Key Stats for Illumina Stock

- 52-Week Range: $69.8 to $155.5

- Current Price: $120.9

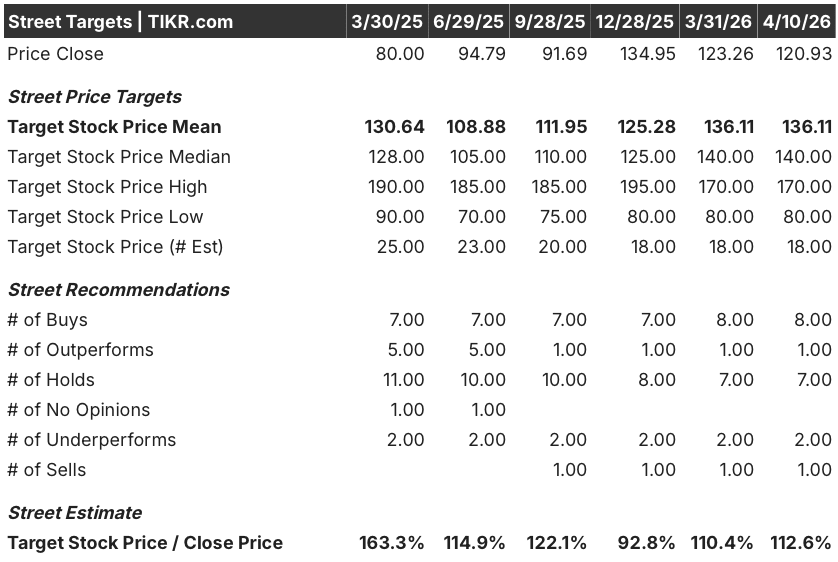

- Street Mean Target: $136.1

- Street High Target: $170

- TIKR Model Target (Dec. 2030): $199.4

What Happened?

Illumina (ILMN), the dominant provider of next-generation sequencing (NGS) platforms used in cancer diagnostics, rare disease testing, and drug discovery, returned to meaningful earnings growth in fiscal 2025 with normalized EPS climbing to $4.84, up 97.6% year-over-year, even as Illumina stock trades more than 22% below its 52-week high. Q4 revenue hit $1.16 billion, a 5% year-over-year gain, beating analyst expectations of $1.10 billion on stronger-than-expected clinical consumables demand.

The clearest single driver of that beat was clinical consumables revenue growing 20% ex-China in Q4, powered by the NovaSeq X, Illumina’s flagship high-throughput sequencing platform launched in 2023, which processes DNA samples faster and at lower cost per genome than its predecessor, the NovaSeq 6000.

Illumina’s installed base of NovaSeq X instruments reached 890 globally by the end of Q4, with placements representing the second-highest quarterly total since the platform’s launch, while total sequencing gigabase output on connected high- and mid-throughput instruments grew more than 30% year-over-year.

Jacob Thaysen, Chief Executive Officer, stated on the Q4 2025 earnings call that “the momentum we have built going into 2026 gives me high confidence that the strategy we put in place in 2024 to return to long-term growth is working,” pointing specifically to mid-teens clinical consumables growth expected in 2026 and a clear trajectory toward the company’s 26% operating margin target by 2027.

Illumina also completed the $350 million acquisition of SomaLogic in January 2026, a proteomics company whose SomaScan platform can simultaneously measure more than 9,500 proteins in a single experiment, and announced a strategic expansion of its Labcorp collaboration in March 2026 to broaden access to precision oncology testing, both of which extend Illumina’s multiomics platform well beyond core DNA sequencing.

Wall Street’s Take on ILMN Stock

The earnings inflection Illumina delivered in 2025 changes the forward story: normalized EPS of $4.84 represents the strongest earnings the company has produced since before its costly GRAIL acquisition distorted results, and it arrived while the research segment was still in decline, meaning the recovery thesis hasn’t yet fully priced in the upside.

Consensus estimates project Illumina stock’s normalized EPS growing from $4.84 in 2025 to $5.12 in 2026 and $5.83 in 2027, anchored by the company’s own guidance of $5.05 to $5.20 for 2026 and the continuing expansion of clinical consumables, which drove 20% ex-China growth in Q4 2025 and management expects to sustain at double-digit to mid-teens rates through 2026.

Nine of 18 analysts covering ILMN carry a buy or outperform rating, with 7 holds and 3 underperforms or sells; the mean price target of $136.11 implies approximately 12.6% upside from the current price of $120.93, but the median target of $140.00 and the presence of a $170.00 high target suggest meaningful conviction among the more bullish cohort as clinical volumes scale.

The spread from $80.00 to $170.00 in street targets maps directly onto two unresolved questions: whether NIH-funded research volumes recover faster than guidance assumes, and whether Roche’s competitive AXELIOS sequencing launch materially disrupts Illumina’s share in the research segment during the transition year.

