Key Stats

- Current price: ~$495 (May 1, 2026 close)

- Q1 2026 revenue: $8.4B, up ~16% YoY

- Q1 2026 adjusted EPS: $4.60, up ~23% YoY

- Q2 2026 net revenue growth guidance: low end of low double-digits (currency-neutral, ex-inorganic)

- Full-year 2026 net revenue growth guidance: high end of low double-digit range (currency-neutral, ex-inorganic)

- TIKR model price target: ~$904

- Implied upside: ~82%

Mastercard Stock Posts 16% Revenue Growth in Q1 2026

Mastercard stock (MA) delivered Q1 2026 net revenue of $8.4B, up ~16% year-over-year, with adjusted EPS of $4.60, up ~23% from $3.73 in the prior-year quarter.

Value-Added Services and Solutions was the standout driver, with net revenue up 18% on a currency-neutral basis, according to Chief Financial Officer Sachin Mehra on the Q1 2026 earnings call.

Payment network net revenue grew 8% on a currency-neutral basis, driven by domestic and cross-border transaction and volume growth.

Cross-border volume grew 13% globally for the quarter, reflecting continued strength in both travel and non-travel-related spending.

CEO Michael Miebach noted the quarter’s momentum directly: “Building on 2025 momentum, ’26 is off to an excellent start. Net revenue growth was up 12% and net income up 15% in the first quarter on a year-over-year non-GAAP currency-neutral basis.”

The Middle East conflict emerged as the primary headwind, with cross-border travel showing sequential pressure beginning in March, according to Sachin Mehra on the Q1 2026 earnings call.

Mastercard repurchased $4B worth of stock during Q1, with an additional $1.7B repurchased through April 27, accelerating the pace given current valuation levels and long-term conviction, according to Sachin Mehra on the Q1 2026 earnings call.

For Q2 2026, management guided net revenue growth to the low end of low double-digits on a currency-neutral basis, with the Middle East conflict representing the largest incremental headwind; absent the conflict, Q2 growth would have been roughly in line with Q1.

Full-year 2026 net revenue guidance was maintained at the high end of a low double-digit range on a currency-neutral basis, with a ~1.5 point tailwind expected from foreign exchange.

Mastercard Stock: What the Income Statement Shows

Mastercard’s Q1 2026 income statement shows sustained operating leverage, with revenue growth accelerating above 15% while operating margin held above 58%, even as the company absorbs increased strategic investment spending.

Revenue has grown each quarter over the past two years, moving from $7.0B in Q2 2024 to $8.4B in Q1 2026, a consistent upward arc with no quarters of decline in the visible window.

Operating income reached $4.9B in Q1 2026, up from $4.3B in Q1 2025, a 14% year-over-year increase.

Operating margin was 58% in Q1 2026, compared to 59% in Q1 2025, a modest one-point compression.

The compression is partly attributable to the 9% increase in operating expenses year-over-year, driven by strategic infrastructure investment and geographic expansion, according to Sachin Mehra on the Q1 2026 earnings call.

Operating margin peaked at 60% in Q2 2025 and has trended modestly lower since, settling at 58% this quarter, though the absolute dollar expansion in operating income confirms this is investment-driven, not cost-driven.

