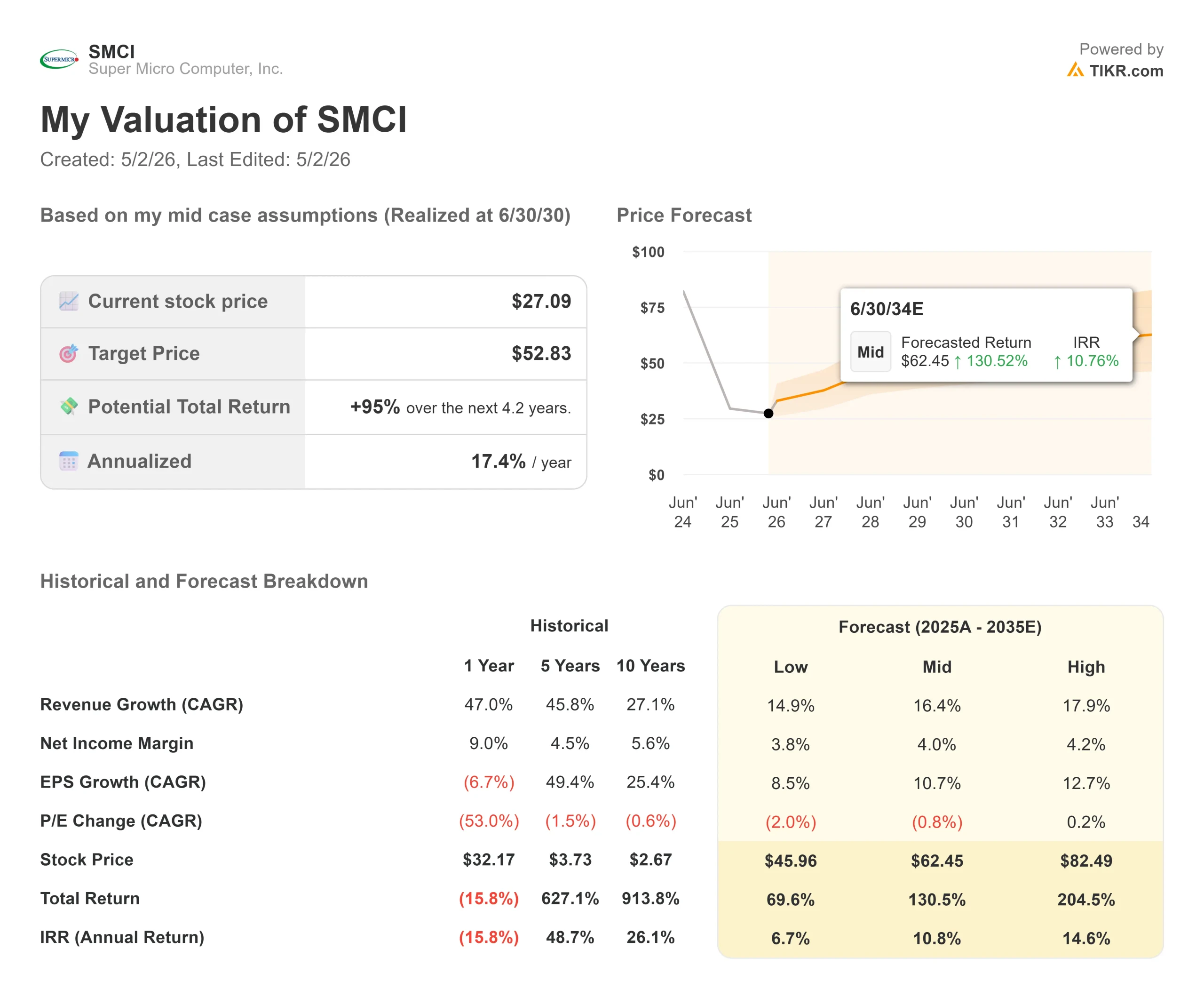

Key Stats for Super Micro Computer Stock

- Current Price: $27.09

- Target Price (Mid): ~$53

- Street Target: ~$33

- Potential Total Return: ~95%

- Annualized IRR: ~17% / year

- Earnings Reaction (Q2 FY2026): +13.78% (February 3, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Super Micro Computer (SMCI) is sitting on one of the stranger setups in AI hardware right now. The company just posted its best quarterly revenue ever. The stock is still down more than 56% from its 52-week high of $62.36.

That gap exists because of one evening in March. On March 19, 2026, the U.S. Department of Justice unsealed an indictment against three individuals associated with Super Micro, alleging a scheme to divert servers carrying restricted U.S. AI technology to Chinese buyers in violation of export control laws. Co-founder Yih-Shyan Liaw was among those named and subsequently resigned from the board. Super Micro is not a named corporate defendant and stated the alleged conduct “is a contravention of the Company’s policies and compliance controls.” SMCI shares fell 33.3% in a single session on March 20, 2026.

The stock has since recovered roughly 25% through April, but multiple securities class-action lawsuits remain active with a lead plaintiff deadline of May 26, 2026.

