Key Stats

- Current Price: $110 (May 4, 2026 close)

- Q1 2026 DAU Growth: 21% year-over-year

- Q1 2026 Adjusted EBITDA: $83M (~29% of revenue), per CFO Gillian Munson on the Q1 2026 earnings call

- Full-Year 2026 Revenue Growth Guidance: ~16.1%

- Full-Year 2026 Bookings Growth Guidance: ~10.5%

- Full-Year 2026 Adjusted EBITDA Margin Guidance: ~25.7%

- 2026 Free Cash Flow Guidance: Over $350M

- TIKR Model Price Target: $209

- Implied Upside: ~89%

Duolingo Earnings Breakdown: Q1 2026

Duolingo stock (DUOL) delivered a Q1 2026 adjusted EBITDA of $83M, representing approximately 29% of revenue, according to CFO Gillian Munson on the Q1 2026 earnings call.

DAUs grew 21% year-over-year, landing exactly in line with management’s expectations as the company executes a deliberate pivot toward engagement-first growth.

CEO Luis von Ahn on the Q1 2026 earnings call: “Q1 was about execution. We said we were going to prioritize teaching better and growing users, and that’s exactly what we did.”

Asia remains the fastest-growing region, with China identified as a standout market where Duolingo has achieved profitable performance marketing, per von Ahn on the Q1 2026 earnings call.

New product launches drove the engagement narrative: spoken tokens, speaking adventures, and Flashcards all expanded voice practice across both free and paid tiers, with video call users now speaking more than twice as many words on average as a year ago.

Content velocity accelerated sharply, with 20,500 course units published in Q1 2026 alone, more than 10 times the quarterly output from two years prior, according to von Ahn on the Q1 2026 earnings call.

For full-year 2026, management guided to bookings growth of roughly 10.5%, revenue growth of roughly 16.1%, and an adjusted EBITDA margin of approximately 25.7%, per Munson on the Q1 2026 earnings call.

Q2 2026 bookings growth is guided to approximately 6%, reflecting a tough comparable that included the initial rollout of Energy, a price increase on the Super tier, and strong advertising performance a year ago.

Duolingo repurchased 514,000 shares under its $400M buyback authorization, representing approximately 1% of fully diluted shares outstanding, and exited Q1 with over $1B in cash and no debt, per Munson on the Q1 2026 earnings call.

