Key Stats for AppLovin Stock

- Current Price: $460

- Target Price (Mid): ~$1,187

- Street Target: ~$639

- Potential Total Return: ~158%

- Annualized IRR: ~23% / year

- Earnings Reaction: -19.68%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

AppLovin (APP) has spent most of 2026 stuck between a business that keeps performing and a stock that keeps getting punished. The shares fell nearly 50% from their 52-week high of $745.61 to a drawdown low on February 12, 2026, before recovering to $460 today, still down about 38% from the peak. Three forces drove that selloff: short-seller reports alleging fraud, an SEC investigation into AppLovin’s data collection practices confirmed as “still active and ongoing” by the regulator in February, and over $169 million in insider selling.

Bulls say the underlying business has never been stronger. Bears say the regulatory overhang and competition from Meta and Google are real. The core question is simpler: can AppLovin grow beyond mobile gaming fast enough to justify a premium multiple while the SEC probe stays open?

At the Morgan Stanley Technology, Media & Telecom Conference on March 4, CEO Adam Foroughi and CFO Matt Stumpf addressed that question directly. What they said goes further than what most earnings headlines captured.

The 1.3% Number That Explains the Entire Bull Case

The most important figure Foroughi shared at the conference was not a revenue target. It was a conversion rate.

“We, today, have a 1.3% conversion rate on our ads that we serve,” Foroughi said. “Said differently, we make money on 1.3% of the ads we serve. We lose money on 98.7% of the ads we serve.”

AppLovin’s platform reaches over 1 billion daily active users playing mobile games. It already generates around $5.5 billion in annual revenue at an 82% EBITDA margin, the share of each revenue dollar kept as operating profit on just 1.3 cents of value extracted per hundred impressions.

Here is where the upside case begins. When a user is likely to switch games, what Foroughi calls a “high-value moment,” the platform’s conversion rate exceeds 5%. Most impressions are not high-value gaming moments. A user absorbed in a game they enjoy is not going to install a new one. Because AppLovin’s model has had mostly gaming ads to serve in those non-gaming moments, conversion stays low, and revenue per impression stays compressed.

E-commerce changes that. “Fast forward 5 years,” Foroughi said. “Let’s say we have hundreds of thousands of customers. This powerful technology is going to be able to serve a different product in every single ad impression.” With enough advertiser diversity, the model routes each impression toward the most relevant brand instead of forcing a second gaming ad. Conversion rates go up. Revenue per impression goes up. The cost base stays largely flat because the model is already serving the impressions it just needs more demand filling them. Foroughi framed the math directly: scaling toward 5%+ conversion would approach a quadrupling of advertiser spend on the platform. He noted the revenue impact would be smaller than the spend impact because AppLovin pays publishers a majority of that spend. Still, on a base of around $5.5 billion in revenue with free cash flow margins already above 70%, the compounding potential is significant. This is management’s thesis not a TIKR projection or Street estimate.

See historical and forward estimates for AppLovin stock (It’s free!) >>>

The E-Commerce Roadmap Most Investors Have Not Read

The market treats AppLovin’s general availability (GA) e-commerce launch as binary: either it happens, and the stock re-rates, or it doesn’t, and estimates get cut. The reality Foroughi described is more iterative.

AppLovin’s first e-commerce product, launched roughly 18 months before the conference, was a universal campaign a blend of discovery advertising and retargeting. In late October 2025, the company rolled out new customer campaigns targeting users who had visited a brand’s site but never purchased. The week before the conference, it launched new visitor campaigns: ads reaching users who had never appeared in the brand’s data at all. That is the most defensible form of advertising no advertiser can dispute the value of a customer they have never seen.

“Adoption has been really swift,” Foroughi said.

The creative gap is equally important context. Game developers on the platform run more than 50,000 ads per campaign. E-commerce advertisers, at the high end, were running around 1,000. AppLovin’s model finds free cash flow expansion through creative diversity, so that the 50x gap limits how fast e-commerce spend can scale. The company has been closing it with generative AI creative tools pilots on static formats that are already running, and video is in development. Foroughi confirmed both would be available in the first half of 2026.