Bulls say the AI demand cycle has years left, and one person’s alleged conduct does not erase $40 billion in revenue guidance. Bears say a live DOJ investigation keeps institutional money on the sidelines and the multiple permanently compressed. Both sides are now watching May 5.

The Q2 Beat the Market Almost Ignored

For Q2 fiscal year 2026, Super Micro reported $12.68 billion in revenue, up 123% year over year and nearly $3 billion above the top of its own $10 billion to $11 billion guidance range. The stock jumped 13.78% on February 3, 2026.

CFO David Weigand noted on the earnings call that AI GPU platforms represented over 90% of Q2 revenue, with the large data center segment alone delivering $10.7 billion, up 151% year over year.

Worth noting: the Q2 figure included approximately $1.5 billion in shipments delayed from Q1 due to customer readiness. The underlying run rate still supports full-year guidance of at least $40 billion. But the problem was not the revenue line. It was what happened to margins.

See historical and forward estimates for Super Micro Computer stock (It’s free!) >>>

The One Number Q3 Must Deliver

Non-GAAP gross margin fell to 6.4% in Q2, down from 9.5% in Q1. Per TIKR data, SMCI’s gross margin was 18.1% as recently as fiscal 2023. CEO Charles Liang identified three culprits on the earnings call: customer mix shifting toward large hyperscalers with pricing leverage, expedited transportation costs from ramping the new GP300 platform at scale, and ongoing component shortages in memory and storage.

The GP300 timing matters. Liang said the platform “was a little bit new to us” in Q2, meaning one-time ramp costs inflated the damage. Management guided gross margins to improve 30 basis points sequentially in Q3, putting the target at roughly 6.7%.

That is still far below what the business needs in the long term. But direction matters more than level right now. Liang said plainly: “I believe our gross margin will start to improve quarter after quarter.” A Q3 result at or above 6.7% gives the recovery thesis its first confirmed data point. A miss means the legal overhang becomes the only story investors are telling.

See how Super Micro Computer performs against its peers in TIKR (It’s free!) >>>

Is SMCI Undervalued Today?

The path to margin recovery runs through DCBBS (Data Center Building Block Solutions), a pre-designed modular infrastructure package covering compute, cooling, power, and management. Liang disclosed on the Q2 call that DCBBS contributed 4% of the company’s profit in just its first two quarters of existence, and guided that share to reach double digits by the end of calendar 2026.

What makes that meaningful is the margin profile. When pressed directly on DCBBS margins by a Goldman Sachs analyst on the call, Liang said: “The margin is much better, for sure, more than 20%” a sharp contrast to the 6.4% blended non-GAAP gross margin. Every point DCBBS gains as a share of revenue mechanically pulls the blended margin higher.

On valuation, SMCI trades at 0.37x NTM EV/Revenue and 8.03x NTM EV/EBITDA per TIKR data. Dell Technologies trades at 1.11x EV/Revenue and 10.64x EV/EBITDA. Hewlett Packard Enterprise sits at 1.31x and 7.96x, respectively. SMCI’s discount to both peers is steep and almost entirely explained by the legal overhang, not operational inferiority.

The company’s 10-year revenue CAGR of 27.1% per TIKR data dwarfs what either peer has produced. Whether the discount is an opportunity or a trap depends on how the governance situation resolves.

TIKR Advanced Model Analysis

- Current Price: $27.09

- Target Price (Mid): ~$53

- Potential Total Return: ~95%

- Annualized IRR: ~17% / year

See analysts’ growth forecasts and price targets for Super Micro Computer stock (It’s free!) >>>

The TIKR mid-case model projects a target price of around $53 by 6/30/30, using a forward revenue CAGR of approximately 16% and net income margins recovering toward 4%. Both are conservative relative to SMCI’s 10-year historical revenue CAGR of 27.1%. The two primary revenue drivers are continued AI server demand through the Blackwell and Vera Rubin platform cycles, and DCBBS scaling into a higher-margin product category.

The downside case projects around 70% total return if revenue growth slows and margin expansion stalls. The upside case reaches roughly 205% if DCBBS adoption accelerates and customer concentration falls. The primary risk in any scenario is the legal overhang: an adverse outcome in the DOJ investigation or active class actions could trigger customer flight and margin damage that no revenue model absorbs cleanly. At 10.97x NTM P/E against a peer median of 13.41x per TIKR competitor data, even a partial rerating toward peers would produce meaningful upside without any change in the underlying business.

Conclusion

On May 5, watch gross margin. Management guided 30 basis points of sequential improvement over Q2’s 6.4% floor, setting the threshold at roughly 6.7%. A result at or above that confirms the recovery is real. A miss makes the legal overhang the only narrative that matters.SMCI generates around $28 billion in trailing twelve months revenue and trades at roughly 11x forward earnings because the market does not trust its governance. The AI demand is not in question. Whether the legal situation resolves before it does permanent damage is the bet investors are actually making.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Super Micro Computer?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Super Micro Computer, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Super Micro Computer alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Super Micro Computer on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!