Key Stats for Vertiv Holdings Stock

- 52-Week Range: $77 to $323

- Current Price: $312

- Street Mean Target: $296

- Street High Target: $370

- TIKR Model Target (Dec. 2030): $567

What Happened?

Vertiv Holdings Co (VRT) designs and manufactures the critical power and thermal infrastructure that keeps data centers running, from uninterruptible power supplies and switchgear to liquid cooling systems and prefabricated data hall solutions.

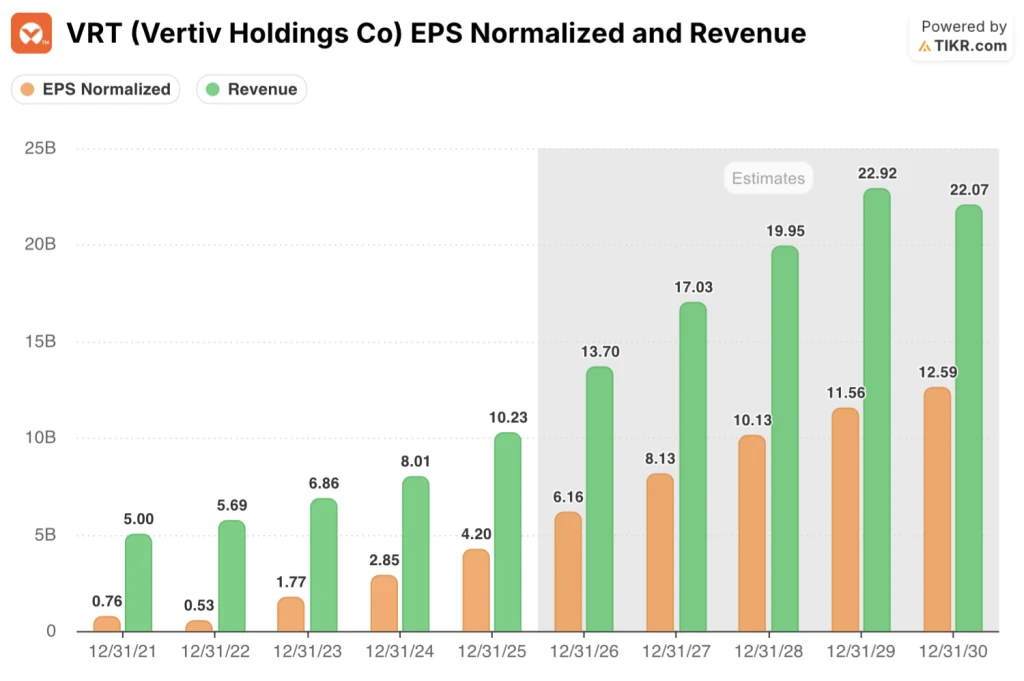

The company closed 2025 with Q4 organic net sales growth of 19% and adjusted diluted EPS of $1.36, up 37% year-over-year and $0.10 above guidance.

The number that stopped analysts mid-question: Q4 organic orders surged 252% year-over-year and 117% sequentially, lifting the total backlog to $15 billion, more than double the prior year.

Vertiv entered 2026 with a $2.1 billion adjusted operating profit in FY2025, up 35% year-over-year, and full-year adjusted free cash flow of approximately $1.9 billion, up 66%.

Management issued 2026 guidance projecting $13.5 billion in net sales at the midpoint, representing 28% organic growth, with adjusted diluted EPS of $6.02, a 43% increase at the midpoint.

CEO Giordano Albertazzi framed the trajectory on the Q4 earnings call: “I’ve never been more excited about Vertiv’s future. We’re leading the industry in orders. We are scaling. We are very well positioned to expand our market leadership and drive the industry forward.”

The manufacturing buildout matches that confidence: in March, Vertiv announced four new or expanded facilities across the Americas, including two South Carolina sites expected to increase regional capacity roughly 7x when fully ramped, plus a Pennsylvania facility focused on AI-specific integrated cooling cabinets.

On March 7, S&P Dow Jones Indices confirmed Vertiv would join the S&P 500, effective March 23, sending shares up nearly 6% in extended trading on the announcement.

Vertiv also closed a $4.6 billion capital markets transaction in early March, a debut $2.1 billion investment-grade bond offering paired with a new $2.5 billion revolving credit facility, replacing the prior $800 million secured facility and retiring the existing term loan in full.

