Key Stats for Carvana Stock

- Past week’s performance: -6%

- 52-week range: $253 to $487

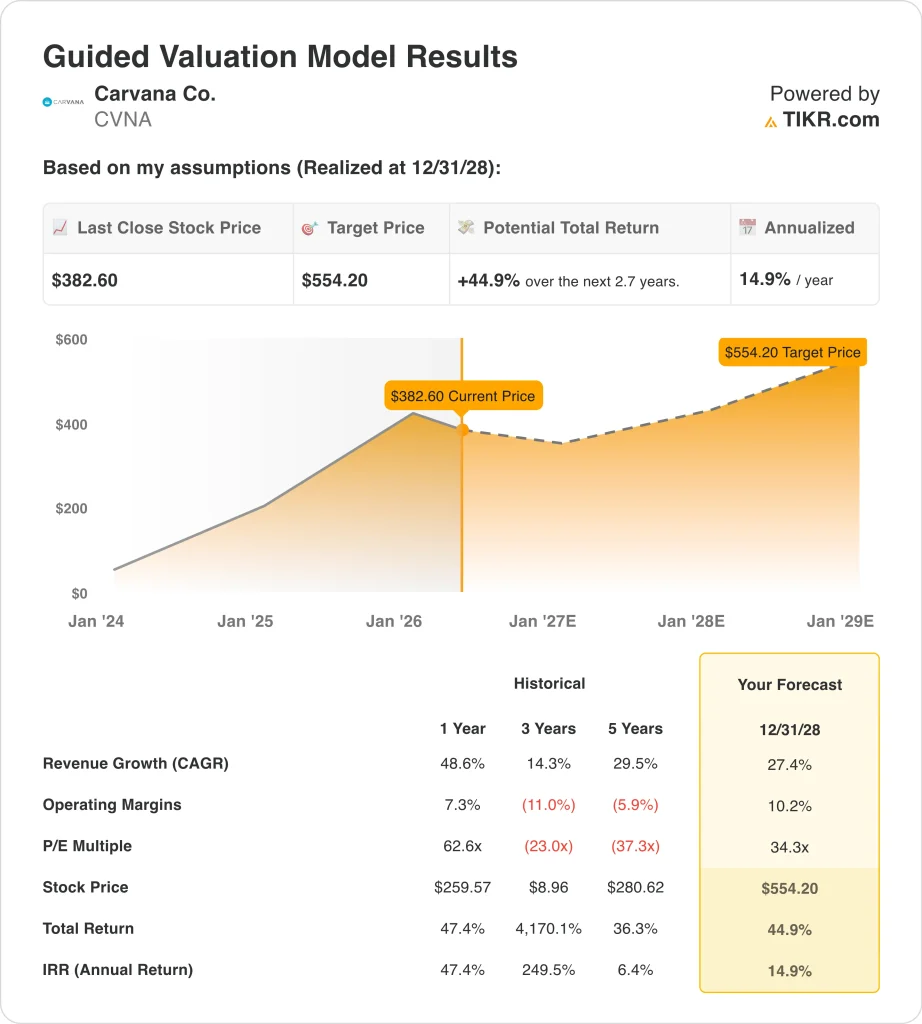

- Valuation model target price: $554

- Implied upside: 44.9% over 2.7 years

Value your favorite stocks like CVNA with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Carvana Co. (CVNA) shares fell about 6% this week despite reporting one of the strongest quarters in the company’s history. Q1 2026 revenue came in at $6.43 billion, a 52% jump from the same period a year ago and well ahead of analyst estimates of $6.08 billion. Net income rose 8.6% to $405 million, confirming that Carvana is growing profitably and not just chasing volume.

Several brokers raised their price targets after the results, citing strong used-car demand and improved unit economics. Unit economics refers to how much profit Carvana generates per vehicle sold, and that number has improved sharply over the past two years.

Despite analyst upgrades, the stock pulled back as investors weighed the company’s elevated valuation against near-term uncertainty in the broader market.

Carvana also announced an expansion of its inspection and reconditioning facility at the ADESA Syracuse site, creating approximately 200 new jobs. ADESA is a network of vehicle auction and logistics sites that Carvana acquired to speed up its car preparation process. Building out that infrastructure reduces vehicle turnaround time and lowers per-unit costs, both of which support margin improvement.

A 5-to-1 stock split is scheduled for May 6, 2026. Stock splits do not change the underlying business value, but they lower the per-share price and can attract a broader base of retail investors. Going forward, Q2 2026 results expected on July 24 will be the next major test of whether Carvana can sustain its extraordinary revenue momentum.

See analysts’ growth forecasts and price targets for CVNA (It’s free) >>>

Is Carvana Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 27.4%

- Operating Margins: 10.2%

- Exit P/E Multiple: 34.4x

Based on these inputs, the model estimates a target price of $554, implying a 44.9% total return from the current share price of $383 and a 14.9% annualized return over the next 2.7 years.

