Key Stats

- Current Price: ~$169

- Q4 FY2026 Revenue: $836M, +16% YoY

- FY2026 Full-Year Revenue: $3.195B

- FY2026 Non-GAAP Operating Income: $1.434B

- FY2027 Subscription Revenue Growth Guidance: ~13%

- TIKR Model Price Target: ~$319

- Implied Upside: ~89% over ~5years (around 14% annualized)

Veeva Systems Stock Closes Out Fiscal 2026 Ahead of Guidance

Veeva Systems stock (VEEV) delivered Q4 FY2026 revenue of $836 million, ahead of guidance, capping a full fiscal year at $3.195 billion.

According to CEO Peter Gassner on the Q4 earnings call, non-GAAP operating income for the quarter came in at $366 million, with full-year non-GAAP operating income reaching $1.434 billion.

The result marked Veeva’s first full year surpassing its $3 billion revenue run rate goal, a milestone Gassner cited directly in his opening remarks.

R&D Cloud was the primary growth driver, with Veeva reporting a top 20 pharmaceutical company standardizing on RTSM and a separate top 20 safety win in the quarter, according to Gassner on the Q4 call.

The company also reported its first top 20 customer going live on the Safety Signal and Workbench product, according to Gassner, marking a meaningful execution milestone in a segment Veeva has called the “safety surge.”

On the commercial side, Vault CRM momentum continued, with approximately 140 customers live on the platform as of the Q4 call, according to EVP of Strategy Paul Shawah.

Shawah confirmed that roughly 14 of the top 20 pharmaceutical companies are expected to end up on Vault CRM, with most decisions already made and remaining commitments expected to finalize over the course of FY2027.

For FY2027, Veeva guided to approximately 13% subscription revenue growth, with management noting tougher Crossix comparables and a mix shift in R&D from mature products like eTMF toward faster-growing but earlier-stage products including RTSM, EDC, safety, and LIMS, according to CFO Brian Van Wagener on the call.

Veeva Systems Stock: What the Income Statement Shows

Veeva Systems stock is backed by an income statement that shows consistent operating leverage building across the past four quarters.

