Key Stats for United Airlines Stock

- Current Price: $99.56

- Target Price (Mid): ~$171

- Street Target: ~$130

- Potential Total Return (Mid): ~73%

- Annualized IRR: ~7% / year

- Q4 2025 Earnings Reaction: +2.20% (January 20, 2026)

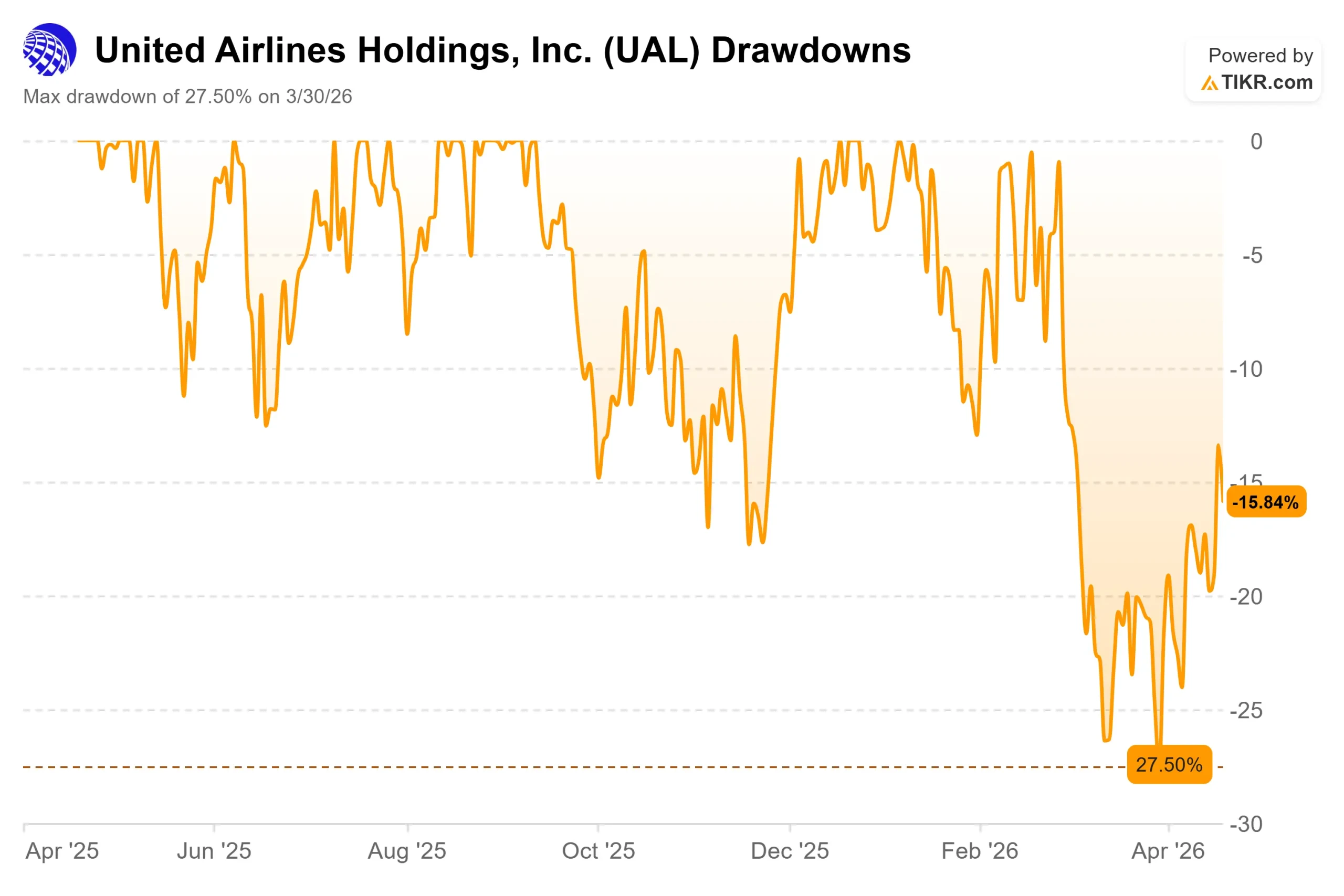

- Max Drawdown: 27.50% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

United Airlines (UAL) has been one of the most event-driven stocks in the S&P 500 this year. After hitting a 27.50% drawdown on March 30, 2026, the stock reversed sharply.

A US-Iran ceasefire framework and the anticipated reopening of the Strait of Hormuz drove crude prices sharply lower, triggering multiple sessions of 7% to 10% gains for United Airlines and its peers.

The stock now trades near $99.56, well off the January 52-week high of $119.21 but meaningfully recovered from the trough.

The problem that caused the selloff has not been solved.