A 14.9% annualized return approaches the 15% threshold that often signals an undervalued or high-growth opportunity. But the model requires Carvana to sustain 27.4% compound annual revenue growth through the end of 2028. That is an ambitious assumption, even for a company that just delivered 52% quarterly growth, so the target carries real execution risk.

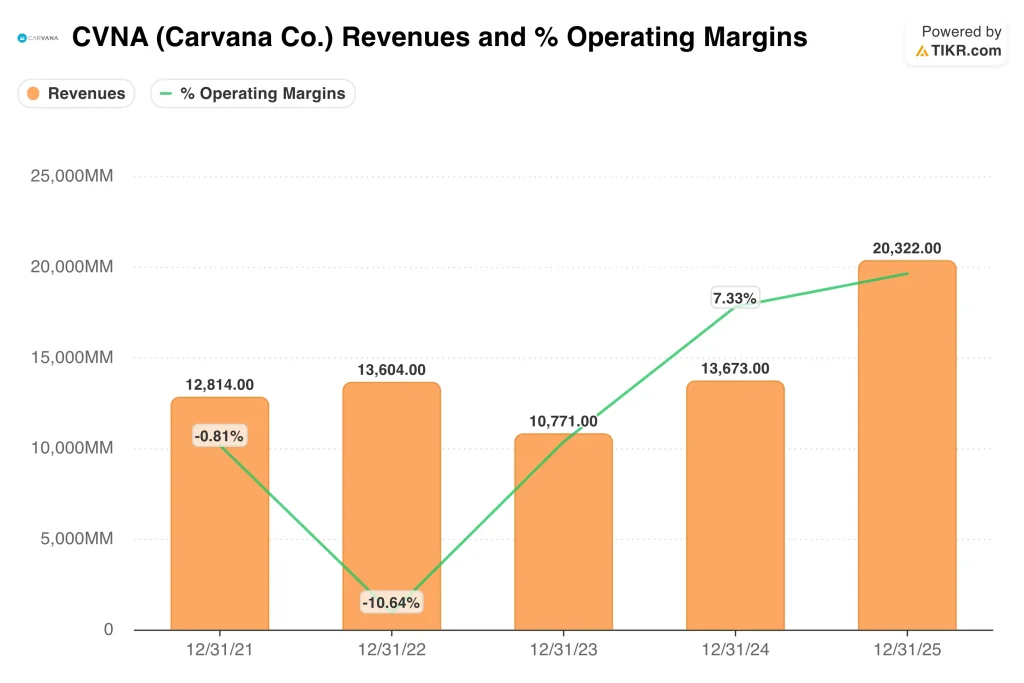

Carvana’s operating margin of 9.2% over the past twelve months shows the business has made a genuine financial turnaround. Just a few years ago, the company carried debt levels that raised serious solvency concerns. Today, the leverage ratio has declined sharply, and net debt stands at approximately $2.6 billion, a manageable level given the earnings power the company is now generating.

The 34.3x exit P/E multiple reflects the market’s expectation that Carvana remains a high-growth platform rather than a mature auto retailer. Traditional dealers trade at single-digit earnings multiples because their growth is slow and cyclical. Carvana’s premium is justified by its fully online model, faster inventory turnover, and improved unit economics, but only if revenue continues expanding at a strong pace.

Street analysts set an average price target of $465, which is below the model’s $554. That gap suggests the model is using growth assumptions that are more aggressive than mainstream Wall Street forecasts. Investors should factor that difference into their analysis before treating the target as a base case outcome.

What’s Driving Carvana Stock Going Forward?

Used-car demand is the foundation of Carvana’s growth story, and Q1 results confirmed that demand remains healthy. Carvana’s fully online buying model, which lets customers browse, finance, and receive a vehicle without visiting a dealership, continues to differentiate it from traditional auto retailers. As long as consumers favor digital convenience over showroom visits, Carvana should continue gaining market share.

The ADESA logistics network expansion is a key operational catalyst for margin improvement. More reconditioning capacity means faster inventory turnover and lower per-vehicle preparation costs. Carvana’s ability to prepare and deliver cars efficiently is central to the 10.2% operating margin target in the valuation model, so this infrastructure investment supports the long-term earnings trajectory.

The 5-for-1 stock split on May 6 will lower the per-share price from roughly $383 to around $77. That price level makes the stock more accessible to individual investors and could increase daily trading volume. But institutional investors and analysts focus on the business fundamentals, so the split’s impact on the investment thesis is cosmetic rather than structural.

Tariff policy on imported vehicles and auto parts is a background risk that management will likely address on the Q2 call. Higher import costs could push used-car prices upward, which might benefit Carvana’s per-unit revenue in the short term but could also dampen consumer demand if vehicle affordability deteriorates materially.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Carvana?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CVNA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CVNA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Carvana stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!