Key Takeaways

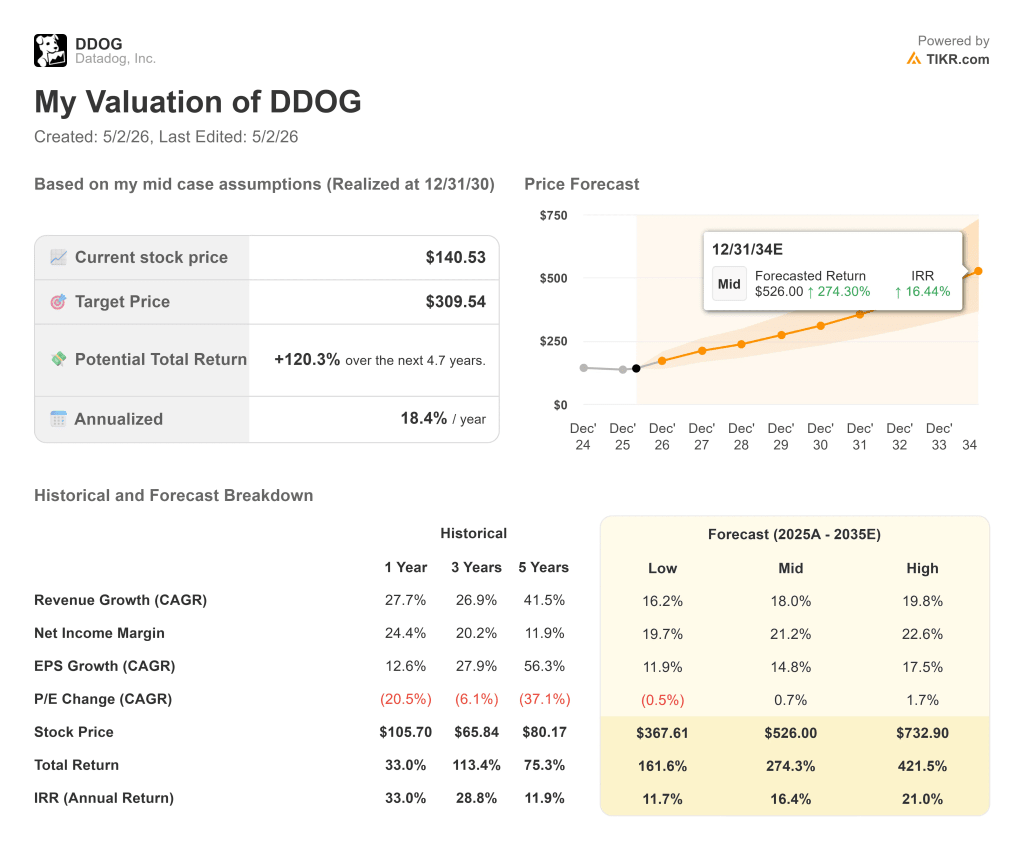

- Datadog, Inc. (NASDAQ: DDOG) grew revenue 27.7% to $3,427.16 million in fiscal 2025, beat revenue consensus in all five reported quarters, and carries a free cash flow margin of 26.7%, while trading at 11.36xNTM EV/Revenue and 46.62x NTM MC/FCF as of May 1, 2026.

