Key Stats for Nucor Stock

- 52-Week Range: $105.9 to $196.9

- Current Price: $186.1

- Street Mean Target: $186.4

- Street High Target: $210

- TIKR Model Target (Dec. 2030): $239.3

What Happened?

Nucor Corporation (NUE), North America’s largest steel producer by capacity, is entering a structural earnings inflection after spending $20 billion since 2020 to modernize its mill fleet, and Q1 2026 guidance of $2.70 to $2.80 per diluted share signals that inflection is arriving faster than the market has priced in.

The company reported Q4 2025 adjusted EPS of $1.73, missing the $1.91 consensus, as lagging sheet contract prices held back what was otherwise a volume-recovery quarter — and the stock currently trades at $186.12, less than 1% above its 52-week high of $105.92.

Jefferies and Wells Fargo both raised Nucor stock price targets in early April, with Wells Fargo lifting its target to $194 and reiterating an overweight rating, citing a self-sufficient U.S. steel market now shielded by 50% tariffs on imports.

Steel mill backlogs entered 2026 up 40% year-over-year, a tangible signal that the demand side of the equation is catching up to the capacity Nucor built.

The Q1 guidance midpoint of $2.75 per diluted share represents more than a 3x increase from the prior-year comparable, when Q1 2025 EPS came in at $0.77, underscoring how dramatically the pricing and volume environment has shifted.

CEO Leon Topalian even stated on the Q4 2025 earnings call that “we entered the year with historically strong backlogs, up nearly 40% year-over-year in the steel mills segment and 15% in steel products,” tying record structural order depth to Nucor’s sustained nonresidential and infrastructure exposure.

Looking 3 to 5 years out, Nucor’s West Virginia sheet mill (set for late 2026 completion), its $4 billion buyback authorization, four new facilities ramping to positive EBITDA in 2026, and a $500 million projected EBITDA uplift from recently completed projects position the company to target its November 2022 Investor Day through-cycle EBITDA figure of $6.7 billion as West Virginia reaches full run rate.

Wall Street’s Take on NUE Stock

The Q4 miss obscured the more important story: Nucor stock’s forward earnings picture is undergoing a step-change, and the Street has been slow to reprice it.

Consensus estimates show NUE’s normalized EPS accelerating from $7.71 in 2025 to $12.57 in 2026 (up 63.1%), driven by the combination of higher realized sheet prices, a 5% increase in planned steel mill shipments, and the incremental EBITDA from four capital projects that reached completion in 2025.

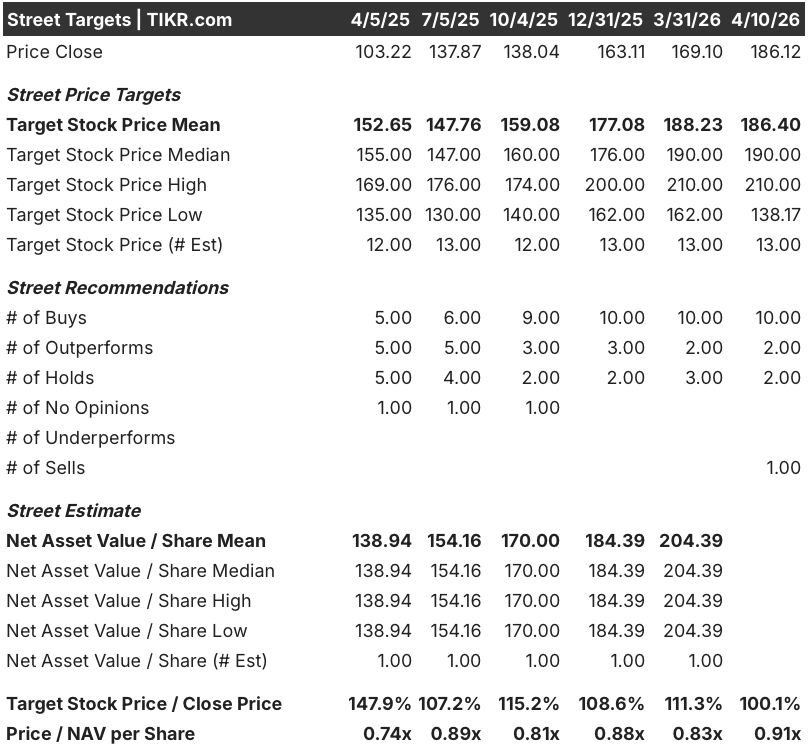

Ten analysts rate NUE a buy, two rate it outperform, two hold, and one sells — a mean price target of $186.40 against a current price of $186.12, implying the consensus is essentially pricing in zero near-term upside, with the most optimistic target sitting at $210.

The spread from $138 to $210 reflects genuine disagreement about whether 50% tariffs on imported steel are durable policy or a negotiating chip, and the answer to that question is the single variable that most determines whether 2026 earnings beat or miss the $12.57 consensus.

