Key Stats

- CHD price: $96 (May 1, 2026)

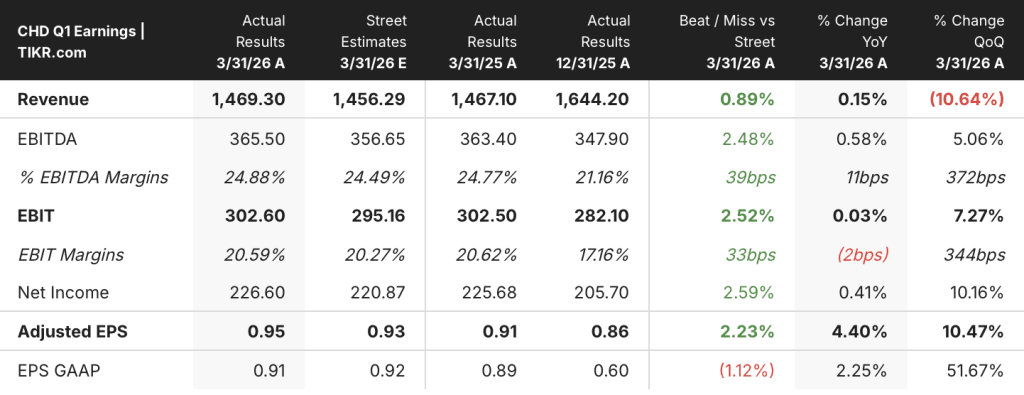

- Q1 2026 revenue: $1.47B, +0.15% YoY

- Q1 2026 organic sales growth: +5%

- Q1 2026 adjusted EPS: $0.95, +4.4% YoY

- Full-year 2026 organic sales guidance: +3% to +4%

- Full-year 2026 adjusted EPS growth guidance: +5% to +8%

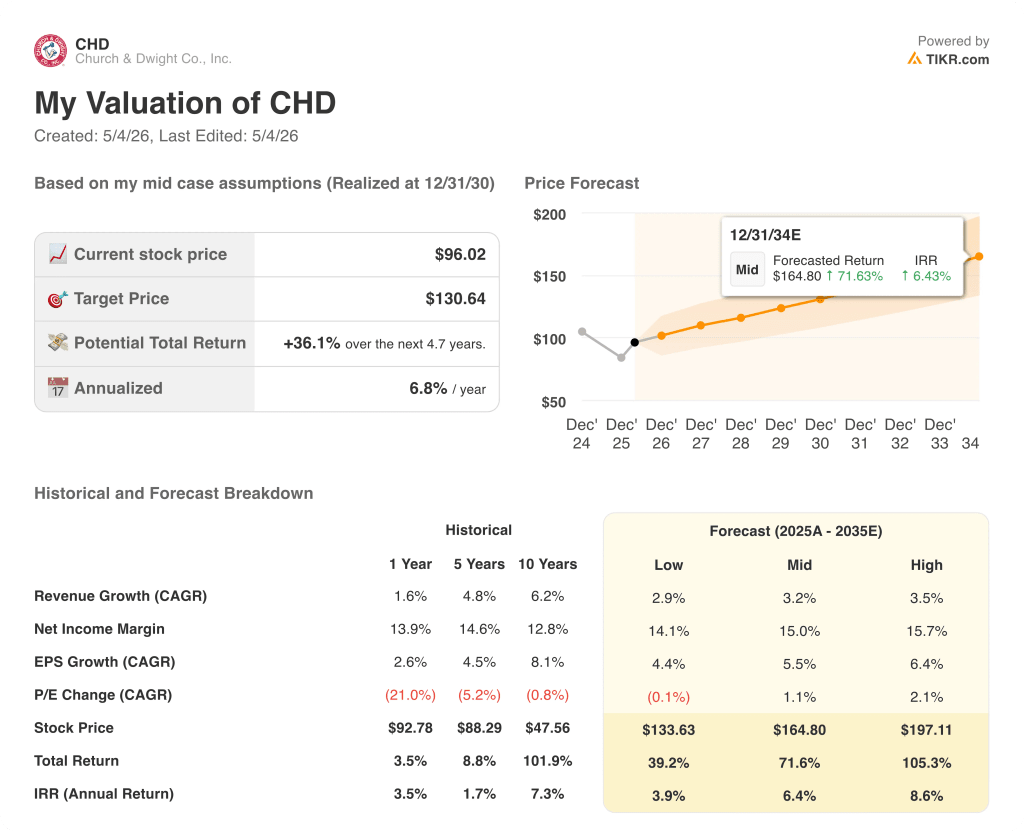

- TIKR model price target: $131

- Implied upside: ~36%

Church & Dwight Q1 2026 Earnings Breakdown

Church & Dwight beat its own Q1 outlook across every key metric, despite starting 2026 with a portfolio headwind that would have pushed reported revenue down 8% on its own.

Church & Dwight stock (CHD) posted Q1 organic sales growth of 5%, above its 3% outlook, with adjusted EPS of $0.95, up 4.4% year over year and ahead of the $0.92 guidance figure.

Reported net sales came in at $1.47B, up just 0.2% year over year, but that headline understates the organic performance: according to CFO Lee McChesney on the Q1 earnings call, the company’s 2025 portfolio actions created an 8% structural drag on reported revenue, which organic growth and the Touchland acquisition fully offset.

The U.S. Consumer segment led growth with organic sales up 5.4%, driven almost entirely by volume.

THERABREATH reached record share gains of 3.5 points, bringing its mouthwash share to 24.1% and cementing its number two position in total mouthwash, according to CEO Rick Dierker on the Q1 call.