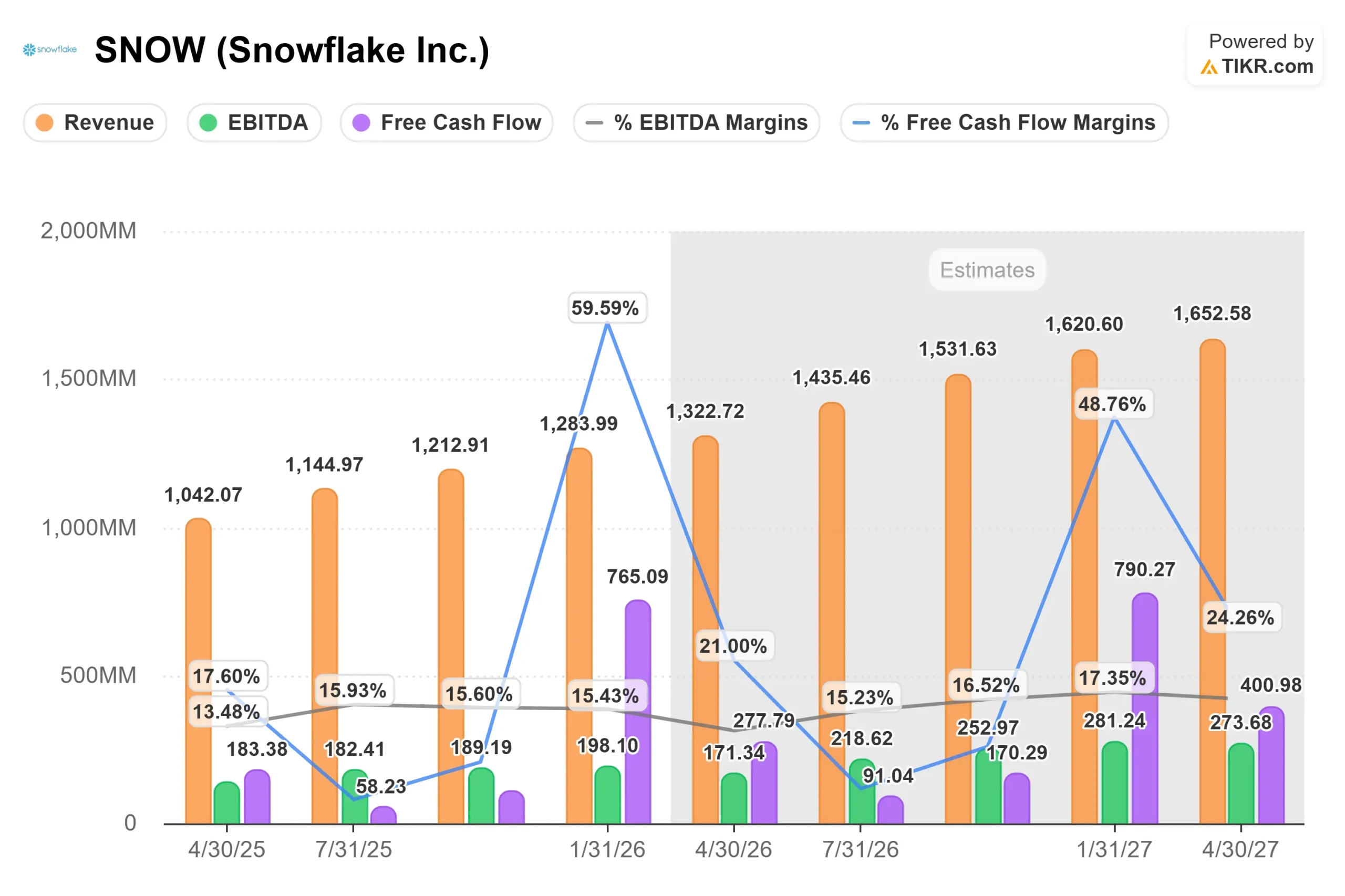

- Snowflake Inc. (NYSE: SNOW) reaccelerated product revenue growth to 30% in Q4 fiscal 2026, closed a record $400 million customer deal, and grew remaining performance obligations 42% year over year to $9.77 billion, according to Snowflake’s Q4 fiscal 2026 earnings release.

- Datadog leads on free cash flow margins today at 26.7% versus Snowflake’s 23.9%, with 81% LTM gross margins versus Snowflake’s 67.2%. Consensus projects both converging near 36% FCF margins by fiscal 2030-2031.

- The TIKR mid-case model prices Datadog at around $310 with an annualized return of around 18%, and Snowflake at around $376 with an annualized return of around 23%, reflecting Snowflake’s deeper discount to its own growth trajectory.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Two Consumption Models, One Question

The cloud infrastructure spending cycle produced two clear beneficiaries. Datadog (DDOG) monitors what runs in the cloud. Snowflake (SNOW) stores and processes what the cloud generates. Both charge customers based on consumption, so revenue rises with the intensity of actual cloud usage rather than seat count.

Both companies are AI infrastructure plays. As enterprises deploy more agents, train more models, and push workloads into production, the infrastructure underneath needs to be monitored, governed, and queried. Datadog and Snowflake sit directly in that path.

According to Snowflake’s Q4 fiscal 2026 earnings release, product revenue hit $1.23 billion in Q4, up 30% year over year. Datadog, heading into its May 7 Q1 2026 earnings report, guided for $951 million to $961 million in Q1 revenue after posting $953.19 million in Q4 2025, according to Datadog’s Q4 2025 earnings release. The question is not whether both companies are growing. The question is which is the better growth play at current prices.