Trading at roughly 14.8x 2026 estimated EPS of $12.57 against a 5-year historical average P/E closer to 17x during comparable margin expansion periods, Nucor stock appears undervalued given the magnitude of the earnings acceleration the backlog data supports.

The risk is policy reversal: a February report suggesting the Trump administration was reviewing tariff rollbacks sent NUE down more than 5% intraday, confirming that tariff durability is the load-bearing assumption in every bull model.

The catalyst to watch is the Q1 2026 earnings release: a beat above the $2.80 guidance ceiling, combined with continued sheet price strength, would be the first concrete evidence that the earnings inflection has cleared the theoretical phase and entered the realized one.

Nucor Stock Financials

Nucor’s revenue recovered 5.7% to $32.49 billion in 2025 after a two-year contraction that cut the top line from $41.51 billion in 2022 to $30.73 billion in 2024, establishing a base from which the 2026 consensus estimate of $36.08 billion represents the steepest revenue reacceleration in four years.

The more pressing story is in the margin structure: gross profit fell from $12.53 billion (30.2% gross margin) in 2022 to $3.91 billion (12.0%) by 2025, a compression of nearly 19 percentage points that explains why the stock spent most of 2024 and early 2025 trading in the $103-to-$138 range despite the company’s scale advantage.

Operating income traced an identical arc, declining from $10.41 billion (25.1% operating margin) in 2022 to $2.66 billion (8.2%) in 2025, yet the direction in Q1 2026 is the point — Q1 guidance of $2.70 to $2.80 in EPS, driven by higher sheet prices and volume ramp on four newly completed facilities, implies operating income is expanding sequentially in a way the annual chart does not yet show.

The tension worth naming: gross margins have compressed from 30.2% to 12.0% over three years, and while the 2026 revenue recovery is real, margin restoration to anywhere near historical peaks would require sustained tariff protection and full ramp of West Virginia’s higher-value automotive and galvanized sheet output (targeted for late 2026 commissioning).

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $239.30 is built on a 4.1% revenue CAGR through 2030 and a net income margin of 8.3%, both conservative assumptions against a backdrop where Nucor’s four newly ramped facilities are expected to add roughly $500 million in incremental EBITDA in 2026 alone and West Virginia’s exposed-automotive and galvanized sheet lines represent a premium product mix shift the historical margin profile does not fully capture.

NUE appears undervalued at current levels, trading at roughly 14.8x 2026 consensus EPS while the TIKR model implies a 5-year total return of 28.6% at conservative growth inputs — a gap that only closes if either the earnings acceleration stalls or tariff policy reverses materially before West Virginia reaches run rate.

The central tension for Nucor stock is not whether earnings will recover in 2026 — the backlog data and Q1 guidance make that close to certain — it is whether the 2026 inflection is a one-year tariff-driven event or the beginning of a structurally higher earnings floor built on premium product mix, import displacement, and operating leverage.

Low Case: $196.20

- Revenue growth holds at 3.7% CAGR; net income margin reaches only 7.8%

- Tariff rollbacks (reported in February as under review) suppress HRC prices back toward $800/ton, limiting sheet segment pricing power

- West Virginia ramp slower than guided; pre-operating costs of $496 million in 2025 persist at elevated levels into 2027

- NUE EPS in 2026 comes in at or below consensus $12.57; P/E multiple stays compressed at 14x to 15x

- IRR of 1.1%/year through 2030: total return barely exceeds inflation

Mid Case: $239.30

- Revenue reaches $36.08 billion in 2026 (11.0% growth) on 5% shipment volume increase and sustained sheet prices above $900/ton

- $500 million EBITDA uplift from four completed capital projects begins flowing in H1 2026; Lexington and Kingman rebar micro mills hit positive EBITDA by end of Q1

- West Virginia commissions on schedule late 2026, opening 1 million tons of galvanizing capacity and a new exposed-automotive customer base

- EPS normalized reaches $12.57 in 2026 and $13.88 in 2027; $4 billion buyback authorization shrinks share count at $186-level prices

- IRR of 5.5%/year through 2030: 28.6% total return

High Case: $283.32

- Net income margin expands to 8.6%; revenue CAGR reaches 4.5% on tariff durability through USMCA renegotiation in July and sustained import share below 15%

- Full West Virginia ramp accelerates Nucor’s sheet mix toward exposed automotive and appliances, segments where EAF producers have not previously competed and where pricing premiums are structural

- EBITDA approaches the $6.7 billion through-cycle target from the November 2022 Investor Day; P/E re-rates toward 17x to 18x historical average at equivalent growth

- IRR of 9.3%/year through 2030: 52.2% total return

Should You Invest in Nucor Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NUE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Nucor Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NUE stock on TIKR for Free →