ARM & HAMMER laundry detergent hit record shares in total laundry, growing consumption 4.1% against category growth of 2.7%, while ARM & HAMMER cat litter consumption rose 6.8% with share climbing 0.4 points to 24.6%, according to Dierker.

HERO outpaced its category and maintained share leadership, with Dierker noting HERO is 2x larger than the next competitor.

OXICLEAN remains a soft spot: distribution loss from a large club retailer one year ago continued to weigh on share, though the segment’s sales growth improved through the quarter and surpassed internal expectations.

Touchland consumption grew roughly 12% to 13% on an all-in basis including untracked channels, though tracked consumption appeared down 20% due to the comparison against heavy Q4 holiday multipack activity, according to Dierker.

International organic sales grew 3.7%, with THERABREATH, HERO, and BATISTE leading, partially offset by lower Middle East regional sales.

On the cost side, McChesney flagged $25M to $30M in incremental inflation from Middle East conflict, covering oil-based derivatives, diesel, resin, and surfactants, but the company is offsetting the full amount through productivity programs rather than price increases.

Church & Dwight reiterated its full-year 2026 guidance: organic sales growth of 3% to 4%, reported sales decline of approximately 1.5% to 0.5% due to portfolio actions, gross margin expansion of approximately 100 basis points, and adjusted EPS growth of 5% to 8%.

Q2 guidance calls for reported sales decline of approximately 1%, organic growth of approximately 3%, gross margin expansion of 50 basis points, and adjusted EPS of $0.88.

