Key Stats for Danaher Stock

- Past week’s performance: -1.5%

- 52-week range: $171 to $243

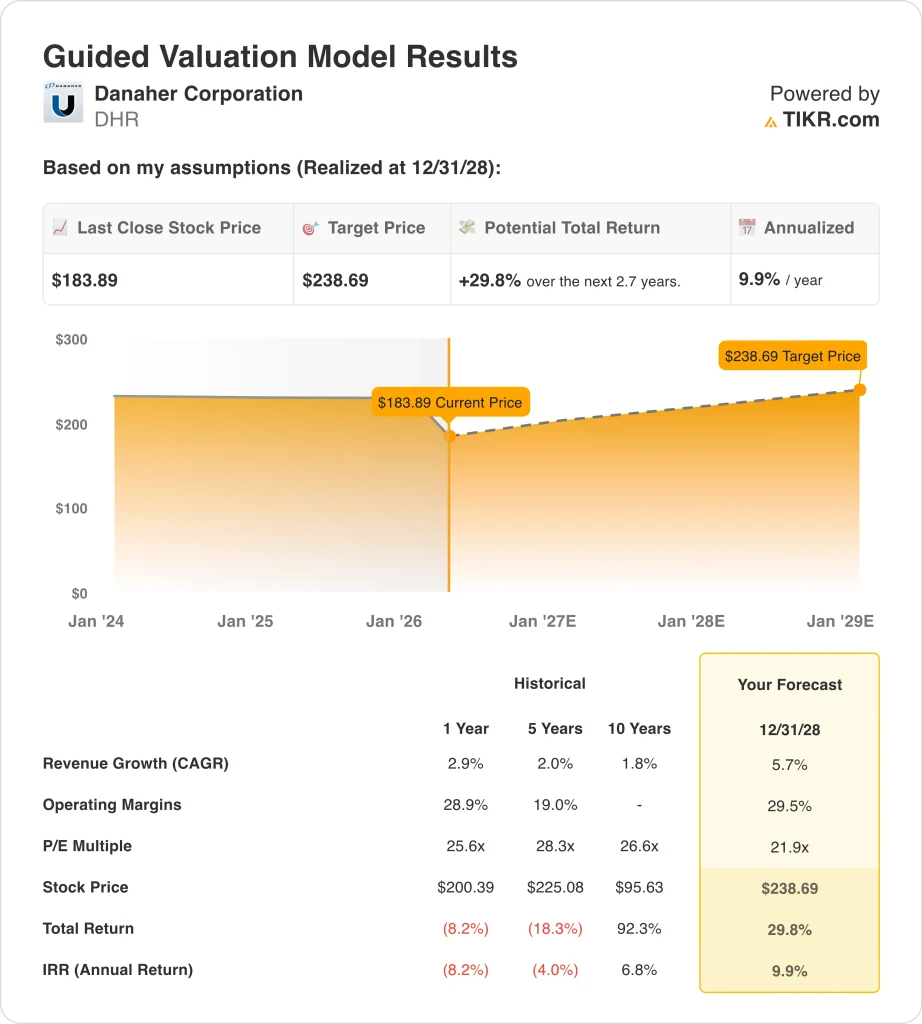

- Valuation model target price: $239

- Implied upside: 29.8% over 2.7 years

Value your favorite stocks like DHR with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Danaher Corporation (DHR) stock slipped 1.5% over the past week, but the bigger move is the 19.7% drop so far in 2026. This week itself was relatively quiet, with the company publishing its annual report on March 25 and paying its $0.40 quarterly dividend on March 27.

That means the recent weakness looks more tied to investor positioning and the broader Danaher story than to a fresh operational surprise.

The main story still hanging over the stock is Danaher’s February agreement to buy Masimo for $180 per share in cash, or about $9.9 billion including debt. Reuters reported that the deal surprised analysts because Masimo pushes Danaher further into patient monitoring, which sits outside the company’s more familiar life sciences tools focus.

Danaher shares fell nearly 3% on the day of that announcement, which showed investors were rethinking the company’s acquisition path.

At the same time, Danaher’s most recent earnings were solid, but not strong enough to erase those concerns. The company reported fourth-quarter 2025 adjusted EPS of $2.23 on revenue of $6.8 billion, both ahead of consensus, and it said full-year 2026 core revenue should rise 3% to 6%. Still, that outlook points to steady recovery rather than a sharp rebound, so the market has kept the stock in a wait-and-see mode.

Management has tried to frame the setup positively. CEO Rainer Blair said the company saw “continued strength in our bioprocessing business” and “improved momentum in Diagnostics and Life Sciences.” Even so, investors still seem focused on whether Danaher can turn that gradual recovery into faster growth while also absorbing a large acquisition.

See analysts’ growth forecasts and price targets for DHR (It’s free) >>>

Is Danaher Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 5.7%

- Operating Margins: 29.5%

- Exit P/E Multiple: 21.9x

Based on these inputs, the model estimates a target price of $238.69, implying 29.8% total upside from the current share price and a 9.9% annualized return over the next 2.7 years.