Datadog: The Platform Consolidator with Structural Momentum

Datadog’s model is built on a unified observability and security platform, meaning a single interface where engineers monitor infrastructure, application performance monitoring (APM), logs, and security posture without switching tools. At the March 2026 Morgan Stanley Technology, Media and Telecom Conference, CFO David Obstler described the consolidation engine at work:

“Despite the fact we’ve been at this for a while, only half of our customers are using all 3 pillars. And once a customer standardizes on Datadog, their spend accelerates.”

That matters because it describes a land-and-expand engine with substantial unexploited surface area. The company has 32,000-plus customers, but platform penetration across all three core pillars is only around half. Each incremental product a customer adopts raises their spend.

Datadog grew revenue from $2,684.28 million in fiscal 2024 to $3,427.16 million in fiscal 2025, a 27.7% increase. Free cash flow reached $914.72 million at a 26.7% FCF margin. The company carries approximately $3.2 billion in net cash. LTM gross margins stand at 81%. Revenue beats across the five most recent quarters ranged from 2.72% to 4.53%.

The AI tailwind is both direct and structural. Datadog has 650 AI-native customers, including 19 of the top 20 AI companies by revenue, all 19 spending over $1 million annually, per David Obstler’s remarks at the March 2026 Morgan Stanley conference. According to Guggenheim’s channel checks, Anthropic signed an eight-figure deal with the platform. LLM spans sent to Datadog grew 10x in the six months preceding the conference, per Obstler’s comments. Bits AI, Datadog’s autonomous SRE agent (a tool that detects and triages incidents automatically), entered general availability with over 1,000 paying customers.

According to Datadog’s April 2026 announcement, the company also launched GPU monitoring, positioning the platform ahead of enterprise AI compute buildouts not yet fully reflected in budgets.

On valuation multiples, Datadog trades at 11.36x NTM EV/Revenue as of May 1, 2026. The mean NTM EV/Revenue across the TIKR software peer group stands at 8.45x, placing Datadog at a roughly 34% premium. CrowdStrike trades at 18.90x and Palo Alto Networks at 11.24x in the same group. Datadog’s premium reflects its growth rate and gross margin quality.

See historical and forward estimates for Datadog stock (It’s free!) >>>

Snowflake: The Data Layer Betting on Agentic AI

Snowflake charges customers based on the compute and storage they consume when running queries, pipelines, and AI workloads on top of their data. Revenue moves with the intensity of enterprise data activity, which is why AI is a direct tailwind: more data, more queries, more models, more consumption.

At the March 2026 Morgan Stanley conference, CEO Sridhar Ramaswamy framed the strategy plainly: “Data in Snowflake is data that we can help you get in great shape for AI, data that we can help you govern very easily. It’s the thing that we can then make you easily develop agents on top of.”

According to Snowflake’s Q4 fiscal 2026 earnings release, product revenue reached $1.23 billion in Q4, up 30% year over year. Remaining performance obligations totaled $9.77 billion, up 42% year over year. More than 9,100 accounts now use Snowflake’s AI features. Snowflake Intelligence, the company’s enterprise agentic AI product, reached 2,500 active accounts within three months of launch.

Snowflake signed one deal over $400 million and seven additional nine-figure deals in the quarter. Net revenue retention stood at 125%, meaning existing customers are growing their spend by 25% annually on average.

Full-year product revenue grew from $3,462.42 million in fiscal 2025 to $4,472.32 million in fiscal 2026, a 29.2% increase. Free cash flow was $1,120.31 million at a 23.9% FCF margin. LTM gross margin stands at 67.2%.

Snowflake’s acquisition of Observe, which closed in early February 2026 for approximately $600 million, brings the company into the observability market. According to Snowflake’s Q4 fiscal 2026 earnings call, the deal carries roughly 150 basis points of free cash flow margin headwind in fiscal 2027, pulling guided FCF margins to 23%. That compression is deliberate and temporary.

On valuation multiples, Snowflake trades at 7.89x NTM EV/Revenue and 36.15x NTM MC/FCF as of May 1, 2026, compared to Microsoft at 8.50x and Oracle at 7.58x in the same software peer group. The stock has shed more than 50% from its 52-week high of $280.67. The NTM EV/Revenue compressed from 17.85x as recently as October 2025.

