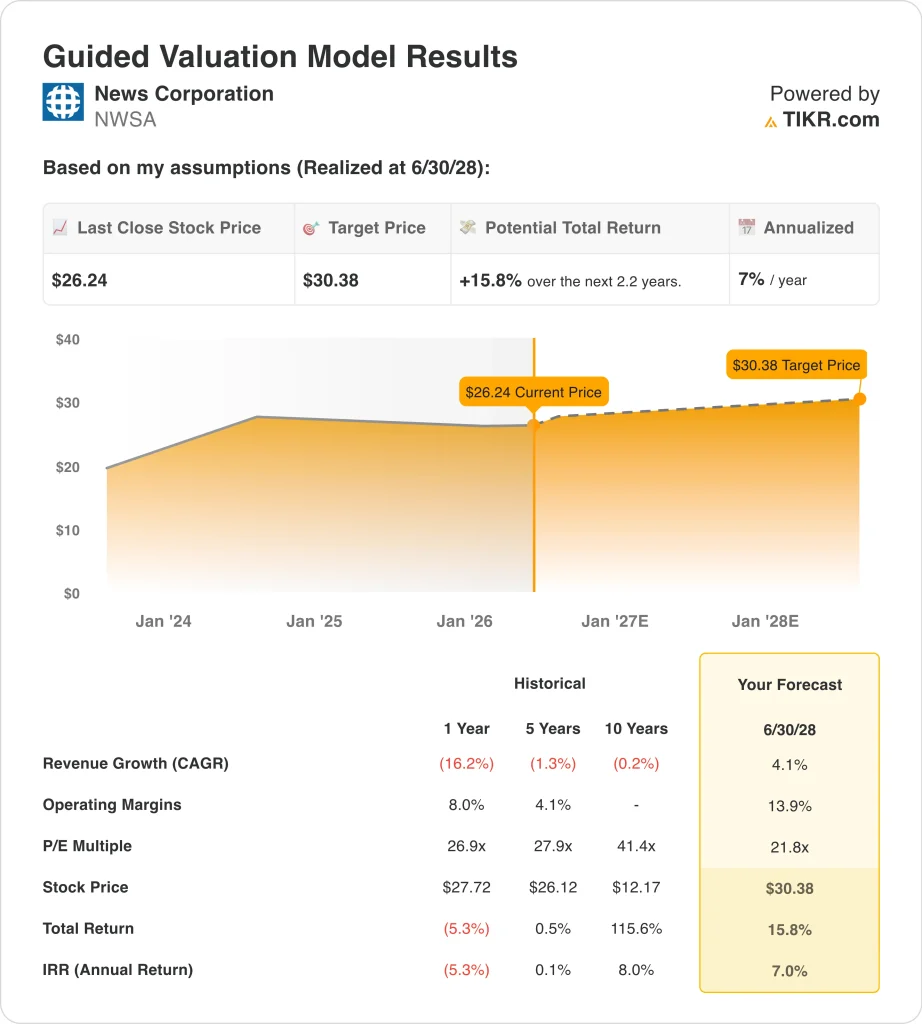

Key Stats for NWSA Stock

- Past week’s performance: Consolidating

- 52-week range: $22 to $32

- Valuation model target price: $30

- Implied upside: +15.8% over 2.2 years

Value your favorite stocks like NWSA with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

News Corporation (NWSA) shares have dipped about 3% over the past year, but the story beneath that modest decline is more complex. The biggest positive development was a content licensing agreement with Meta signed in early March, worth up to $50M per year.

That deal allows Meta to use News Corp content, including from the Wall Street Journal and other properties, to train its AI models. Investors welcomed the move as validation of News Corp’s high-quality editorial assets.

On the earnings front, Q2 FY2026 results came in ahead of expectations. Adjusted EPS of $0.40 beat the consensus estimate of $0.34, and digital revenue growth remained steady. So the quarter reinforced the idea that News Corp’s diversified media portfolio continues to generate real cash flow. Realtor.com also contributed steady performance as a digital services asset.

News Corp also forged a partnership between Dow Jones and prediction market platform Polymarket in January, making the Wall Street Journal an exclusive prediction market media partner.

And HarperCollins teamed up with AI animation studio Toonstar in April to adapt popular books into animated series. Those moves reflect a deliberate strategy to monetize intellectual property in new digital formats beyond traditional publishing.

Australia’s government proposed a 2% levy on large technology companies unless they reach local news licensing deals. That regulatory development could benefit News Corp’s Australian media properties by creating leverage for better compensation terms.

If NWSA stock receives a re-rating from further AI content deals or a strong Q3 earnings beat, the stock could push toward the $34 analyst consensus target.

See analysts’ growth forecasts and price targets for NWSA (It’s free) >>>

Is News Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 4.1%

- Operating Margins: 13.9%

- Exit P/E Multiple: 21.8x

Based on these inputs, the model estimates a target price of $30, implying 15.8% total upside from the current share price and a 7.0% annualized return over the next 2.2 years.

News Corporation trades at $26, sitting well below its 52-week high of $32. The stock’s valuation is modest by media sector standards, with a forward P/E of about 21.8x and a dividend yield of 0.8%.

The analyst consensus target of $34 implies more upside than the valuation model currently projects. So there is a visible gap between what sell-side analysts and the model assume about the growth trajectory.

The 4.1% revenue growth forecast reflects the company’s transition away from declining traditional media toward digital revenue streams. Historically, News Corp’s 5-year revenue growth has been nearly flat at negative 1.3%, so the 4.1% forecast requires genuine acceleration.

The Meta AI content deal, Realtor.com digital data, and Dow Jones subscription growth all form the foundation of that revenue acceleration story.

The 13.9% operating margin assumption is a meaningful step up from where the business has been recently. But the portfolio is diverse, and margins across segments vary widely. Reaching that level requires the higher-margin digital businesses to grow faster than the lower-margin traditional publishing units.

The 7% annualized return sits below the 10% threshold that generally defines an attractive investment, so NWSA is a modest opportunity rather than a high-conviction undervalued play.

What’s Driving NWSA Stock Going Forward?

The most important near-term event is Q3 FY2026 earnings, due on May 7. Analysts will focus on digital advertising trends, Dow Jones subscriber growth, and any updates on AI content licensing revenue. A strong Q3 beat would reinforce the turnaround narrative and could push shares toward the $34 analyst target. And guidance commentary on the Meta deal’s revenue contribution will likely move the stock.

The Meta AI content licensing agreement is potentially a meaningful and recurring revenue stream. At up to $50M per year, it translates News Corp’s editorial quality directly into monetizable digital intellectual property. So similar deals with other major AI platforms remain a plausible and near-term catalyst. The Wall Street Journal and Dow Jones brands carry significant premium positioning in AI training data markets.

News Corp’s Realtor.com business also warrants close attention. The US housing market showed six consecutive months of median price declines through April 2026, but inventory is rising, and conditions are gradually normalizing.

So if housing market activity stabilizes, Realtor.com’s lead generation revenue could recover and lift segment margins. That improvement would be a meaningful tailwind for the company’s digital real estate segment.

Australia’s proposed 2% tech levy on large platforms creates an industry tailwind for News Corp’s Australian operations. That regulation would give local publishers more leverage in AI licensing negotiations.

And News Corp has been vocal about seeking fair compensation from platforms distributing its journalism. That regulatory momentum, combined with its existing deal structures, could expand the AI revenue stream materially over the next two to three years.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in News Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NWSA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NWSA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze NWSA stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!