Church & Dwight Stock Financials

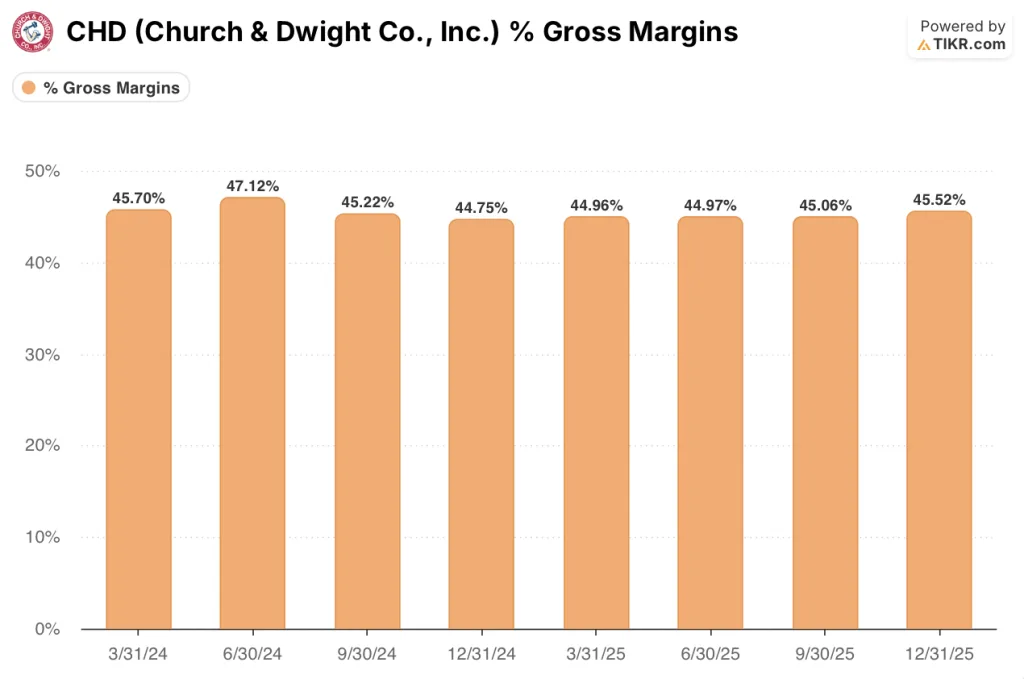

Church & Dwight stock enters 2026 with a margin recovery arc that began in Q3 2025 after a soft first half of last year.

Gross margin had declined from 45.7% in Q1 2024 to 45% by Q1 2025, then held at 45% through Q2 2025 before recovering to 45.1% in Q3 2025 and 45.5% in Q4 2025.

Q1 2026 adjusted gross margin reached 46.4%, a 130-basis-point increase year over year, according to McChesney.

The expansion was driven by 150 basis points from productivity programs, 110 basis points from higher-margin acquisitions and portfolio actions, and 50 basis points from volume, price, and mix, partially offset by 190 basis points of inflation and tariff costs, according to McChesney.

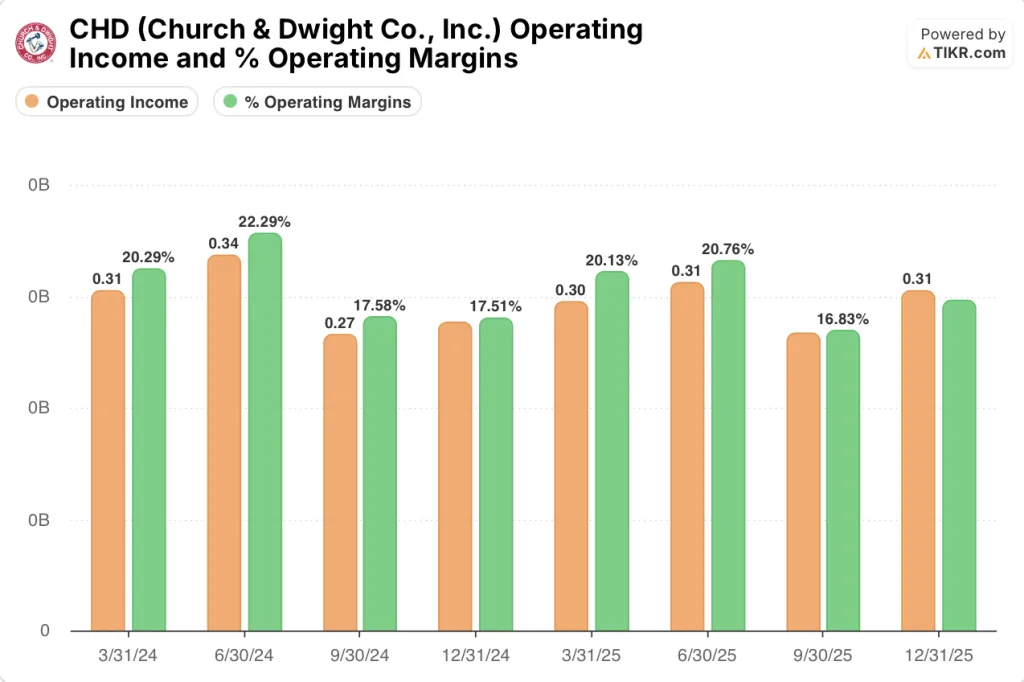

Operating income has followed a similar trajectory: $300M in Q1 2024, $280M in Q4 2024, a softer $270M in Q3 2025, and $310M in Q4 2025.