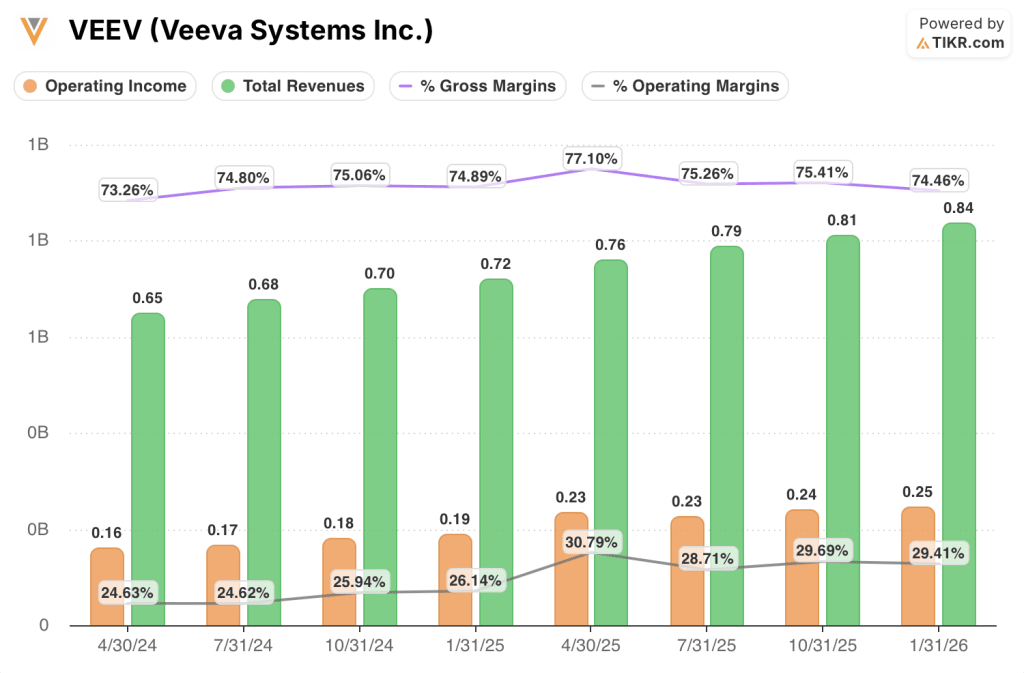

Q4 FY2026 revenue grew 16% year over year to $0.84B, part of a streak of four consecutive quarters of 16% to 17% growth that underpins the operating leverage story below.

Q4 FY2026 gross margin came in at 74.5%, down modestly from 75.4% in Q3 FY2026 and 74.9% in Q4 FY2025, holding within a tight band despite revenue scaling.

Operating income for Q4 FY2026 was $0.25B, up 30.5% year over year from $0.19B in Q4 FY2025.

Operating margin reached 29.4% in Q4 FY2026, compared with 26.1% in Q4 FY2025, representing meaningful year-over-year expansion.

The margin trajectory over the past year is notable: operating margins moved from 30.8% in Q1 FY2026 to 28.7% in Q2, 29.7% in Q3, and 29.4% in Q4, reflecting a broadly stable high-20s operating margin profile even as the company absorbed services headcount for CRM migration activity.

Valuation Model Take and Scenario Breakdown

The TIKR model prices Veeva Systems stock at ~$319, implying roughly 89% total return potential from the current price of ~$169 over approximately 4.8 years, or about 14% annualized.

The mid-case model assumes a 13.0% revenue CAGR and a 40.6% net income margin through 2036, a combination that would require Veeva to sustain its current growth trajectory while expanding margins from today’s GAAP levels.

This quarter’s results support that framework: FY2026 came in ahead of guidance, operating leverage is visible in the income statement, and the R&D Cloud pipeline is gaining scale in high-value product areas.

The investment case for Veeva Systems stock is modestly stronger after this report, not because of a single blowout number, but because the company executed precisely on the transition it committed to: Vault CRM adoption, R&D Cloud penetration into safety and RTSM, and a disciplined services margin profile heading into FY2027.

The central tension for Veeva Systems stock is whether R&D Cloud’s newer products (RTSM, EDC, safety) can scale fast enough to offset Crossix comp headwinds and a maturing CRM base over the next two to three years.

What Has to Go Right

- RTSM standardization deals, like the top 20 enterprise win in Q4, need to replicate across additional pharma majors; RTSM is described by Gassner as comparable in scale to EDC

- Safety momentum, now including a top 20 go-live on Signal and Workbench, must convert into broader platform adoption across the remaining top 20 holdouts

- Vault CRM’s ~140 live customers and 14-of-20 top-pharma trajectory must continue generating cross-sell pipeline for Network, OpenData, and adjacent commercial products

- FY2027 subscription growth guidance of ~13% assumes the mix shift from mature R&D products to early-stage, high-growth products plays out on schedule

What Could Still Go Wrong

- Crossix had an outsized FY2026, and Van Wagener specifically flagged that the same level of outperformance would be surprising to repeat in FY2027, creating a visible top-line comp risk

- EDC penetration has hit what Gassner called “an air pocket,” with timing of top 20 wins harder to predict, introducing lumpiness to R&D Cloud growth

- The 6 top 20 customers still undecided on CRM (with Salesforce as the alternative) represent potential revenue leakage if even one or two land outside Veeva’s projections

- AI agent monetization is not expected to be a material financial contributor in FY2027, according to Van Wagener, leaving the long-term margin upside from Veeva AI in the “out years” with no near-term revenue offset

Should You Invest in Veeva Systems Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VEEV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Veeva Systems Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VEEV stock on TIKR for Free →