Key Stats for Mastercard Stock

- Current Price: $495.46

- Target Price (Mid): ~$904

- Street Target: ~$649

- Potential Total Return: ~82%

- Annualized IRR: ~14% / year

- Earnings Reaction: -1.48% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Mastercard (MA) shares fell 1.48% on April 30, even after beating every key Q1 2026 estimate, extending a year-to-date decline of roughly 13% while the underlying business accelerated. Bulls say the selloff reflects temporary macro anxiety. Bears cite the Middle East conflict’s drag on cross-border travel and a premium multiple.

The question the market cannot yet resolve is whether those headwinds are passing noise or the beginning of a structural slowdown. The Q1 transcript makes a strong case for the former.

What the Numbers Actually Said

The results left little room for bearish interpretation. Mastercard reported Q1 actual revenue of $8,398 million against a consensus estimate of $8,255.52 million, and adjusted EPS of $4.60 against an estimate of $4.41, a 4.24% beat per the Q1 2026 earnings release. On a currency-neutral basis, net revenue grew 12%, and net income grew 15% year over year. CEO Michael Miebach’s summary was direct: “Building on 2025 momentum, ’26 is off to an excellent start.”

The figure most worth watching is Value-Added Services and Solutions, or VAS, covering cybersecurity, fraud management, data analytics, and open finance. VAS grew 18% on a currency-neutral basis in Q1, representing roughly 40% of total revenue.

CFO Sachin Mehra confirmed explicitly that the 18% carries no acquisition contribution; it is entirely organic. For context, Q4 2025’s 22% VAS growth included approximately 3 percentage points from the Recorded Future acquisition, making Q1’s organic result the cleaner signal of underlying demand.

The core network held firm. Switched transactions grew 9%, or 10% excluding the Capital One debit portfolio migration, which is now essentially complete. Contactless penetration reached 78% of all in-person switched purchase transactions, up 5 percentage points year over year. Cross-border volume grew 13% for the full quarter, though travel began softening in March as the Middle East conflict intensified.

See historical and forward estimates for Mastercard stock (It’s free!) >>>

The Middle East Headwind Is Real but Bounded

The conflict’s drag on cross-border travel is the primary near-term overhang. CFO Mehra sized it on the call: the Gulf Cooperation Council countries and Israel together represent roughly 6% of Mastercard’s total cross-border volumes, inbound and outbound. Real but bounded in a network operating across 150 currencies globally.

Management’s base case assumes the conflict ends in Q2, with the largest headwinds concentrated there and a gradual recovery in the second half. Mehra noted that, absent the conflict, Q2 net revenue growth would have been generally in line with Q1. Full-year guidance held at the high end of a low-double-digit range on a currency-neutral basis, with an approximately 1.5 percentage point FX tailwind adding a new positive.

The portfolio shift headwind, certain travel-heavy card portfolios migrating off the network, is a separate factor that will persist for multiple quarters and is already embedded in consensus estimates.