Operating margin showed comparable movement, compressing from 20.3% in Q1 2024 to 16.8% in Q3 2025 before recovering to 18.6% in Q4 2025.

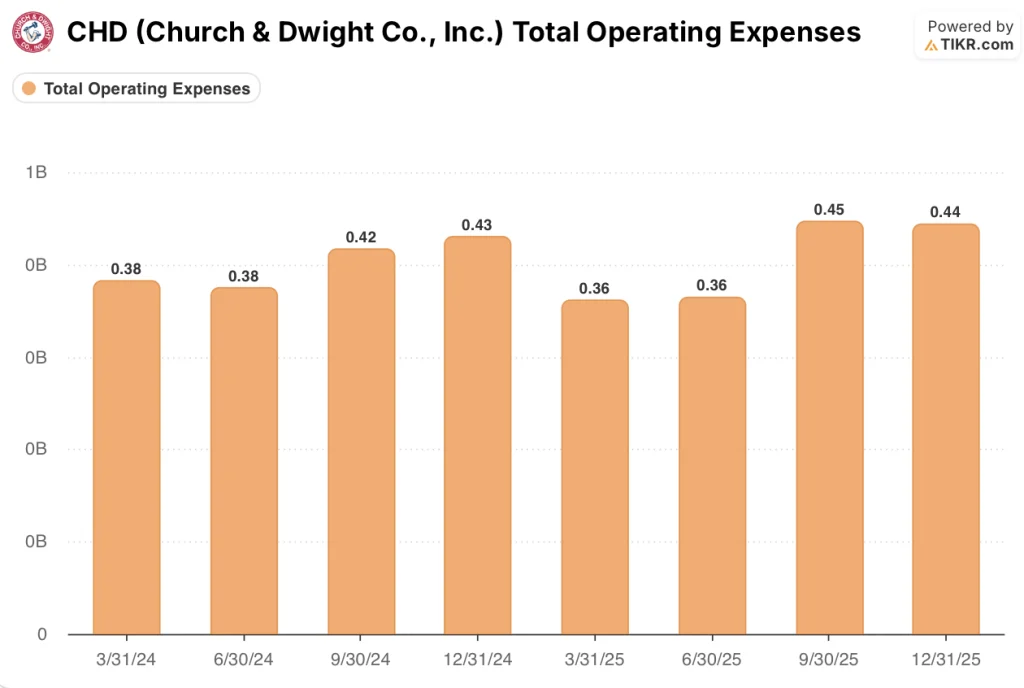

Total operating expenses rose from $360M in Q1 2025 to $440M to $450M in the back half of the year, and McChesney noted on the Q1 call that adjusted SG&A increased 110 basis points year over year, driven primarily by the inclusion of Touchland’s SG&A and amortization expense, with the same dynamic expected to persist through the first half before moderating.

What Does the Valuation Model Say?

The TIKR model prices Church & Dwight stock at a mid-case target of $131 from the current $96, implying approximately 36% total upside over ~5 years with an annualized return of around 7%.

The model assumes a revenue CAGR of 3% (mid case) and a net income margin of 15%, both achievable given Q1’s organic momentum and the structural tailwinds from portfolio rationalization.

The Q1 report strengthens the risk/reward picture at current prices: the organic growth rate came in above guidance, gross margin is expanding ahead of the prior-year pace, and management maintained the full-year outlook despite absorbing a new $25M to $30M cost headwind.

Church & Dwight stock does not offer explosive upside, but the mid-case scenario reflects a low-volatility compounder where execution, not growth rerating, is the primary driver.

Organic growth re-acceleration is confirmed, but the investment case now hinges on whether margin expansion holds as incremental cost pressures layer in through the second half.

Should You Invest in Church & Dwight Co., Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Church & Dwight Co., Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Church & Dwight Co., Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CHD stock on TIKR for Free →