Key Stats for Quanta Services Stock

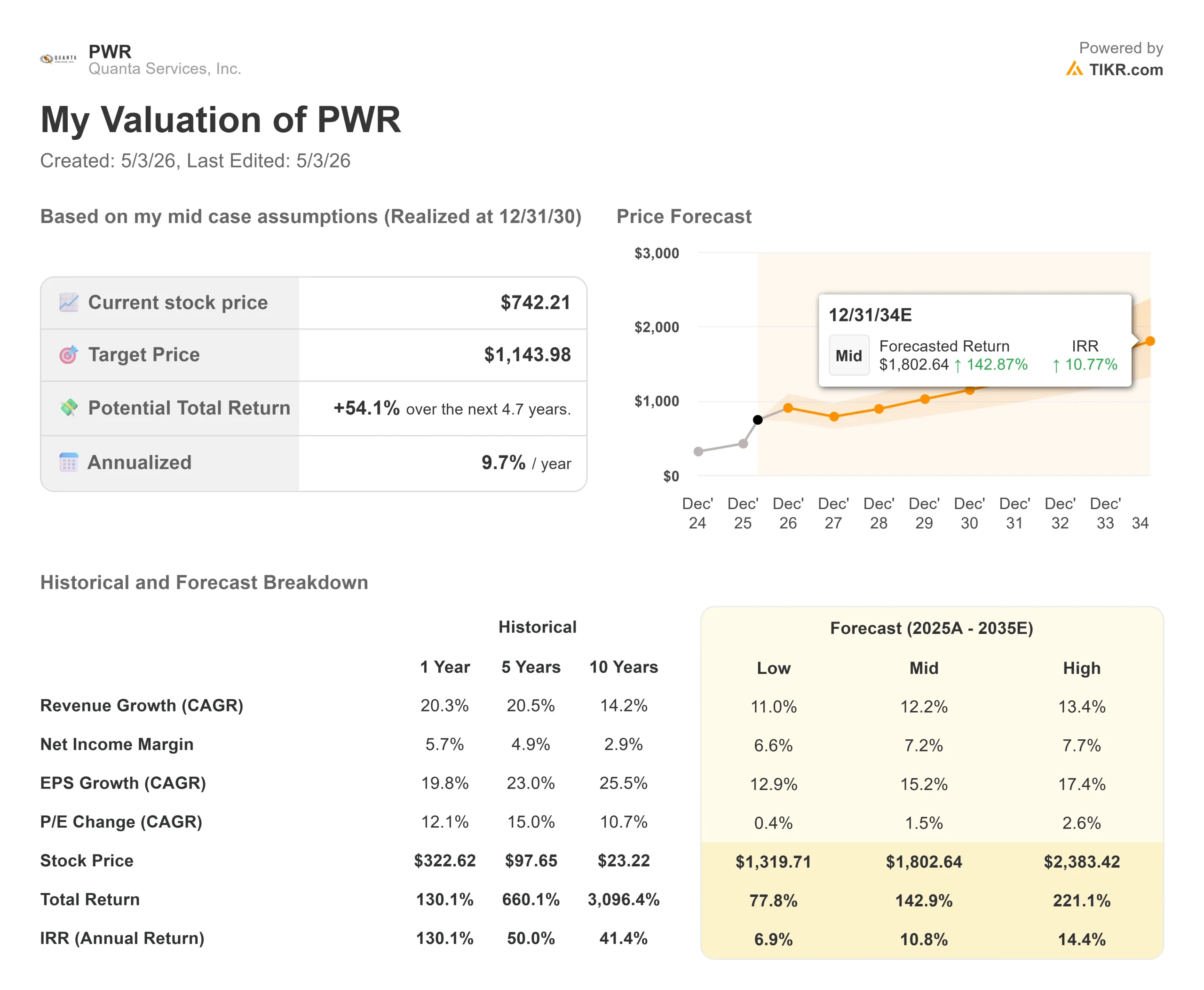

- Current Price: $742.21

- Target Price (Mid): ~$1,144

- Street Target: ~$638

- Potential Total Return: ~54%

- Annualized IRR: ~10% / year

- Earnings Reaction: +1.98% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Quanta Services (PWR) stock gained on April 30 and extended those gains through May 1 after Quanta Services reported Q1 2026 results that beat estimates across every major line. Bulls point to a $48.5 billion record backlog, double-digit growth with zero acquisitions, and a CEO who says the biggest contracted programs haven’t hit revenue yet. Bears look at a stock trading above 53x forward earnings and ask how much of the decade-long infrastructure buildout is already priced in. The central question right now: if Q1 was this strong without any M&A and without the largest projects flowing through, what does the back half look like?

