Key Stats for Coca-Cola Stock

- 52-Week Range: $62 to $82

- Current Price: $79

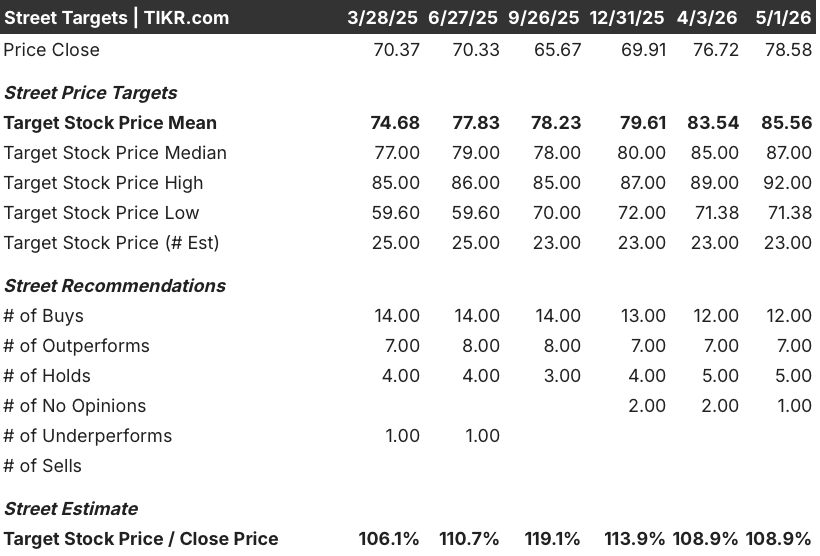

- Street Mean Target: $86

- Street High Target: $92

- Analyst Consensus: 12 Buys / 7 Outperforms / 5 Holds / 0 Underperforms

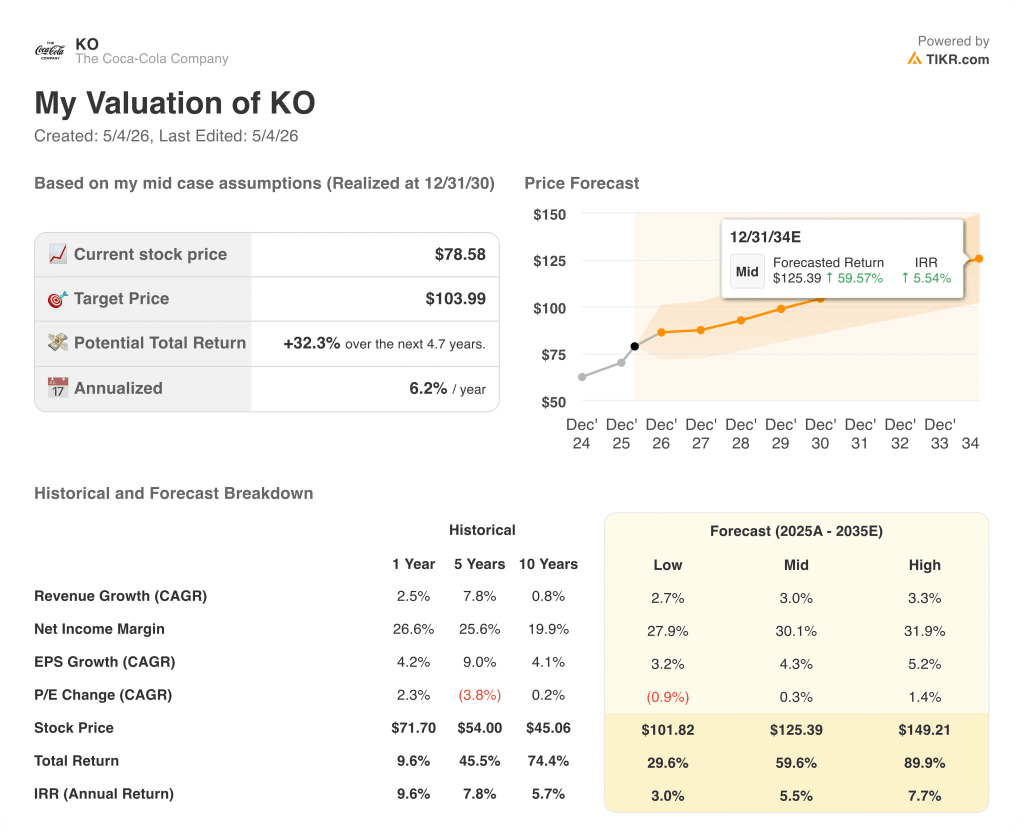

- TIKR Model Target (Dec. 2030): $104

What Happened?

The Coca-Cola Company (KO), the world’s largest nonalcoholic beverage company with 32 billion-dollar brands spanning sparkling, water, dairy, and tea categories, raised its full-year earnings outlook on April 28 as first-quarter results topped expectations, sending Coca-Cola stock up more than 5% on the day.

Revenue for the quarter ended April 3 came in at $12.47 billion, a 12% year-over-year increase that beat analyst estimates of $12.24 billion and was partly lifted by six additional selling days versus the prior-year period.

