Key Takeaways:

- Capital One Financial operates as a bank holding company providing credit cards, auto loans, and consumer banking services, and completed its transformative acquisition of Discover Financial in 2026.

- COF stock trades near $190, down around 23% year to date, as rising credit card charge-offs and integration costs weighed on Q1 2026 results.

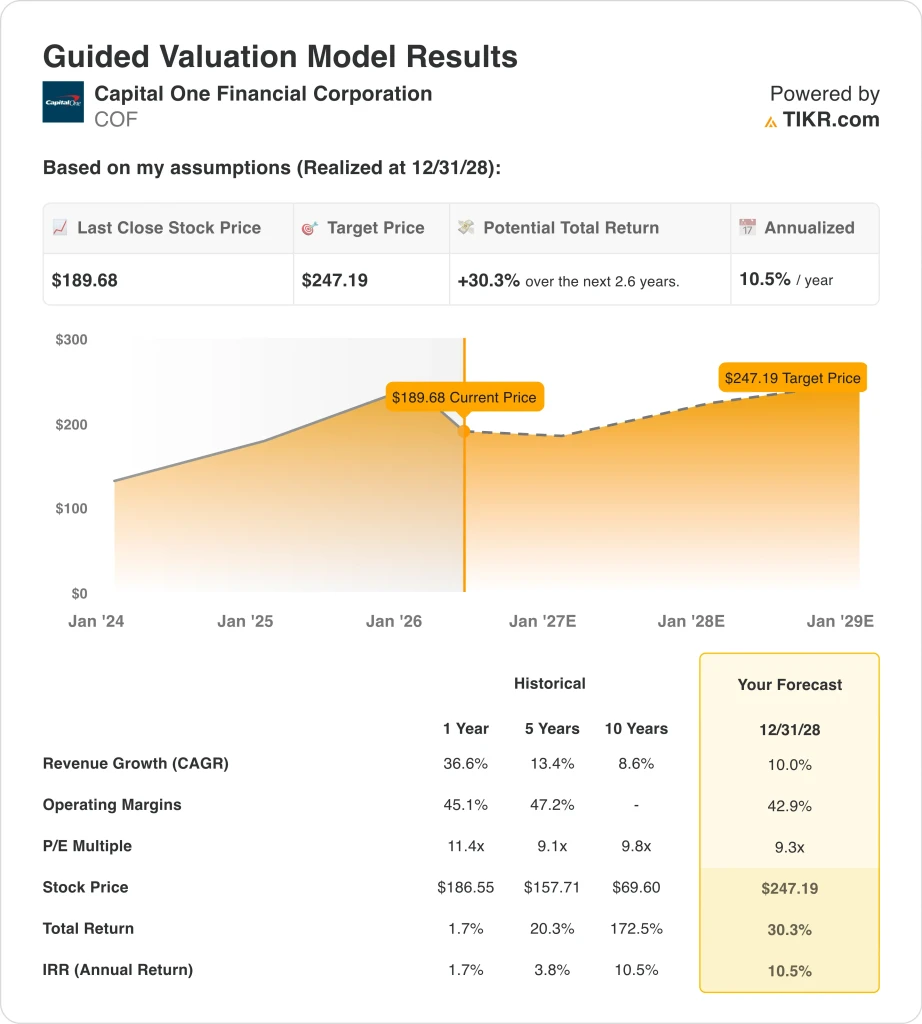

- COF stock could rise from $190 to around $247 per share by December 2028, based on 10% annual revenue growth, 42.9% operating margins, and a 9.3x P/E multiple.

- That would be a 30.3% total return, or around 10.5% annualized over the next 2.6 years.

What Happened?

Capital One Financial Corporation (COF) operates as a bank holding company providing credit cards, auto loans, commercial lending, and consumer banking services. The company completed its long-awaited acquisition of Discover Financial Services in 2026, creating a combined payments and lending platform with a proprietary card network that can compete directly with Visa and Mastercard for merchant acceptance.

Capital One also closed its $5.15 billion acquisition of Brex, a corporate fintech platform targeting startups and growing businesses, in April 2026. These two deals repositioned Capital One from a primarily domestic consumer lender into a broader financial technology and payments platform.

Q1 2026 results were mixed. Capital One reported Q1 net interest income of $12.15 billion and net income of $2.2 billion, but total revenue dropped 2% to $15.2 billion as higher provisions for bad loans weighed on results.

The domestic credit card net charge-off rate, which measures loans written off as uncollectible, rose to 5.09% in March 2026, reflecting continued pressure on borrowers in a higher interest rate environment. One Reuters analysis described the quarter as Capital One “buying time, not immunity on expenses.” Investors grew concerned about the credit trajectory.

Analyst consensus remains constructive despite the Q1 miss. The street consensus target price of around $257 implies more than 35% upside from current levels. Capital One also rebranded its Spark Miles business cards under the Venture brand umbrella in April, signaling continued investment in its premium card franchise.