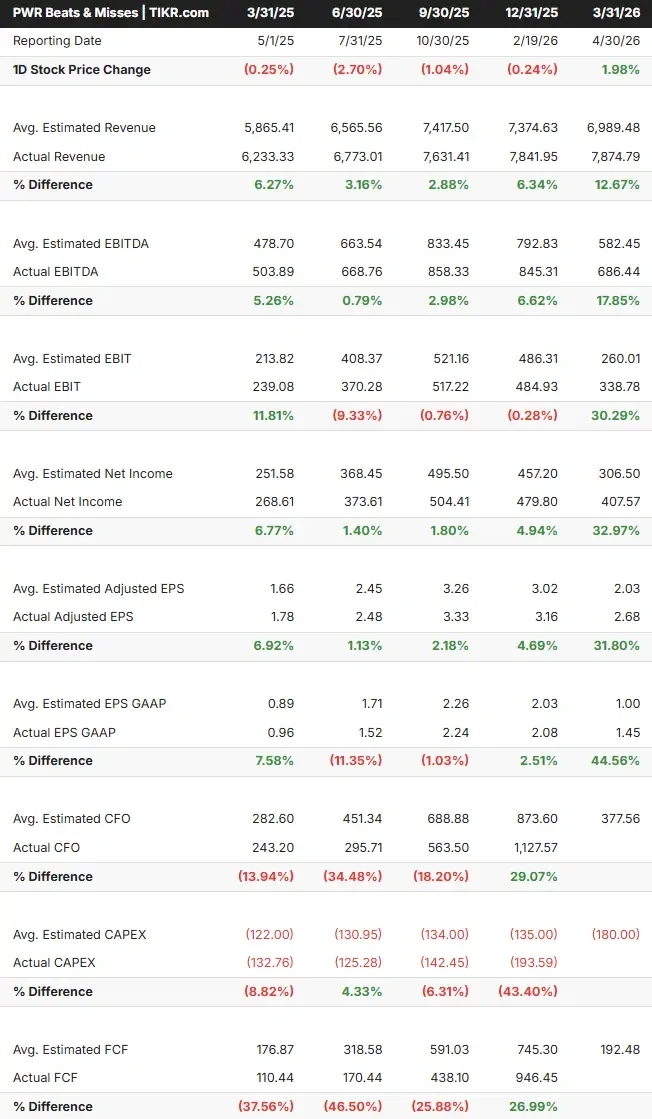

A Clean Beat Across Every Line

Per TIKR’s Beats & Misses data, Quanta’s adjusted EPS of $2.68 beat the $2.03 consensus by 31.8%. Revenue of $7,874.79 million beat the $6,989.48 million estimate by 12.67%. EBITDA of $686.44 million came in 17.85% above the $582.45 million consensus.

What makes those numbers matter: Quanta made no acquisitions in Q1 2026. Every dollar of that 26% year-over-year revenue growth was organic.

CFO Jayshree Desai said on the call that “revenue growth and margin performance exceeded our expectations across both segments.” CEO Earl “Duke” Austin flagged the Underground and Infrastructure segment specifically, saying he expects it to reach double-digit operating margins. Per TIKR’s segment data, that segment generated $398.28 million in operating income on $5,478.23 million in revenue in full-year 2025 margins heading toward double digits would add meaningfully to consolidated earnings power.

See beats & misses for Quanta Services stock (It’s free!) >>>

Guidance Raised, With More Potentially Coming

Management lifted full-year 2026 guidance to revenue of $34.7 billion to $35.2 billion, adjusted diluted EPS of $13.55 to $14.25, and adjusted EBITDA of $3.49 billion to $3.65 billion. The EPS midpoint of $13.90 implies roughly 29% growth over 2025’s $10.75.

Austin said the company raised guidance $50 million past the Q1 beat adding incremental confidence in the back half, not just carrying the outperformance forward. Desai added she feels “greater confidence about being at the higher end” of the free cash flow range.

The guide also has a built-in kicker: no acquisitions are included, and Austin said he expects Quanta to execute deals over the next nine months. Every acquisition that closes before year-end would be additive to an already-raised baseline.

