Key Stats for Figma Stock

- Past week’s performance: 8.3%

- 52-week range: $17 to $143

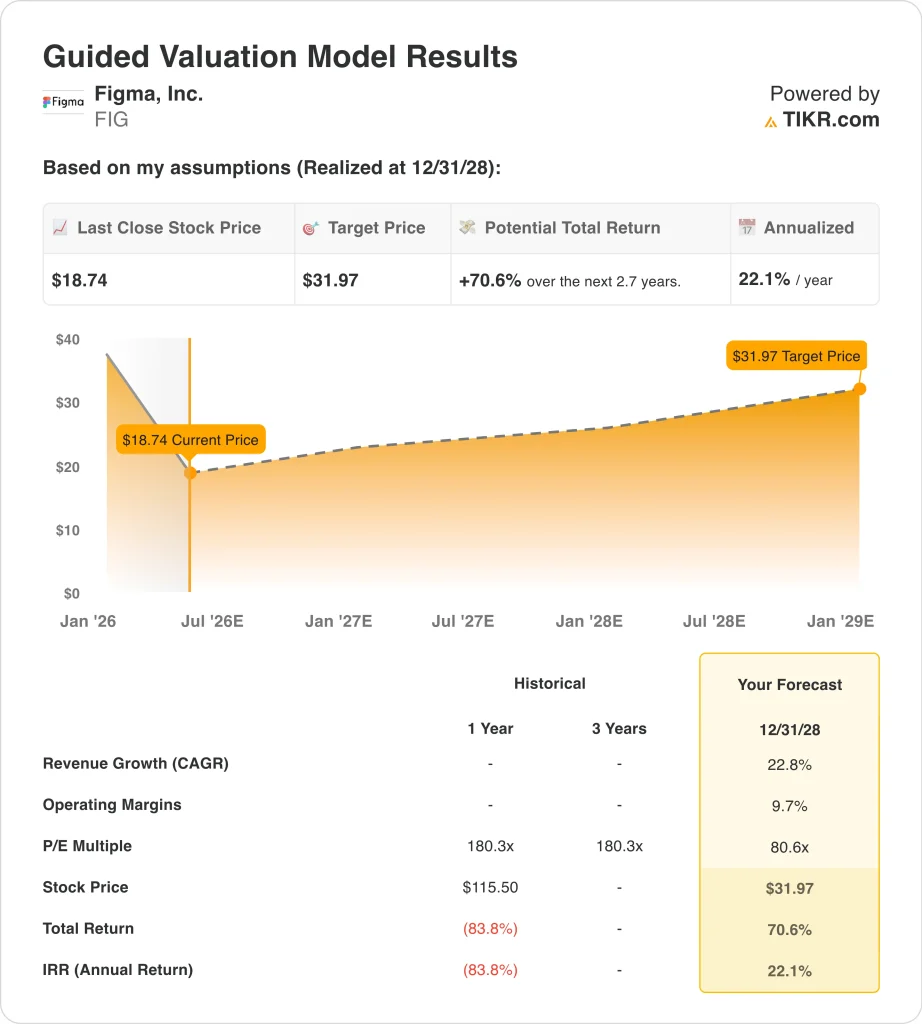

- Valuation model target price: $32

- Implied upside: 70.6% over 2.7 years

Value your favorite stocks like Figma with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Figma, Inc. (FIG) shares climbed about 8.3% this week, recovering from recent pressure tied to competitive concerns. The stock remains well below its 52-week high of $143, and is currently trading near $19.

Much of the recent decline was tied to Anthropic’s Claude Design announcement in mid-April, which weighed on Figma shares. So the week’s bounce reflects sentiment normalization after what appeared to be an overreaction.

The business fundamentals paint a stronger picture than the recent stock action suggests. Figma beat Q4 2025 revenue estimates, reporting $303.8M versus the $293.2M consensus.

That beat suggests the core collaborative design business remains healthy despite the rise of AI design tools. And Figma has been actively building out its platform through new integrations, including Figma Weave.

There are also some concerns investors should track closely. Board director Mike Krieger resigned in April, and several senior executives also disposed of shares recently.

And Lowey Dannenberg, a law firm, is probing Figma’s IPO process for potential securities law violations. Going forward, managing those concerns while maintaining product momentum will be key to sustaining the FIG rebound.

See analysts’ growth forecasts and price targets for Figma (It’s free) >>>

Is Figma Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 22.8%

- Operating Margins: 9.7%

- Exit P/E Multiple: 80.6x

Based on these inputs, the model estimates a target price of $32, implying 70.6% total upside from the current share price and a 22.1% annualized return over the next 2.7 years.

That 22.1% annualized return is well above the 10% threshold that makes a stock look genuinely attractive. The model assumes 22.8% annual revenue growth, consistent with Figma’s track record and strong design software adoption trends.

And the 9.7% operating margin target is realistic, because Figma is still absorbing the costs of scaling its enterprise go-to-market. So the model is not asking for a dramatic transformation, but rather disciplined execution on a well-established growth trajectory.

The 80.6x exit P/E multiple is high, but it reflects Figma’s standing as a category leader in collaborative design software. Figma’s gross margin of 82.4% is exceptional and typical of the best software businesses, so a premium multiple is not unwarranted.

But the stock has fallen over 86% from its 52-week high, reflecting a sharp IPO valuation correction. So if Figma executes on its growth plan, the current entry point could offer meaningful long-term returns for patient investors.

What’s Driving Figma Stock Going Forward?

Q1 2026 earnings, expected around May 14, will be the most important near-term catalyst. Investors will want continued revenue momentum and commentary on how Figma is responding to AI design competition. Because the stock is still well below its all-time highs, management needs to reassure investors on long-term competitive positioning.

The emergence of Anthropic’s Claude Design is the most significant competitive threat to monitor. Figma’s core value is collaborative design, where teams work inside its platform as a daily shared workflow.

And while Claude Design can generate UI components, it has not yet matched the depth of Figma’s collaborative environment. But rapidly improving AI tools could reduce switching costs and pressure Figma’s pricing power over time.

Product expansion remains the key internal growth lever for Figma. Figma Weave integration and broader platform investments aim to deepen engagement and increase revenue per user.

And Figma’s 82.4% gross margin provides strong operating leverage, so revenue growth can translate quickly into earnings. But achieving profitability will require continued enterprise expansion and careful management of operating expenses over the next several quarters.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Figma?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FIG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FIG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Figma stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!