Duolingo Stock Financials: Q1 2025 Through Q4 2025

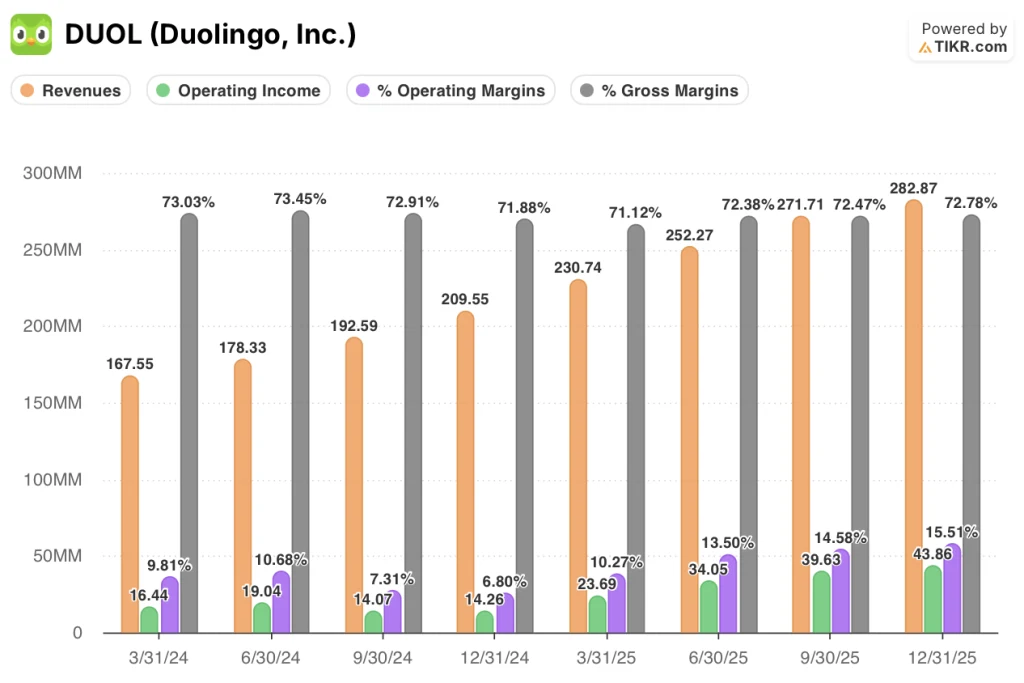

Duolingo stock’s income statement shows a sustained operating leverage story across 2025, with operating margins expanding every quarter from 10.3% in Q1 to 15.5% by Q4.

Revenue grew sequentially each quarter through 2025: $230.74M in Q1, $252.27M in Q2, $271.71M in Q3, and $282.87M in Q4, with year-over-year growth rates ranging from 38% to 42% across the four quarters.

Gross margin held in a tight band throughout the year, moving from 71.1% in Q1 2025 to 72.8% in Q4 2025, a stable performance given the accelerating AI content investment running through cost of goods sold.

Operating income expanded from $23.69M in Q1 2025 to $43.86M in Q4 2025, a near-doubling over four quarters driven by revenue scale outpacing operating expense growth.

Operating margin at 15.5% in Q4 2025 represents a significant step-up from the 6.8% trough in Q4 2024, reflecting both revenue leverage and controlled headcount spending.

Management guided Q2 2026 gross margin to approximately 71%, with a gradual drift toward approximately 69% by Q4 2026 as more AI-powered features are embedded in the product, per Munson on the Q1 2026 earnings call.

What Does the Valuation Model Say?

The TIKR model prices Duolingo stock at $208.70, implying approximately 89% upside from the current price of $110.23 over a 4.7-year horizon, with a 14.7% annualized return.

The mid-case model assumes a revenue CAGR of 9.8% and a net income margin of 32.2% from 2025 through 2035, with EPS growing at a 3.9% CAGR as P/E multiples compress at roughly 4.5% annually.

Q1 2026 reinforced the model’s margin expansion trajectory: adjusted EBITDA at 29% of revenue already exceeds the full-year 25.7% guidance target, suggesting front-loaded profitability before heavier AI investment lands in H2.

Duolingo stock at $110 prices in near-term bookings headwinds without crediting the margin improvement and DAU flywheel that is already showing up in the income statement.

The investment case is incrementally stronger after Q1: execution matched guidance, cash generation is on track for $350M+ this year, and the product roadmap is moving faster than the growth deceleration implies.

The Q1 report confirms execution discipline, but the real debate for Duolingo stock is whether sustained 20% DAU growth is enough to reignite bookings growth above 10% once the 2025 monetization comparables normalize.

What Has to Go Right

- DAU growth holds at approximately 20% through 2026 as guided, providing the compounding user base that eventually converts into subscription growth beyond the current roughly 12% paid penetration rate

- Longer free trials (1-month and potential 3-month experiments) drive bookings growth in H2 2026 without eroding DAU gains, validating the non-friction monetization thesis

- Video call expansion into the Super tier lifts average subscription revenue per user, with early pricing tests already confirming users “are willing to pay more,” per von Ahn on the Q1 2026 earnings call

- Asia performance marketing scales profitably, with China already achieving positive unit economics that management expects to extend across the region

What Could Still Go Wrong

- Full-year 2026 bookings growth guided at only roughly 10.5% reflects a genuine deceleration from the 38%+ revenue growth rates in 2025, raising the question of whether the monetization reset runs longer than one year

- Gross margin is guided to compress from 72.8% in Q4 2025 to approximately 69% by Q4 2026 as AI content costs scale, and any faster adoption of AI features could push margins below that floor

- Top-of-funnel growth has been “about flat,” per von Ahn on the Q1 2026 earnings call, and MAU deceleration limits the ceiling on eventual paid subscriber additions regardless of conversion rate improvements

- Max tier cannibalization risk is unresolved: management is running experiments that could lower Max pricing or restructure the tier entirely, creating near-term revenue mix uncertainty

Should You Invest in Duolingo, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Duolingo stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Duolingo, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DUOL stock on TIKR for Free →