Trading at roughly 23.6x forward 2026 normalized EPS of $5.12, and with EPS expected to compound at 10.3% annually through 2030 per consensus, Illumina stock appears undervalued given that comparable genomics and life science tools platforms have historically commanded 30x-plus forward multiples during periods of accelerating clinical volume growth.

At the TD Cowen Health Care Conference on March 3, 2026, Thaysen stated that “Illumina will be able to grow very strongly going forward, at least high single-digit growth even in a very competitive space,” a direct reframe of the market’s residual concern that Roche’s entry would compress Illumina’s pricing power in key research segments.

A funding freeze in U.S. academic institutions, if deeper or longer than guidance assumes, would pressure the research consumables segment further, compressing the revenue bridge that supports the 2027 high-single-digit growth target.

Q1 2026 results on April 30 are the first concrete test: consensus expects revenue of $1.06 billion to $1.08 billion and EPS of $1.02 to $1.07, and any deviation in clinical consumables growth will either validate or reset the 2026 full-year thesis.

Illumina Stock Financials

Illumina’s operating income recovered sharply in fiscal 2025, reaching $870 million and representing a 20.0% operating margin, up from $400 million and a 9.1% margin in fiscal 2024 as SG&A expenses fell from $1.39 billion to $1.16 billion and R&D rationalization continued to take hold.

The gross margin story is more nuanced: ILMN posted 68.2% gross margins in fiscal 2025, essentially flat with fiscal 2024’s 68.4% and well below the 71.3% achieved in fiscal 2022, reflecting the structural cost of transitioning a large installed base from the NovaSeq 6000 to the NovaSeq X platform, where consumables pricing is lower per run but volume growth is expected to compensate.

The trajectory is directionally encouraging nonetheless: total operating expenses contracted from $2.59 billion in fiscal 2024 to $2.10 billion in fiscal 2025, a $490 million improvement, driven almost entirely by the multi-year cost reduction program that Illumina began executing in 2023 following the GRAIL spin-off.

The one tension in the income statement is that gross profit declined slightly in absolute terms from $2.99 billion in fiscal 2024 to $2.96 billion in fiscal 2025, meaning operating income expansion has been driven primarily by opex cuts rather than top-line gross profit growth. Until clinical consumables volume is sufficient to lift gross profit back toward fiscal 2022 levels, operating leverage will remain partially constrained.

What Does the Valuation Model Say?

The TIKR mid-case model prices Illumina at $199.38 by December 2030, embedding a 5.5% revenue CAGR from 2025 through 2031, a net income margin expanding to 22.3%, and an EPS CAGR of 10.3%, assumptions grounded in the clinical consumables growth trajectory and the 180 basis points of operating margin expansion Illumina delivered in 2025 alone.

Illumina stock appears undervalued at current levels, trading at roughly 23.6x 2026 consensus EPS against a model that implies a $199 target by 2030 and a 64.9% total return from today’s price.

The real question for Illumina is whether clinical volume growth can carry the thesis as research spending remains depressed. At $120.93, the stock is pricing in a scenario where that growth is modest and the research headwind is persistent.

Low Case / High Case

The low and high cases diverge on two variables: research market recovery speed and the pace of clinical consumables scaling, both of which management has quantified in guidance.

Low Case ($163.17 by 2030 | 5.0% revenue CAGR | 34.9% total return)

- Research consumables remain down mid-to-high single digits annually through 2026 and beyond, with NIH funding uncertainty continuing to suppress academic instrument placements

- NovaSeq X placements hold at 50 to 60 per quarter but clinical consumables growth decelerates from 20% to low double digits as the installed base matures and conversion effects dissipate

- SomaLogic dilutes EPS by $0.18 in 2026 with limited revenue contribution before 2027, pressuring margin improvement

- Roche captures 10% to 15% of addressable research whole-genome market over two to three years, slowing Illumina’s high-throughput volume ramp

- Revenue reaches $4.54 billion in 2026 at the low end of guidance, with operating margin expansion limited to 130 basis points

High Case ($237.34 by 2030 | 6.1% revenue CAGR | 96.3% total return)

- NIH budget clarity improves research spend in the second half of 2026, returning mid-throughput consumables to flat or modest growth and supporting instrument placements above 60 per quarter

- Clinical consumables sustain mid-teens growth as whole-genome sequencing adoption accelerates in oncology MRD and genetic disease, driving higher sequencing intensity per instrument

- TruPath Genome ($395 per genome list price, launched February 2026) captures share in clinical whole-genome workflows by eliminating library prep preparation, delivering structural cost advantages that Roche’s AXELIOS cannot match on workflow simplicity

- SomaLogic integration contributes 1.5% to 2.0% of revenue growth in 2026 as planned, with proteomics cross-sell to the existing NGS customer base beginning to gain traction

- BioInsight Billion Cell Atlas pharma partnerships (AstraZeneca, Merck, Eli Lilly) convert into subscription revenue contracts beginning in 2027, adding the 1% to 2% growth from new multiomics and data initiatives that management has projected

Should You Invest in Illumina, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ILMN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Illumina, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ILMN stock on TIKR for Free →