At the JPMorgan Industrials Conference on March 17, 2026, CEO Scott Kirby laid out the fuel math plainly: to fully offset approximately $4.6 billion in higher fuel costs, United needs RASM (revenue per available seat mile, the standard airline unit revenue metric) to rise by 8.5 points, and the first ten weeks of 2026 registered as the ten largest booking weeks in the company’s history.

March RASM was tracking up 14%, reflecting strong underlying demand and the airline industry’s success in passing fuel costs through via fare hikes and international fuel surcharges.

United entered this moment in solid shape. The Q4 2025 earnings release showed adjusted EPS of $3.10, beating the consensus estimate of $2.94, and the stock gained 2.20% on January 20, 2026. CEO Scott Kirby, Chief Executive Officer, said in the press release: “Our results are built on winning more and more brand-loyal customers.”

One wildcard surfaced in mid-April. American Airlines said it was “not interested” in any merger talks with United after Bloomberg reported Kirby had floated a potential combination with American to government officials.

Most analysts view a United-American deal as a regulatory non-starter. The news added noise but has not changed the core investment case.

See historical and forward estimates for United Airlines stock (It’s free!) >>>

Is United Airlines Undervalued Today?

At $99.56, UAL trades at around 10x NTM earnings and roughly 6x NTM EV/EBITDA per TIKR data. The Street mean target of $130.17 across 24 analysts implies around 31% upside from today’s price. That gap between the current price and where analysts think the stock belongs is the whole story.

The bull case rests on a business model shift that the multiple does not fully reflect. United’s MileagePlus loyalty program has over 130 million members, and the revenue it generates through its co-brand credit card partnership with Chase flows in largely independent of ticket prices. Per United’s Q4 2025 earnings release, co-brand remuneration grew 12% for the full year and 14% in Q4, with loyalty revenue up 9% for the year.

That kind of recurring, non-ticket income is qualitatively different from seat revenue, and airline multiples have historically given it limited credit.

The international network reinforces the case. Per TIKR segment data, the Atlantic segment generated $11,647 million in revenue in 2025, and the Pacific segment $6,878 million, both growing year over year. Those high-yield long-haul routes carry margins that low-cost carriers cannot reach.

The balance sheet is the main counterargument. Net debt stood at $19,854 million at year-end 2025, with a net debt to EBITDA ratio of 2.43x per TIKR. Levered free cash flow over the last twelve months was $916 million against a total enterprise value of roughly $51 billion. That is a thin cushion if fuel costs stay elevated. Management is targeting an investment-grade credit rating by late 2026 or early 2027, and a credit upgrade would reduce interest costs and expand the institutional buyer base, but it is not locked in.

The downside scenario is concrete. Kirby told Bloomberg that in a recessionary environment, United’s internal modeling points to EPS of $7 to $9, well below the official 2026 guidance of $12 to $14 per the Q4 2025 earnings release. At 10x earnings on a recession print, downside to the low $70s is a real possibility. That is the risk investors are paying for at today’s multiple.

See how United Airlines performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $99.56

- Target Price (Mid): ~$171

- Potential Total Return: ~73%

- Annualized IRR: ~7% / year

See analysts’ growth forecasts and price targets for United Airlines stock (It’s free!) >>>

The TIKR mid-case model targets approximately $171 by December 31, 2030, representing around 73% total return and an annualized IRR of around 7% per year. The model was built at an entry price of $98.91, close to today’s market price.

Two drivers underpin the mid-case path: continued international network expansion in the Atlantic and Pacific, and growing loyalty and premium cabin revenue. The model assumes a revenue CAGR of around 4% through 2030, with net income margins expanding from 5.9% in 2025 toward around 7% by 2030 as new aircraft lower per-seat costs and debt amortization reduces interest expense.

The high case reaches approximately $206, implying over 100% total return, on around 5% revenue growth and around 7% margins. The low case of approximately $139 assumes closer to 4% revenue growth with margins around 7%, and still represents meaningful upside. The primary risk to any case is sustained elevated fuel costs that RASM growth cannot fully absorb, compressing margins and likely contracting the multiple.

Conclusion

Watch RASM and premium cabin revenue when United reports Q1 2026 results today, April 21, with the earnings call on April 22. If Q1 RASM came in above 10%, the fuel offset story holds, and the bear case loses its primary leg. A RASM print below 8%, or any reduction to the $12 to $14 full-year EPS guidance, would likely send the stock back toward the March lows.

At around 10x forward earnings, with a 130-million-member loyalty program and dominant trans-Atlantic and trans-Pacific route positions, UAL looks more like a macro-pressured franchise than a structurally impaired business. Whether today’s Q1 print confirms that framing is the question.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in United Airlines?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up United Airlines, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Airlines alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze United Airlines on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!