Key Stats for JPMorgan Stock

- Past-Week Performance: -1.3%

- 52-Week Range: $202.2 to $337.3

- Current Price: $283.8

What Happened?

JPMorgan Chase (JPM), the largest U.S. bank by assets, is pressing its competitive advantages across every revenue line simultaneously, with the firm guiding full-year 2026 net interest income to $104.5 billion while trading near $290 after pulling back from a 52-week high of $337.25.

Jamie Dimon launched the American Dream Initiative on March 31, committing JPMorgan to lend $80 billion to small businesses over 10 years and hire 1,000 additional small-business credit officers, expanding its target client base from 7 million to 10 million.

The investment banking and markets engines reinforced the forward case at the February 23 company update, where CIB co-CEO Troy Rohrbaugh guided Q1 2026 investment banking fees up mid-to-high teens year-on-year and markets revenue up mid-teens, building on a 2025 in which the CIB posted 12% revenue growth with record results in markets, payments, and securities services.

Jeremy Barnum, Chief Financial Officer, stated at the February 23 company update that “business volumes, activity and pipelines, all remain very strong,” then confirmed Q1 IB fees could reach high teens “if the quarter remains constructive.”

JPMorgan’s $19.8 billion technology budget, $80 billion small-business lending commitment, $14 billion already deployed in direct lending with capacity to reach $50 billion, and the April 14 Q1 2026 earnings call as the next hard catalyst position the firm to convert its capital surplus of $30 to $40 billion into durable earnings growth across retail, wholesale, and asset management over the next three to five years.

Wall Street’s Take on JPM Stock

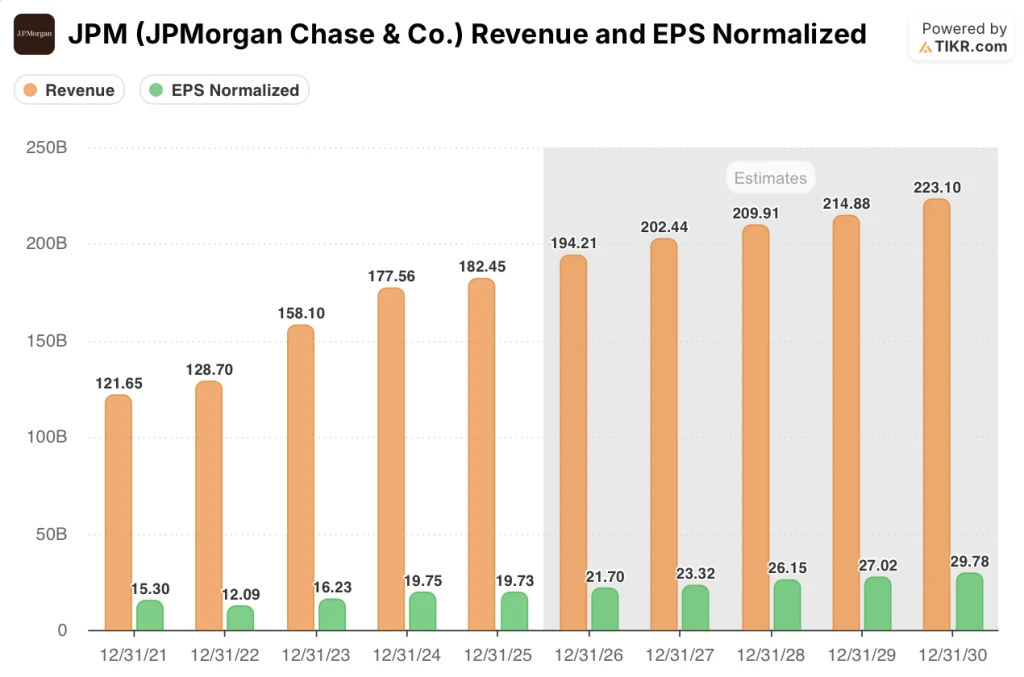

The American Dream Initiative’s $80 billion small-business lending commitment and the $104.5 billion NII guide together confirm that JPMorgan’s 2026 revenue acceleration, estimated at $194.2 billion (+6.4% year-on-year by TIKR), is backed by named, capital-deployed growth vectors rather than macro tailwinds alone.

TIKR estimates normalized EPS reaching $21.70 in 2026 and $23.32 in 2027, anchored by the $80 billion small-business lending program, 160-plus branch openings, and $50 billion direct lending capacity already being deployed across the franchise.

Wall Street’s 24 covering analysts currently carry a mean price target of $340.33, implying 19.9% upside from the March 30 close of $283.77, with 9 buys, 5 outperforms, and 13 holds anchored to Q1 delivery of the mid-to-high teens IB fee and markets revenue growth Rohrbaugh flagged at the February 23 company update.

The spread between the street’s low target of $289 and high of $400 maps directly to two known variables: the $289 floor assumes Iran conflict disruption persists and private credit markdowns widen, while the $400 ceiling assumes Q1 IB fees hit high-teens and the EA and Qualtrics debt syndications clear without further blockage.

What Does the Valuation Model Say?

TIKR’s mid-case model prices JPM at $388.77 by December 2030, assuming a 3.9% revenue CAGR and a 30.1% net income margin, both supported by the $50 billion direct lending capacity buildout and the 160-plus branch openings confirmed for 2026.

At 13.1x 2026E EPS of $21.70, JPM trades at a discount to its own 5-year average forward P/E of approximately 14x while delivering a 5.9% EPS CAGR mid-case — fairly valued to modestly undervalued given the scale of confirmed capital deployment.

The $80 billion small-business lending program, $14 billion already deployed in direct lending, and 1,000 front-office hires in 2025 are the operational developments TIKR’s 3.9% revenue CAGR assumes, and the TIKR mid-case target of $388.77 reflects a 37% total return over 4.7 years at a 6.8% IRR.

Dimon’s February 23 confirmation that excess capital sits at $30 to $40 billion above regulatory minimums, with deployment accelerating organically through SRI and direct lending, signals this is a franchise reinvesting at scale, not drifting toward multiple compression.

If the Iran conflict extends materially beyond Q2 and the Qualtrics and EA debt syndications stall, CIB revenue would miss its mid-to-high teens Q1 guide, breaking TIKR’s 6.4% 2026 revenue growth assumption and compressing the forward multiple.

The April 14 Q1 2026 earnings call is the single confirming event: watch IB fees for mid-teens delivery and card net charge-off rate against the 3.4% full-year guide, as both directly validate TIKR’s EPS and margin trajectory.

Should You Invest in JPMorgan Chase & Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up JPM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track JPMorgan Chase & Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze JPM stock on TIKR for Free →