The Buyback Signal

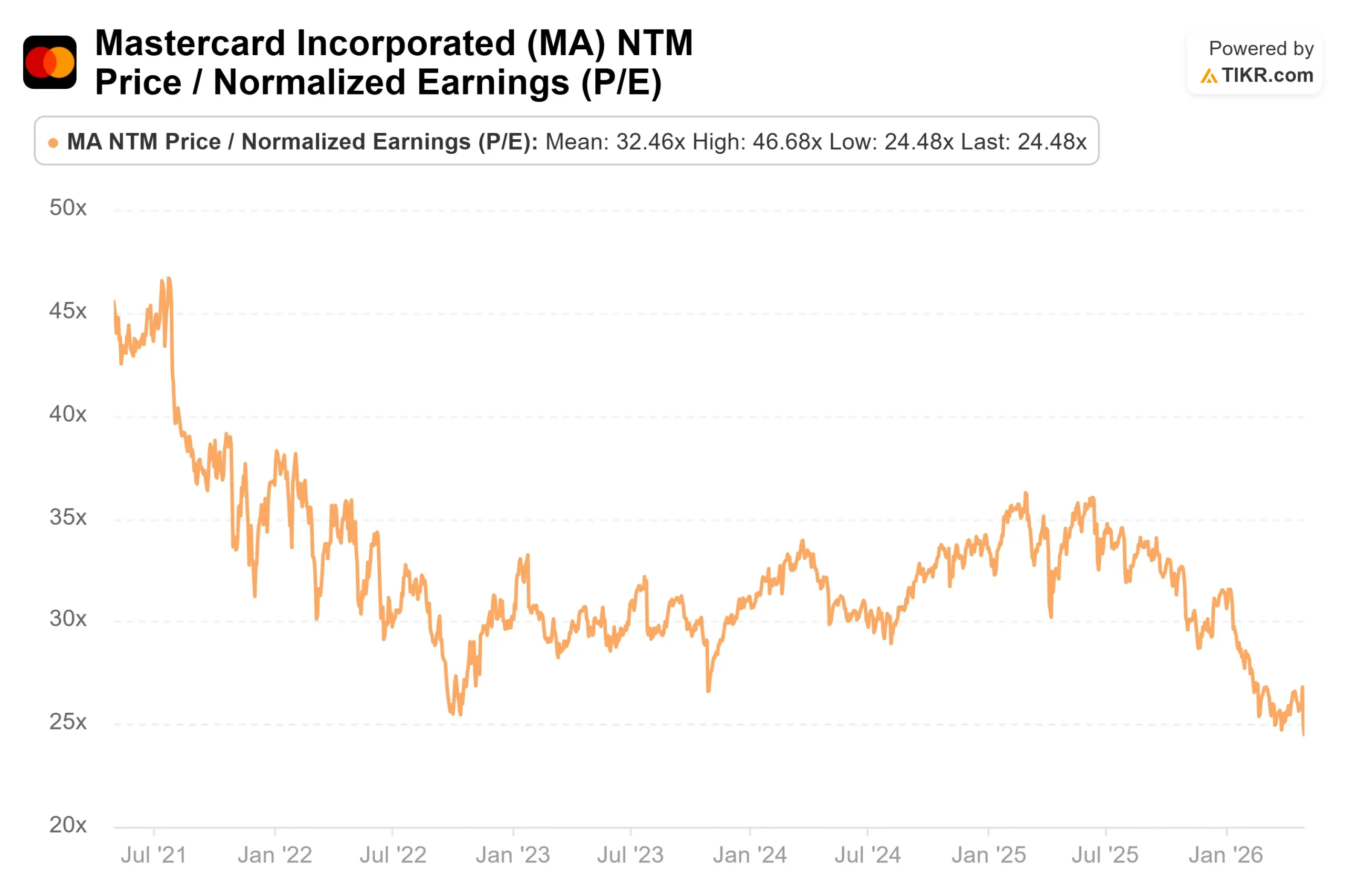

One of the clearest signals in Q1 is not on the income statement. Mastercard repurchased $4.0 billion in stock during Q1 and an additional $1.7 billion through April 27, totaling $5.7 billion in roughly four months.

Mehra was explicit about the rationale: “We accelerated the pace of our share buybacks given current valuation levels and our strong conviction in our long-term growth potential.” When management deploys $5.7 billion of its own capital against a stock and explicitly cites valuation, it is a stronger signal than any analyst note.

The TIKR multiple data supports the read. As of May 1, MA trades at 24.48x NTM P/E and 18.65x NTM EV/EBITDA, representing meaningful compression for a business that has compounded revenue at 16.4% over the past year and 16.5% over five years.

See how Mastercard performs against its peers in TIKR (It’s free!) >>>

Three Growth Engines Not Fully Priced In

Three structural opportunities from the Q1 transcript represent incremental revenue beyond the core network’s current run rate.

Agentic commerce. Miebach confirmed that nearly all Mastercards globally are now enabled for Mastercard Agent Pay, the company’s AI-driven payments infrastructure, with active partnerships spanning Google, Microsoft, and OpenAI. In Q1, Mastercard launched Verifiable Intent, a tamper-resistant record of what a consumer authorized when an AI agent acts on their behalf. The FIDO Alliance, the industry body that sets authentication standards, is now using it as the foundation for its agentic commerce security standards. Volumes are early-stage, as Miebach acknowledged, but the infrastructure positions Mastercard as the trust and settlement layer for a category that could reshape commerce over the coming decade.

Stablecoins. In March, Mastercard announced a planned acquisition of BVNK, a London-based stablecoin infrastructure firm, for up to $1.8 billion, including $300 million in contingent payments. BVNK enables stablecoin payments across more than 130 countries on all major blockchain networks. The deal is pending regulatory approval. The revenue model is basis points on stablecoin volume in an addressable market Mastercard does not currently participate in.

Cybersecurity. Mastercard Threat Intelligence, which combines Mastercard’s transaction data with Recorded Future’s capabilities, has already engaged more than 500 customers since launching. Ethoca products, Mastercard’s dispute resolution and fraud management tools, grew around 25% year over year last quarter, per Miebach’s prepared remarks. AI-driven fraud creates a structural tailwind for this business that is independent of payment volumes.

TIKR Advanced Model Analysis

- Current Price: $495.46

- Target Price (Mid): ~$904

- Potential Total Return: ~82%

- Annualized IRR: ~14% / year

See analysts’ growth forecasts and price targets for Mastercard stock (It’s free!) >>>

The mid-case model uses the mid scenario from TIKR. The two primary revenue drivers are continued VAS growth outpacing the core network and the secular digitization of transactions in underpenetrated markets. On that second point, switched transaction penetration has moved from 60% in 2020 to north of 70% today, with material runway remaining in markets like Japan and Mexico, where Mastercard only recently began switching transactions at scale, per management’s Q1 comments. The margin driver is operating leverage in VAS: as the faster-growing, higher-margin services segment expands its share of total revenue, blended margins widen without requiring cost cuts. The mid-case projects a net income margin of approximately 47%.

The primary risk is a scenario where the Middle East conflict extends beyond Q2 and VAS growth decelerates. The secondary risk is that the BVNK acquisition, still pending regulatory approval, closes later than expected, leaving a window for competitors to build stablecoin infrastructure positions first.

Against 29 Buys, 7 Outperforms, 3 Holds, and 1 No Opinion from Street analysts, the consensus mean target of approximately $649 already implies around 31% upside on more conservative assumptions than the TIKR model.

Conclusion

The metric to watch at the Q2 2026 earnings call on July 23, 2026, is cross-border travel volume growth. Management’s entire second-half recovery thesis rests on the conflict ending in Q2 and travel sequentially recovering from its depressed April levels. Any improvement in that figure is the clearest confirmation that the thesis is on track. Mastercard’s 13% year-to-date decline reflects a bounded geographic headwind, not a broken business, and management just spent $5.7 billion of its own capital making exactly that argument.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Mastercard?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Mastercard, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Mastercard alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Mastercard on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!