The NVIDIA partnership deepened in March with Vertiv contributing simulation-ready power and cooling designs to NVIDIA’s Vera Rubin DSX AI factory reference architecture, validating Vertiv as the infrastructure layer for next-generation AI factory deployments.

Wall Street’s Take on VRT Stock

The Q4 order result reframes Vertiv stock not as a cycle play but as a structural compounder: when backlog doubles in a year and every regional pipeline continues to grow despite record order intake, the forward revenue trajectory is no longer a forecast.

VRT’s normalized EPS compounded at 47.4% in 2025 to $4.20, and consensus estimates project another 47% step to $6.16 in 2026, followed by 32% growth to $8.13 in 2027, underwritten by a $13.5 billion revenue guide and 22.5% adjusted operating margin guidance.

Twenty-three analysts cover Vertiv at current levels, with 16 Buys and 7 Outperforms against just 4 Holds; the mean price target of $296 sits below the current price of $312, while the high target reaches $370, reflecting a genuine debate about how aggressively to model 2027 and 2028 execution.

The $370 high target versus the $155 low target is not noise: it maps directly to whether EMEA’s H2 2026 pipeline conversion materializes on schedule and whether the Americas capacity buildout translates into revenue without significant margin drag from greenfield ramp costs.

Trading at roughly 51x 2026 consensus EPS and approximately 38x 2027 consensus EPS, Vertiv stock appears fairly valued for investors underwriting the next 12 months, though the EPS ramp from $8.13 in 2027 to $10.13 in 2028 gives long-duration holders a structurally different entry calculus.

The S&P 500 inclusion effective March 23 removed a persistent technical overhang: index funds now hold VRT as a benchmark constituent, reducing forced-seller risk and expanding the passive ownership base.

The key risk is incremental margin delivery: CFO Craig Chamberlin guided 2026 incrementals at the lower end of the 30%-to-35% long-term range, with Q1 the lowest-margin quarter as greenfield capacity in Asia and brownfield expansions in the Americas reach run rate.

Q1 2026 earnings is the catalyst to watch: Chamberlin guided $2.6 billion in Q1 sales at 19% adjusted operating margin, and any upside to that margin exit rate, particularly in Americas, would accelerate the 2026 operating profit walk toward the $3.04 billion full-year target.

What Does the Valuation Model Say?

TIKR’s mid-case model prices Vertiv at $568 by December 2030, anchored to a 15% revenue CAGR from 2025 through 2035 and a 19.2% net income margin, assumptions that Vertiv’s own $13.5 billion 2026 revenue guide and accelerating EMEA pipeline make structurally credible rather than optimistic.

At approximately 51x 2026 consensus EPS with a mid-case target of $568 and EPS projected to reach $10.13 by 2028, Vertiv stock appears fairly valued at today’s price for 12-month holders, while the two-year EPS ramp makes the current multiple substantially more defensible for investors with a longer time horizon.

The question for Vertiv stock is not whether demand is real — a $15 billion backlog of binding purchase orders settles that — but whether the margin ramp from the Americas capacity buildout arrives on the schedule management has set.

Bull Case:

- Americas guided to grow high-30s percent in 2026, consistent with Q4 organic growth of 46%, with $15 billion in binding purchase orders providing near-certain revenue coverage through 2027

- Adjusted operating margin guided at 22.5% for 2026, up from 20.4% in 2025, with management signaling 30%-to-35% long-term incrementals as brownfield and greenfield capacity reaches run rate by year-end

- NVIDIA Vera Rubin DSX partnership and S&P 500 inclusion (March 23) expand both technical credibility and passive institutional ownership, structurally broadening the shareholder base

- ThermoKey acquisition (expected Q2 2026 close) strengthens EMEA thermal management capacity ahead of the H2 2026 pipeline conversion Albertazzi signaled on the earnings call

Bear Case:

- Consensus mean price target of $296 sits below the current price of $312, suggesting the Street is not underwriting the full 2027 EPS ramp at present levels

- EMEA revenue guided flat to down mid-single digits in H1 2026, with recovery dependent on pipeline conversion that has been flagged but not yet delivered in reported sales

- Q1 2026 adjusted operating margin guided at 19%, the lowest quarter of the year, with incremental margins at the lower end of the 30%-to-35% long-term range as new facilities ramp

- China market remains muted with no recovery catalyst named on the earnings call, capping APAC upside to India and the rest of Asia

Should You Invest in X?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up X stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track X alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze X stock on TIKR for Free →