Bank of America reiterated its Buy rating on April 21 with a $705 price target, calling e-commerce the primary “swing factor.” BofA analyst Omar Dessouky projected e-commerce net revenue to climb from roughly $34 million in Q4 2025 to around $90 million in Q1 2026, driven by approximately 2,000 new advertisers entering the platform. BofA warned that a lack of first-half ramp could trigger second-half estimate cuts.

See how AppLovin performs against its peers in TIKR (It’s free!) >>>

What the Competition Argument Gets Wrong

The standard bear case: Meta has more data, Google has more reach, and eventually one of them replicates what AppLovin built. Foroughi pushed back directly at the conference.

AppLovin has competed against both platforms inside mobile gaming for over a decade and built what management describes as the number-one destination for game developers in that market. His argument is structural. The 1 billion daily users playing mobile games are a different audience, watching a different format, for a different reason than social media users. AppLovin’s ads average over 30 seconds of watch time. Roughly half of the rewarded video users actively opt in to watch them. That attention quality is not replicable on a social feed.

The model is also not a simple ad-targeting layer. Foroughi described a prediction chain that runs 28 days forward, covering ad engagement, download behavior, usage patterns, propensity to spend, and amount of spend all in sequence. Getting any step wrong loses money for both AppLovin and the advertiser. That chain was built on over a decade of proprietary data that no competitor can access.

“Our data moat is already growing with the technology and the ads we serve,” Foroughi said. “The more customers we get and the quicker we do that, that data moat will even expand more.”

AppLovin’s MAX product, which optimizes publisher ad inventory by running a real-time competitive auction across all demand sources, launched in 2018 and grew to roughly one-third of the market in two to three years, per Foroughi. CFO Stumpf confirmed the company runs on around 900 total employees, with only around 400 tied to the core ad tech business. That lean structure is a competitive moat that sales-heavy rivals cannot easily replicate.

On valuation multiples, the TIKR Competitors page shows Unity Software (U) at 21.53x NTM EV/EBITDA, the ratio of enterprise value to next-twelve-month EBITDA. AppLovin trades at 23.08x on the same metric. Given the EBITDA growth rate gap between the two, AppLovin’s modest premium over its closest direct peer is hard to argue with on fundamentals.

The Risks

The SEC investigation is unresolved. The regulator confirmed in February 2026 the probe is “still active and ongoing.” AppLovin acknowledged in its 10-Q that an adverse outcome “could adversely affect” its business and results. Foroughi has called the short-seller allegations “false and misleading,” but the investigation has no public timeline.

Insider selling remains a headline risk. CEO Adam Foroughi sold shares across 44 transactions on March 11 and 12. Director Eduardo Vivas disposed of 163,910 shares on March 16 for approximately $74 million, per SEC Form 4 filings. The company’s ~$3.28 billion buyback authorization provides some offset, but the volume of selling has been consistent.

The e-commerce ramp is still a thesis. AppLovin’s e-commerce team has around 15 people. CFO Stumpf confirmed the company has begun performance marketing to acquire advertisers but is doing it “in a very disciplined manner.” If the GA launch does not produce a measurable step-change in advertiser count by mid-2026, BofA’s estimate-cut warning becomes the next market narrative.

TIKR Advanced Model Analysis

- Current Price: $460

- Target Price (Mid): ~$1,187

- Potential Total Return: ~158%

- Annualized IRR: ~23% / year

See analysts’ growth forecasts and price targets for AppLovin stock (It’s free!) >>>

The TIKR mid-case model applies a compound annual growth rate of around 20% to revenue from 2025 through 2030. Two things drive it: continued AXON model improvements compounding gaming ad performance in the 20% to 30% range, CFO Stumpf described at the conference, and the e-commerce ramp bringing total platform revenue toward around $17 billion by 2030. Net income margins are projected to expand to around 65% as the platform scales. The margin driver is operating leverage. Stumpf confirmed at the conference that data center costs have grown at roughly 10% of the rate of revenue growth, and headcount additions are expected to remain minimal.

