Key Stats for CAVA Stock

- 52-Week Range: $43 to $102

- Current Price: $96

- Street Mean Target: $87

- Street High Target: $110

- TIKR Model Target (Dec. 2030): $278

What Happened?

Cava Group (CAVA) is a fast-casual Mediterranean restaurant chain serving customizable bowls, pitas, and salads priced roughly between $11 and $16, and it ended fiscal 2025 with a milestone no analyst could dismiss.

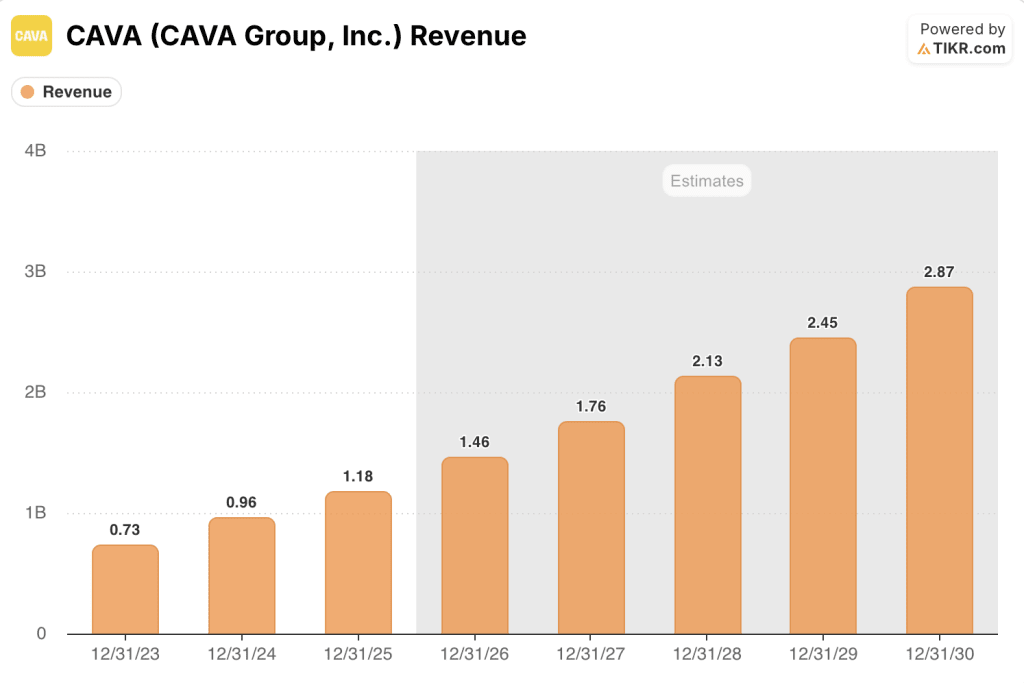

The company crossed $1 billion in annual revenue for the first time, reporting full-year revenue of $1.17 billion, a 22.5% increase over fiscal 2024, driven by 72 net new restaurant openings and same-restaurant sales growth of 4%.

Fourth-quarter results continued that momentum: Q4 revenue reached $272.8 million, a 21.2% year-over-year gain that beat the $267.9 million consensus estimate, and Q4 adjusted EPS of $0.04 topped the $0.03 estimate.

The number that silenced the “slop-bowl fatigue” narrative came from the comps: Q4 same-restaurant sales rose 0.5%, reversing an analyst expectation for a 0.85% decline.

For fiscal 2026, management guided same-restaurant sales growth of 3% to 5%, above the 3.16% Street estimate, projecting 74 to 76 net new restaurant openings and adjusted EBITDA of $176 million to $184 million.

“CAVA remains one of the handful of investable growth concepts in restaurants, with a good degree of visibility into its long-term algorithm and 1,000 stores by 2032 in sight,” said Jefferies following the report.

The expansion story is accelerating into new territory: in March, Cava Group opened its first Ohio restaurant in Cincinnati, followed in April by its first St. Louis-area location in Cottleville, Missouri, lifting the operating base to 29 states plus the District of Columbia.

CEO Brett Schulman confirmed on the Q4 earnings call that the salmon launch, CAVA’s first-ever seafood protein, arrives before the end of Q1, with test results performing slightly better than the Chicken Shawarma offering that drove comp reacceleration in late 2024.