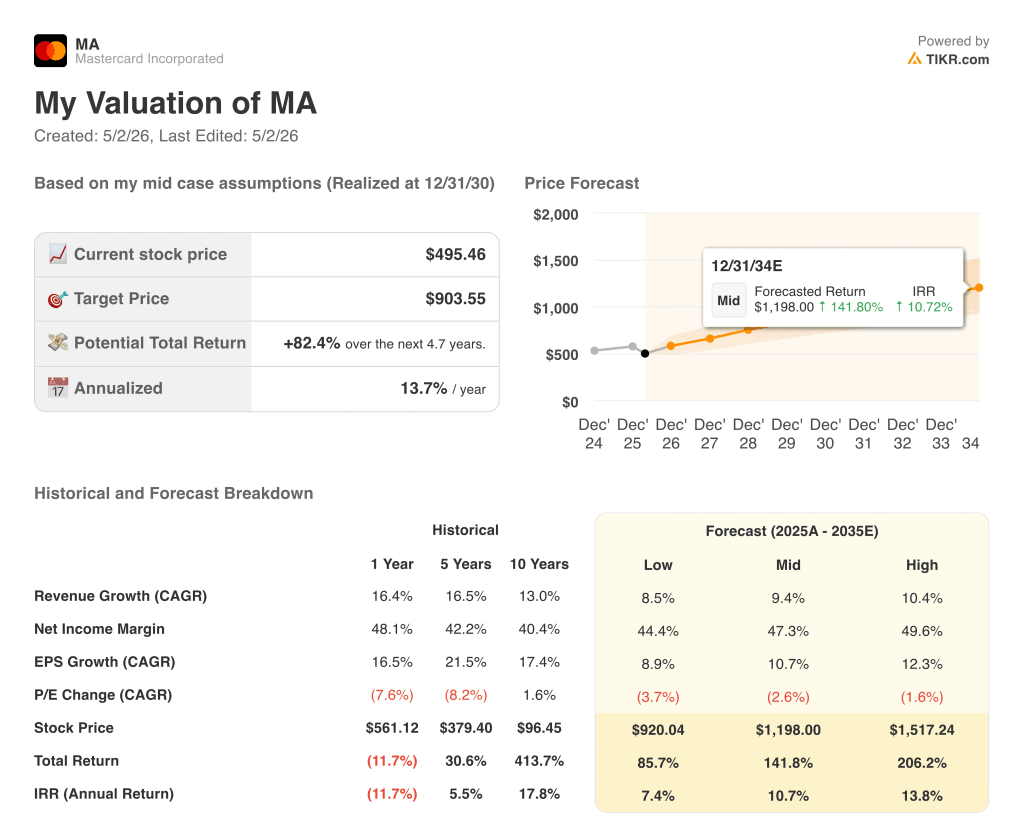

What Does the Valuation Model Say?

The TIKR model prices Mastercard stock at ~$904, implying ~82% upside from the current ~$495 price over the next ~5 years, with an annualized return of ~14%.

The mid-case model assumes a revenue CAGR of around 9% and a net income margin of ~47%, both well within reach given the 16% YoY revenue growth and 48% net income margin delivered over the past year.

Q1 2026 results reinforce the base case: VAS growing at 18%, operating income expanding year-over-year, and buybacks accelerating at current levels all tighten the gap between where the stock trades and where the model says it belongs.

The investment case for Mastercard stock is incrementally stronger after this quarter, with the key risk (Middle East cross-border headwind) already sized, guided, and framed as temporary.

The debate isn’t whether Mastercard grows, it’s whether a temporary cross-border headwind can hold back a business generating 18% VAS growth and $4B in quarterly buybacks.

Bull Case

- VAS grew 18% organically in Q1 2026, with no acquisition contribution; security solutions, digital/authentication, and consumer acquisition all cited as strong demand drivers

- Full-year currency-neutral guidance held at the high end of low double-digits despite a Middle East headwind, supported by a Q1 beat and healthy underlying consumer spending

- Management sized the GCC and Israel cross-border impact at roughly 6% of total cross-border volume, a contained exposure with a guided Q2 peak and progressive H2 recovery

- Accelerated buybacks ($5.7B in Q1 and through late April) at current prices reflect management’s conviction and will mechanically support EPS growth even if revenue softens slightly

Bear Case

- Q2 net revenue guidance landed at the low end of low double-digits, a step down from Q1’s ~16% growth, with the Middle East conflict the primary driver and timeline resolution uncertain

- Cross-border travel declined sequentially from Q1 into the first four weeks of April, with portfolio shifts compounding the conflict-related pressure and extending impact into H2

- Switched transaction growth of 9% (or 10% ex-Capital One migration) continues to lag historical low-teens ranges; geographic mix and average ticket dynamics may keep this below prior-cycle highs

- Operating expenses grew 9% in Q1, at the guided low-double-digit pace for the full year, which means any revenue softness beyond the current guidance range compresses margins with limited offset

Should You Invest in Mastercard Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Mastercard Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MA stock on TIKR for Free →