Investor tone is worried but measured on the longer-term thesis. The Discover network is a powerful strategic asset, and the Brex deal adds commercial fintech exposure. Here’s why Capital One stock could still deliver above-average returns as the integration thesis unfolds over the next two to three years.

What the Model Says for COF Stock

We analyzed the upside potential for Capital One stock based on the transformative scale created by the Discover acquisition, the company’s strong credit card franchise, and the potential for payment network economics to drive earnings growth as the combined business integrates.

Based on estimates of 10% annual revenue growth, 42.9% operating margins, and a normalized P/E multiple of 9.3x, the model projects Capital One stock could rise from $190 to around $247 per share.

That would be a 30.3% total return, or a 10.5% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for COF stock:

1. Revenue Growth: 10%

Capital One’s Q1 2026 revenue of $15.2 billion was down 2% from Q1 2025, as integration costs and credit provisions rose. But the 1-year historical revenue growth rate is 36.6%, boosted by the inclusion of Discover’s financials. And the 10-year historical CAGR of 8.6% reflects the company’s long-run organic growth capability. Based on analysts’ consensus estimates, we used 10% revenue growth, reflecting moderation from acquisition-boosted levels but still above the long-run organic trend.

The forward two-year revenue CAGR sits near 12.2% by analyst consensus. The 10% assumption is slightly below consensus, reflecting near-term integration headwinds and the potential drag from elevated credit losses in 2026. But Discover’s payment network and Brex’s commercial banking capabilities should contribute meaningfully to revenue as synergies are captured over the next two years.

Capital One’s credit card business benefits from the Discover network’s lower interchange fees for merchants. This structure could help expand merchant acceptance and the total addressable market over time. So the 10% assumption is achievable and grounded in both historical trends and the combined company’s strategic positioning.

2. Operating Margins: 42.9%

Capital One’s 1-year historical operating margin of 45.1% reflects the high-margin nature of a consumer credit franchise. But Q1 2026 saw temporary compression as provisions for bad loans rose and integration expenses increased. The 5-year historical operating margin of 47.2% shows the company’s capacity to generate strong margins in a normal credit environment. Based on analysts’ consensus estimates, we used 42.9% operating margins, reflecting compression from elevated credit costs before normalization.

A 42.9% operating margin is achievable if the charge-off rate stabilizes and integration costs decline as the Discover deal matures. Management is actively managing credit quality and cost structure on both fronts. The Brex deal adds a lower credit-risk commercial segment that could also provide a margin-accretive mix shift over time.

The March 2026 domestic credit card charge-off rate of 5.09% is elevated but not unprecedented. If charge-offs moderate as the credit cycle normalizes, operating margins should recover toward the 45% range seen historically. And Discover’s payment network scale advantages could reduce operating costs per transaction as adoption grows.

3. Exit P/E Multiple: 9.3x

Capital One trades at a next twelve-month P/E of 9.3x, which is low for a financial services company of its scale and brand strength. The LTM P/E of 44.2x reflects temporarily depressed earnings during the integration period. Comparable consumer finance peers typically trade at 8x to 15x forward earnings. Based on analysts’ consensus estimates, we maintained a 9.3x exit P/E multiple, reflecting the credit risk embedded in the portfolio and ongoing integration uncertainty through 2028.

A 9.3x multiple is conservative for a company that owns the Discover network alongside Capital One’s established card brand. The street consensus target of around $257 implies a higher embedded multiple, suggesting analysts expect meaningful earnings normalization ahead. And a modest re-rating toward 11x or 12x as credit conditions improve could add significant upside beyond our base case.

The 10.5% annualized return at a 9.3x multiple already sits at the threshold many investors consider attractive. So the current setup offers compelling upside even without assuming any multiple expansion. And the combination of earnings growth and a potential re-rating creates a constructive longer-term case for patient investors.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for COF stock through 2030 show varied outcomes based on Discover integration progress and credit quality normalization (these are estimates, not guaranteed returns):

- Low Case: Credit losses remain elevated, and integration costs drag earnings longer than expected → 6.5% annual returns

- Mid Case: Discover synergies emerge on schedule and charge-offs normalize toward historical averages → 8.4% annual returns

- High Case: Network economics outperform and commercial Brex business scales faster than expected → 9.8% annual returns

Going forward, Capital One’s stock will be primarily driven by two factors: the pace at which credit charge-offs normalize and the speed at which Discover network synergies begin to flow through to earnings.

The annual meeting on May 8, 2026, and Q2 2026 earnings in July are the next major disclosure points for investors to watch. Even in the low case, annual returns remain positive at 6.5%, suggesting the market may have already priced in a reasonable degree of the near-term downside risk from elevated credit costs.

See what analysts think about COF stock right now (Free with TIKR) >>>

Should You Invest in Capital One Financial?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up COF, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track COF alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Capital One Financial stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!