Two structural investments are building quietly: tiered loyalty tiers (Sea, Sand, Sun, and the invite-only Oasis tier) already drive roughly one-third of all revenue, and brand awareness has risen from 55% to 62% over the past year as new market entries compound the network effect.

The company also extended its credit facility in March to 2031 with revolving commitments increased to $150 million, leaving CAVA with $393 million in cash, zero debt, and the runway to fund growth without dilution.

Wall Street’s Take on CAVA Stock

The Q4 beat gave analysts a clean data point to separate the brand’s structural momentum from the short-cycle consumer anxiety that drove the stock down 47% in 2025.

Consensus models CAVA revenue reaching around $1.76 billion in fiscal 2026, roughly 21% above fiscal 2025, then compounding at around 20% annually through fiscal 2030 toward $2.87 billion, making Cava Group one of the fastest-growing restaurant concepts in the Street’s coverage universe.

Of 26 analysts covering CAVA stock, 16 carry buy-equivalent ratings, 12 hold, and 1 sell, with a mean price target of $87 and a high target of $110; the concentration of holds reflects a market where the bull case is well-understood but the stock’s rally has stretched the price above where most models land.

With the stock at $97, nearly every analyst target sits below the current price, meaning the recovery from the $43.41 low has already absorbed the forward growth premium most models assign, leaving CAVA stock appearing overvalued against a backdrop of guided margin compression and a consumer environment where traffic headwinds for discretionary dining persist.

Management guided restaurant-level profit margins of 23.7% to 24.2% for fiscal 2026, below the 24.4% delivered in fiscal 2025, reflecting the 100 basis point headwind from the salmon launch plus ongoing tariff and delivery cost pressure.

The risk is specific: if same-restaurant sales growth comes in below the guided 3% to 5% range, the unit economics that justify the premium multiple deteriorate faster than new openings can offset them.

The catalyst is the Q1 fiscal 2026 earnings release, where the salmon launch’s impact on traffic and average check, alongside comp trajectory versus guidance, will either validate or break the current price.

What Does the Valuation Model Say?

TIKR’s mid-case model projects CAVA reaching a stock price of around $520 by December 2034, anchored to an assumed revenue CAGR of around 18% and net income margins expanding from 5.2% in fiscal 2025 toward around 7%, with improvement supported by the operating leverage that unit density unlocks as the chain approaches the 1,000-restaurant milestone.

At $97, priced above the $87 mean analyst target with margin guidance pointing lower for fiscal 2026, CAVA stock appears overvalued for investors who need the Street’s consensus to provide any near-term cushion.

The entire investment case for CAVA stock hinges on whether the 20%-plus revenue CAGR holds as the restaurant count scales from 439 toward 1,000, or whether comp softness and margin headwinds erode the unit economics that justify trading at a premium to consensus targets.

What Has to Go Right

- Same-restaurant sales sustain above 3% annually, with the salmon launch and tiered loyalty simultaneously driving traffic and average check; salmon test results already came in slightly above Chicken Shawarma benchmarks in early testing

- New restaurant productivity stays near or above 90% as CAVA enters greenfield Midwest markets including Columbus and Minneapolis, keeping new restaurant AUVs above the fiscal 2025 level of $2.9 million

- Brand awareness, up from 55% to 62% over the past year, continues compounding through new market openings, reducing marketing cost per new guest as the footprint scales

- Restaurant-level margins recover toward 25% by fiscal 2027 as tariff and delivery cost pressures normalize and salmon premium pricing offsets the 100 basis point launch headwind

What Could Go Wrong

- Comp growth decelerates below the guided 3% to 5% band due to persistent traffic softness among Gen Z consumers, the cohort CEO Schulman specifically flagged as increasingly sensitive to AI-driven job market uncertainty

- Restaurant-level margins compress further in fiscal 2026 if delivery mix, tariff costs, and AGM wage investments all run above plan, widening the distance from the 25% long-term target rather than narrowing it

- With 12 holds and 1 sell among 26 analysts covering CAVA stock, any Q1 guidance miss triggers multiple compression from a stock already trading above the $87 mean target

- Catering, positioned as a future revenue layer, remains in a two-market test and will not contribute meaningfully to fiscal 2026 results, leaving the growth story fully dependent on unit count and same-restaurant sales velocity

Should You Invest in CAVA Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CAVA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CAVA Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CAVA stock on TIKR for Free →