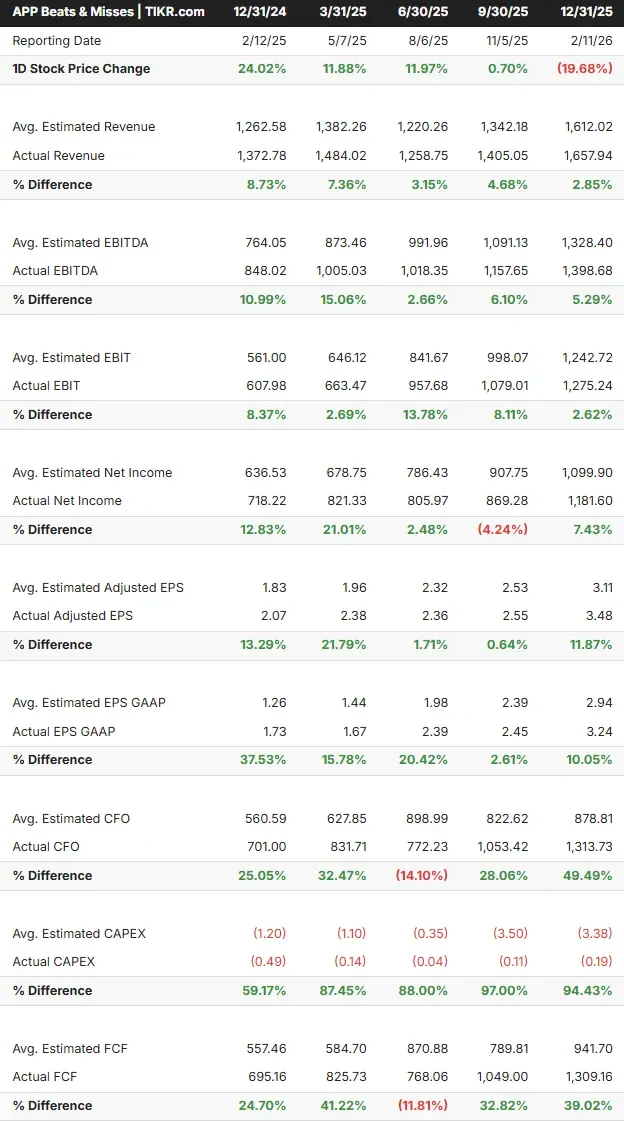

The earnings surprises track record supports that discipline: per TIKR data, AppLovin has beaten EBITDA estimates in each of the past five quarters, with beats reaching as high as about 15%.

The upside: if the e-commerce GA launch accelerates advertiser density and conversion rates begin moving from 1.3% toward 3%, the model’s revenue assumptions look conservative and the stock re-rates sharply. The downside: if SEC enforcement disrupts AppLovin’s data practices or access to major app stores, the core gaming business is at risk and the e-commerce thesis stalls. The Street prices that binary at a mean target of around $639 across 28 price target estimates with 20 Buys, 6 Outperforms, 4 Holds, 1 No Opinion, 1 Underperform, and 1 Sell in analyst recommendations, per TIKR.

At current prices, AppLovin trades at around 23x NTM EV/EBITDA and around 30x NTM P/E, on a trailing twelve months free cash flow base of around $2.7 billion. Investors who want to stress-test the assumptions can run their own inputs through TIKR’s scenario analysis tools.

Conclusion

The number to watch at Q1 2026 earnings on May 6 is e-commerce net revenue from the referral advertiser cohort. BofA is targeting around $90 million, against $34 million in Q4 2025. If that lands and management confirms the GA launch is on track for the first half of 2026, the stock has a clear path toward the Street consensus. AppLovin runs an 82% EBITDA margin business with consistent earnings beats and a data moat built over a decade. The conversion rate math Foroughi laid out at Morgan Stanley is compelling. May 6 is the first chance to see if the numbers confirm it.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in AppLovin?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AppLovin, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AppLovin alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze AppLovin on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!