What the Call Actually Said

The earnings transcript contained several details that the headline numbers don’t capture.

On customer relationships: Austin described a shift away from competitive bidding. “We are in the rooms where customers are planning their entire multiyear capital spend. We are negotiating much of the work directly.” Negotiated contracts typically carry better margins and lower revenue volatility than bid work.

On data center demand: Austin confirmed 100%-plus growth in the technology and large-load segment, then added context that investors should note: “We’re early. I think we’ve only been doing this like 1.5 years.” A business scaling this fast in a market where management describes itself as early-stage is a different risk profile than a mature contractor.

On the NiSource pipeline, Austin said the opportunity, which he had referenced previously as $5.7 billion, “is growing every day,” with additional scope from the Alphabet GenCo expansion announced alongside the original Amazon program.

On supply chain: The company is investing $500 million to $700 million in transformer manufacturing and nearly doubling off-site fabrication capacity to approximately 6.7 million square feet. Austin called it a “labor force multiplier” a way to deploy more revenue per worker, not just add headcount.

On cycle durability: When asked whether the load picture was firming up, Austin was direct. “I’ve seen it actually pretty steady. I’m not seeing the falloff that others may think is out there.” He noted that new load was already pushing utility rates lower in some markets the economic signal that makes the buildout politically sustainable over time.

The Valuation Debate

Quanta trades at a trailing EV/EBITDA of 44.8x and an NTM P/E of 53.3x per TIKR’s multiples data. Against peers on TIKR’s Competitors page, EMCOR Group (EME) trades at 19.9x NTM EV/EBITDA, MasTec (MTZ) at 23.6x, and Dycom Industries (DY) at 15.6x, against a peer median of 18.0x. Quanta’s 32.6x NTM EV/EBITDA reflects a significant premium.

The bull case for that premium rests on things peers don’t have: a $48.5 billion backlog with a 1.6x book-to-bill ratio, a domestic transformer manufacturing capability no competitor can match at scale, and a programmatic pipeline that Austin says extends well past 2030.

The risk is multiple compression. A stock at 53x forward earnings on a contractor with 15.0% gross margins has little room for project timing slippage. Austin acknowledged on the call that interconnection queues and air permits remain friction points, with combined cycle gas turbine work not yet in backlog permits expected to progress in the back half of 2026.

After Q1, JPMorgan raised its price target from $627 to $805 and maintained its Overweight rating. Bank of America reiterated Buy and raised its target, noting Quanta’s record backlog provides multi-year visibility with additional runway from high-voltage bookings. Per TIKR’s Street Targets data, the current analyst breakdown is 17 Buys, 1 Outperform, 7 Holds, 1 Underperform, and 1 Sell, with a mean Street target of $638.01 already well below where the stock trades.

See how Quanta Services performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $742.21

- Target Price (Mid): ~$1,144

- Potential Total Return: ~54%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Quanta Services stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of around 12%, supported by backlog conversion at a pace consistent with the raised 2026 guidance and the programmatic pipelines with AEP, NiSource, and data center customers. The margin driver is net income margin expansion from 5.7% in 2025 toward approximately 7% by 2030, as the Underground segment improves and vertical supply chain investments reduce subcontractor reliance. TIKR estimates free cash flow growing from $1.67 billion in 2025 toward $3.27 billion by 2030, supporting both the M&A pipeline and the ongoing supply chain buildout.

The primary risk is timing slippage on large contracted programs. If permitting delays push the AEP 765-kilovolt transmission work or the NiSource CCGT programs back, revenue cadence compresses, and the model’s assumptions come under pressure.

The mid-case ~10% annualized IRR from current prices reflects a stock that has already priced in strong execution. Investors who need double-digit annual returns would need the high-case scenario: around 13% revenue CAGR and net income margins near 7.7%, which the TIKR model prices at approximately $2,383 by 12/31/30 with a ~14% IRR.

Conclusion

Watch free cash flow at the Q2 2026 earnings report, expected in late July 2026. Desai said she’s confident about landing at the high end of the $1.55 billion to $2.05 billion full-year range. If Q2 FCF is tracking toward that pace, it confirms the Underground margin improvement is holding and gives Quanta the capital to fund M&A without balance sheet strain. Quanta isn’t just executing on the current buildout; it is building the supply chain, workforce, and customer relationships to be the default contractor for the next one.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Quanta Services?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Quanta Services, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Quanta Services alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Quanta Services on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!