Key Stats for Snowflake Stock

- Past week’s performance: -2.2%

- 52-week range: $118 to $281

- Valuation model target price: $202

- Implied upside: +43% over 2.7 years

Value your favorite stocks like SNOW with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Snowflake (SNOW) has lost about 35.7% year to date in 2026, and several factors drove that decline together. A shareholder class action lawsuit filed in late April alleged the company misrepresented its consumption revenue growth. Consumption revenue is the amount customers pay based on how much data they actually process. That filing added more pressure to shares already under stress.

The pressure began with Q4 FY2026 earnings reported in late February. Snowflake posted Q4 product revenue of $1.23B and full-year revenue of $4.68B, up 29%. But the company also reported a net loss of $1.33B for the full fiscal year. Investors began questioning whether rapid growth alone could justify the stock’s historically high valuation.

The broader AI software selloff in April also hit Snowflake hard. Concerns shifted from AI capability toward AI cost efficiency, and that weighed on premium-valued software stocks. Snowflake named Jonathan Beaulier as Chief Revenue Officer in April, replacing Mike Gannon. So investors added that leadership transition to the growing list of near-term uncertainties.

The company also expanded Snowflake Intelligence and Cortex Code to power what it calls the agentic enterprise. Agentic AI refers to systems that act autonomously on behalf of users without constant human input. But those product developments have not yet led to a stock price recovery. Going forward, the May 20 Q1 FY2027 earnings call is the most important near-term test.

See analysts’ growth forecasts and price targets for SNOW (It’s free) >>>

Is Snowflake Stock Undervalued?

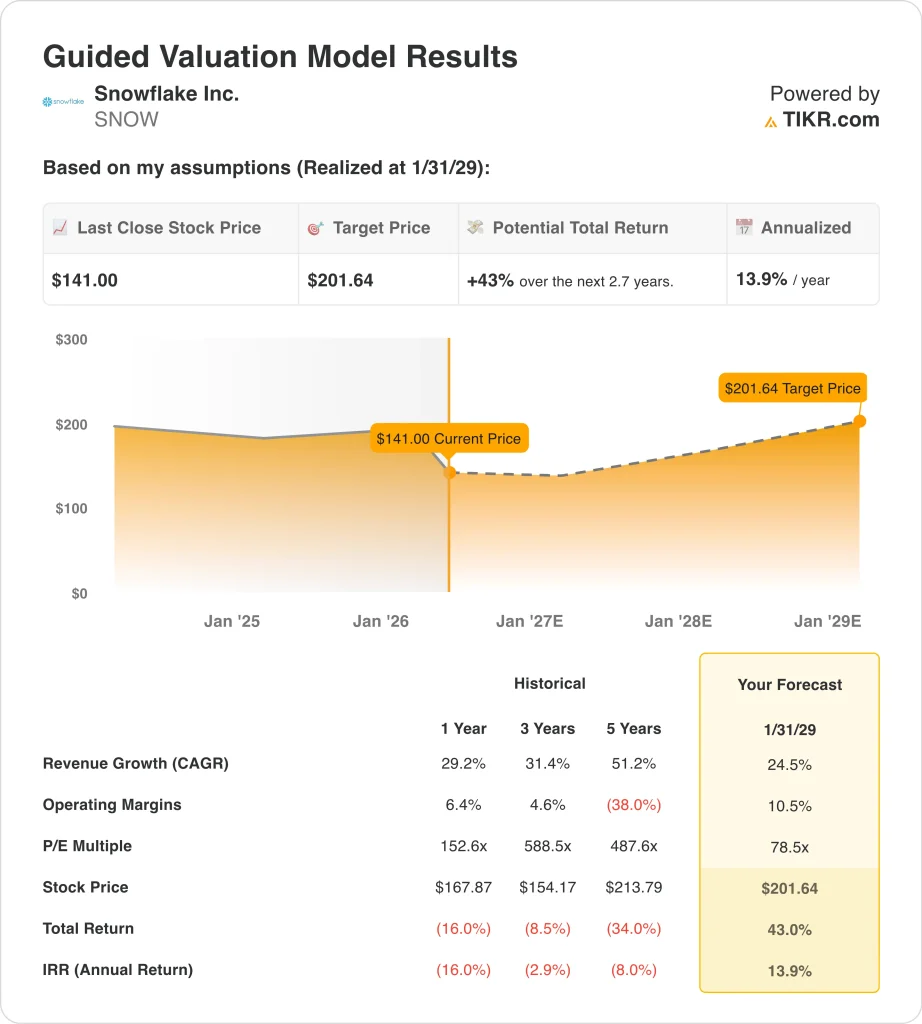

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 24.5%

- Operating Margins: 10.5%

- Exit P/E Multiple: 78.5x

Based on these inputs, the model estimates a target price of $202, implying 43% total upside from the current share price and a 13.9% annualized return over the next 2.7 years.

Snowflake’s stock at $141 sits near the lower end of its 52-week range of $118 to $281. So the entry point looks more attractive than it did during 2024 and early 2025. The analyst consensus target sits at $233, suggesting meaningful upside from current levels. But reaching that target requires execution on a difficult margin improvement story.

The 24.5% revenue growth assumption relies on Snowflake’s cloud data platform expanding into more enterprise AI use cases. Its consumption-based model means revenue scales naturally as customers process more data over time.

But reaching 10.5% operating margins represents a major turnaround from recent deeply negative levels. That improvement depends heavily on disciplined cost management as the company scales.

The 13.9% annualized return puts this model in the attractive range, and institutional holders have taken notice. Investors are paying about 7.9x next year’s expected revenue for the stock, which reflects high growth expectations.

The exit P/E of 78.5x still prices in significant growth at the end of the forecast period. And the ongoing class action lawsuit adds an unquantifiable legal risk that keeps some investors on the sidelines.

What’s Driving SNOW Stock Going Forward?

The most immediate catalyst is the Q1 FY2027 earnings report on May 20. Analysts expect continued strong product revenue growth, and consumption trend commentary will set the tone. A guidance beat could help the stock recover part of its year-to-date losses. But a miss would likely extend selling pressure into the summer.

Snowflake Summit 2026 starts June 1 in San Francisco, and it is a major annual product showcase. The company is expected to highlight its agentic AI strategy and new Cortex Code capabilities.

So the summit is a key opportunity to rebuild investor confidence in the product roadmap. Large enterprise customers attend, and new contract announcements often follow closely after the event.

The ongoing class action lawsuit covers alleged misstatements from June 2023 through February 2024. Litigation timelines are unpredictable, and the case could take several years to resolve. So legal overhang will likely limit the multiple expansion the stock could otherwise achieve.

Institutional investors like BlackRock and Vanguard have recently increased their positions, suggesting long-term confidence despite near-term noise.

Macro conditions also play a meaningful role, because enterprise cloud spending has been cautious in a higher-rate environment. Snowflake’s consumption model benefits directly when customers run more AI workloads on the platform.

So, a renewed wave of enterprise AI investment could be a strong tailwind for the second half of 2026. Management’s commentary on customer demand and budget cycles will be closely watched after May 20.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Snowflake?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SNOW, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SNOW alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Snowflake stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!