The valuation suggests some upside, but it is not an obvious bargain. A 9.9% annualized return sits right around the level where a stock starts to look interesting, but it is not high enough to ignore execution risk.

The revenue assumptions are fairly measured. Based on analysts’ consensus estimates, we use 5.7% revenue growth, and that is above Danaher’s 2.9% revenue growth in 2025 but still below the company’s longer-term historical growth profile shown in the valuation image.

That makes sense because Danaher is coming off a weaker stretch in life sciences demand, even though management is guiding for a gradual improvement in 2026.

Margins are the other key piece of the story. Danaher’s LTM EBIT margin is 21.9%, while the valuation model assumes operating margins reach 29.5% by 2028. That kind of improvement would need a stronger mix, better bioprocessing utilization, and continued operating discipline across Diagnostics, Life Sciences, and Biotechnology.

The balance sheet gives Danaher room to pursue that plan, but the Masimo deal raises the bar. Danaher ended 2025 with $15.1 billion of net debt, and the Masimo acquisition is expected to add to earnings over time, including about $0.15 to $0.20 in the first full year after close and about $0.70 by year five.

So, the stock’s valuation now depends less on financial flexibility alone and more on whether the acquisition actually lifts growth and margins the way management expects.

What’s Driving DHR Stock Going Forward?

The next major catalyst is first-quarter 2026 earnings on April 21. Danaher has said first-quarter core revenue should grow at a low-single-digit rate, so investors will be watching whether bioprocessing, diagnostics, and life sciences all track in line with that plan.

The Masimo acquisition is the other big driver. Danaher said Masimo will sit inside the Diagnostics segment alongside businesses like Radiometer, Cepheid, Leica Biosystems, and Beckman Coulter Diagnostics.

If the company can show that patient monitoring broadens its hospital relationships and supports recurring revenue, the market may become more comfortable with the strategy.

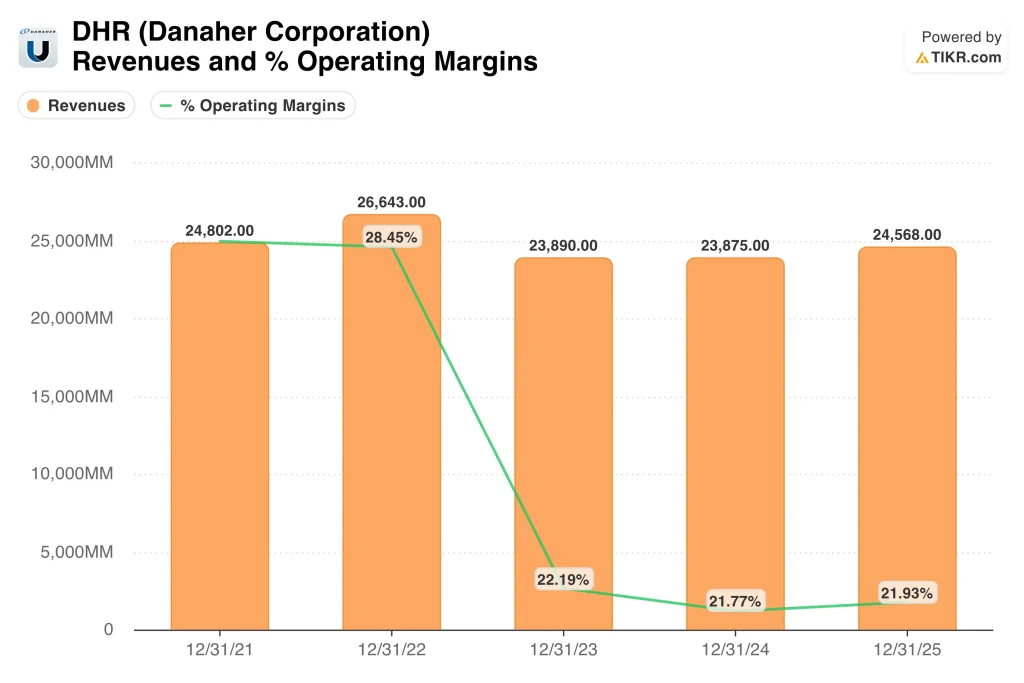

Bioprocessing still matters a lot, too. Danaher’s 2025 results showed revenue of $24.6 billion, adjusted EPS of $7.80, and free cash flow of $5.3 billion, so the business is still highly cash generative even during a slower demand period.

The forward setup is therefore pretty straightforward. Danaher needs to show that its core businesses are recovering, while the Masimo deal strengthens diagnostics without diluting returns.

If those two pieces start working together, the stock can support a higher multiple again, but if growth stays muted, the shares may continue to trade as a high-quality company stuck in a transition year.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Danaher Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DHR, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DHR alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Danaher stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!