The sharpest number in the print was adjusted EPS of $0.86, an 18% jump from the same quarter last year, as operating expense efficiencies and a lower effective tax rate combined with 10% organic revenue growth to drive per-share earnings well above the $0.81 consensus.

Incoming CEO Henrique Braun, who formally took the top role on March 31, stated on the Q1 2026 earnings call that “we delivered strong first quarter results despite a complex external environment,” citing 3% global unit case volume growth and value share gains for the 20th consecutive quarter.

The path forward is anchored in three compounding drivers: new capacity for the fast-growing fairlife protein milk brand coming online at the Webster facility in Q2, a FIFA World Cup activation spanning 75 stops across 30 countries, and a pending sale of Coca-Cola Beverages Africa that management expects will lift consolidated margins in the second half of 2026.

Wall Street’s Take on KO Stock

The Q1 beat matters not because of the extra selling days but because of what it signals about KO’s earnings trajectory under a new leadership team navigating a commodity-pressured environment better than its consumer staples peers.

KO’s normalized EPS reached $3 in 2025 after years of building toward that milestone, and consensus now expects around $3.26 for 2026, a roughly 9% increase, as the pending divestiture of Coca-Cola Beverages Africa removes a structural drag and favorable currency tailwinds add approximately 3 points of EPS support for the full year.

Of the 24 analysts with active ratings on KO, 19 sit in buy or outperform territory, with a mean price target of $85.56 that implies roughly 8% upside from $79, and Wall Street is specifically watching whether the FIFA World Cup activation in North America and Latin America converts volume momentum into sustained organic revenue growth of 4% to 5% through the second half.

The target spread from $71.38 to $92.00 captures a genuine debate: bulls are pricing in EBITDA growing around 8% in 2026 on the back of operating expense efficiencies and the Africa divestiture, while bears cite mounting pressure on bottler economics tied to elevated aluminum and PET resin prices from the Iran-related supply disruption.

CFO John Murphy noted on the Q1 earnings call that net debt leverage of 1.6x EBITDA sits below the targeted range of 2 to 2.5x, giving KO financial flexibility that few consumer staples names currently hold.

Sustained packaging cost inflation, especially for aluminum and PET resin, is the one pressure point that could force bottling partners to absorb margin compression that KO’s own P&L has so far avoided.

Q2 results and management’s update on the fairlife capacity ramp will confirm whether the 8% to 9% full-year EPS guidance range is tracking at the midpoint or above; the specific figure to watch is organic revenue growth against the 4% to 5% full-year target.

What Does the Valuation Model Say?

The TIKR mid-case model assigns Coca-Cola a target price of around $104, reached by December 2030, anchored to a revenue CAGR of 3% from 2025, net income margins expanding toward 30% by the end of the forecast period, and an EPS CAGR of roughly 4%, inputs that look conservative relative to the earnings acceleration already visible in the Q1 print and the updated 2026 guidance.

At $79, with the mid-case implying a total return of around 60% over the next 4.7 years and the underlying margin expansion trend intact across every income statement layer for four consecutive years, KO appears undervalued for a Dividend King whose own history supports a forward P/E closer to 26x, not the 24x on offer today.

The central question for Coca-Cola stock is whether KO can sustain margin expansion and volume growth simultaneously in an environment where commodity costs are rising and consumer spending is bifurcating between value and premium.

What Has to Go Right

- The fairlife capacity ramp at the Webster facility, expected online in Q2, removes a production ceiling on one of KO’s fastest-growing profit pools, with management signaling further plant investments across the U.S. over the next 3 to 5 years

- The pending sale of Coca-Cola Beverages Africa, expected in the second half of 2026, mechanically lifts consolidated operating margins by removing a lower-margin bottling segment, with the CFO explicitly flagging more margin expansion as a second-half tailwind

- FIFA World Cup activation across 30 countries, including North America where KO reported 4% volume growth in Q1, drives beverage occasion incidence during the highest-traffic sports event in the world

- KO locked in commodity hedges before the current Middle East disruption, and a tax rate reduction to 19.9% supports consensus EPS reaching around $3.26 in 2026 versus $3.00 in 2025

What Could Go Wrong

- Aluminum and PET resin prices remain elevated as Iran-related disruptions keep the Strait of Hormuz constrained, putting pressure on bottler economics that KO cannot fully offset at the concentrate level, with aluminum can shortages already impacting Diet Coke supply in India

- Mexico’s sugar tax, implemented at the start of 2026, is generating geographic mix headwinds in Latin America, with volume declines that Brazil and Central America are currently but not necessarily permanently offsetting

- The $2.44 billion BodyArmor trademark carrying value, following a $960 million impairment charge in Q4 2025, remains a risk if the sports hydration category softens under prolonged consumer spending pressure

- Revenue growth has decelerated from 17.1% in 2021 to 1.9% in 2025, and a failure to reaccelerate toward the 4% to 5% organic target in the back half of 2026 would erode the earnings multiple investors are currently assigning to KO

Should You Invest in The Coca-Cola Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Coca-Cola Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Coca-Cola Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KO stock on TIKR for Free →