

See what analysts think about SBUX stock right now (Free with TIKR) >>>

Should You Invest in Starbucks Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SBUX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SBUX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Starbucks stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!