See how Snowflake performs against its peers in TIKR (It’s free!) >>>

Revenue Growth, Margins, and FCF: Where They Actually Differ

On revenue growth, the two companies are nearly even. Datadog grew 27.7% in fiscal 2025, and Snowflake grew 29.2% in fiscal 2026. Consensus three-year revenue CAGRs favor Snowflake at 31.4% versus 26.9% for Datadog.

On gross margins, Datadog leads structurally at 81% versus Snowflake’s 67.2%. Datadog runs software agents; Snowflake runs compute-intensive query workloads. That 13-point gap is structural, not cyclical. Snowflake has committed to 75% non-GAAP product gross margins in fiscal 2027, per its Q4 fiscal 2026 earnings call, but it will not close the gap to Datadog.

On free cash flow margins, Datadog leads at 26.7% versus Snowflake’s 23.9%. Snowflake’s guided FCF margin of 23% for fiscal 2027 reflects the Observe headwind. Both are projected to reach approximately 36% FCF margins by fiscal 2030-2031, per TIKR consensus estimates.

On the operating margin trajectory, Datadog’s EBIT margins are expected to reach around 21% by fiscal 2026. Snowflake’s non-GAAP operating margins are guided to 12.5% for fiscal 2027 and expanding from there. Datadog’s structural advantage is real, but Snowflake is operating from a lower base with more room for incremental improvement.

On EV/Revenue, Snowflake is meaningfully cheaper at 7.89x versus Datadog’s 11.36x despite a comparable or faster growth rate. That 30% discount reflects near-term margin compression, CRO transition risk, and execution uncertainty around monetizing Snowflake Intelligence at scale.

What the TIKR Valuation Models Say

The TIKR mid-case model for Datadog projects a target price of around $310, a total return of around 120%, and an annualized return of around 18% per year, realized at December 31, 2030. The model assumes a revenue CAGR of around 18% and a net income margin of around 21%. The two key revenue drivers are AI-native customer expansion and ongoing platform consolidation as customers adopt additional pillars. The primary risk is multiple compression: at 64.62x NTM P/E, any guidance miss would compress the multiple quickly.

The TIKR mid-case model for Snowflake projects a target price of around $376, a total return of around 166%, and an annualized return of around 23% per year, realized at January 31, 2031. The model assumes a revenue CAGR of around 19% and a net income margin of around 14%. The two key revenue drivers are AI workload consumption growth and monetization of Snowflake Intelligence across the 9,100-plus accounts already using Snowflake AI features.

The primary risk is go-to-market execution: according to a previously published TIKR analysis, new CRO Jonathan Beaulier replaced Mike Gannon on March 31, 2026, and has not yet run a full sales cycle, introducing uncertainty at precisely the moment the AI workload thesis needs confirmation.

Snowflake offers around 4.5 percentage points of additional annualized return over Datadog’s mid-case, reflecting the deeper valuation discount rather than a materially superior business.

See analysts’ growth forecasts and price targets for Snowflake stock (It’s free!) >>>

Which Stock Is the Better Growth Play at Current Prices

Datadog is the higher-quality compounder at a higher price. The business generates 81% gross margins, has beaten consensus estimates in every reported quarter of the past year, carries over $3 billion in net cash, and sits at the intersection of AI infrastructure complexity and enterprise security consolidation.

For investors who want proven execution, durable free cash flow, and a management team with a consistent beat-and-raise track record, Datadog fits that profile. The 11.36x NTM EV/Revenue multiple is not cheap, but it is not unreasonable for a company growing at this rate with these margins.

Snowflake is the higher-upside, higher-uncertainty bet. The stock has lost more than 50% from its 52-week high. The data platform thesis is intact: net revenue retention stands at 125%, RPO growth accelerated to 42% year over year, and Snowflake Intelligence reached 2,500 active accounts within three months of launch.

As AI workloads mature and enterprises push more data-intensive applications into production, the natural beneficiary is the data layer underneath them. The Observe acquisition adds an observability angle that could, over time, allow Snowflake to compete for budgets that currently flow to Datadog. The risks are real: weaker margins than Datadog, a CRO transition introducing near-term go-to-market uncertainty, and a history of multiple compressions.

Datadog is the growth play for investors who want high-conviction execution with a platform already compounding free cash flow. Snowflake is the growth play for investors willing to accept near-term execution risk in exchange for wider potential upside from a deeply compressed starting point. These are different bets, not interchangeable ones.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!