Key Stats for DUOL Stock

- Current Price: $110.23

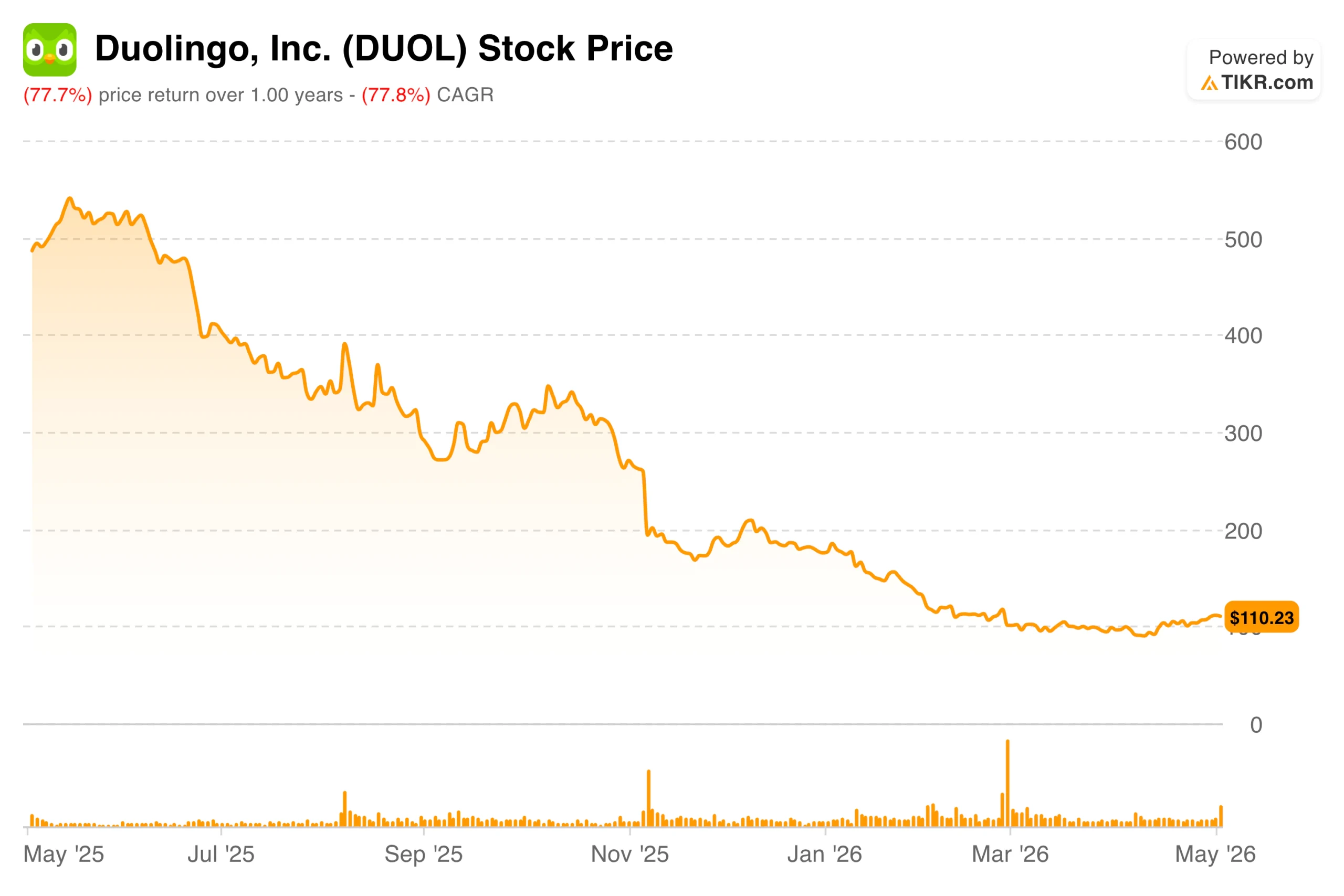

- 52-Week Range: $87.89 to $544.93

- Street Mean Target: ~$105

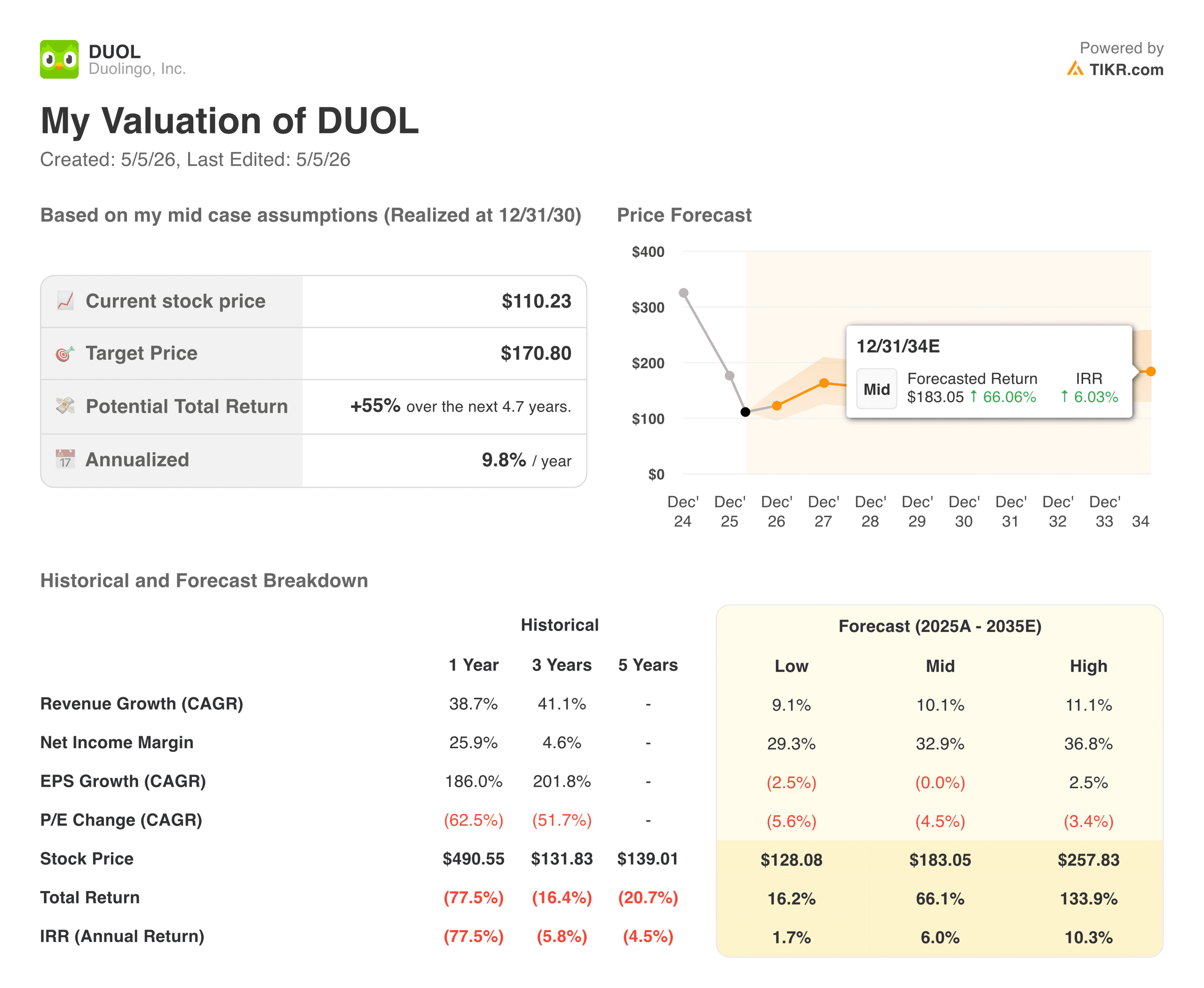

- TIKR Model Target Price: ~$170

- Implied Upside (TIKR): ~55%

Value your favorite stocks like DUOL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Beat on Everything. Still Down 14%, Here’s Why

Duolingo (DUOL) just reported one of the more confusing earnings prints of 2026. Revenue came in at $292 million, up about 27% year over year. EPS of $0.89 cleared estimates of $0.75 by around 18%. Adjusted EBITDA margin hit 29% for the quarter, well above the company’s own full-year target of around 25%. Every number that mattered came in ahead of expectations, and the stock still dropped nearly 14% overnight.

Two things spooked investors. Q2 bookings growth is expected to come in around 6%, well below the pace of recent quarters. Management attributed this to a tough comparison from last year, when a subscription price increase and a new monetization feature drove an unusual spike in the year-ago period.

Alongside that, gross margins are expected to compress as AI-powered features scale across the product. Per-unit AI content costs are actually falling, but total usage is growing fast enough to more than offset those savings, with gross margin expected to exit the year around 69%.

This stock was trading above $500 less than a year ago and has since fallen roughly 78%. Coming in with strong results only to guide conservatively reinforced a concern that has followed DUOL through most of 2026: that the growth story is decelerating faster than the multiple currently assumes.

See analysts’ growth forecasts and price targets for DUOL (It’s free) >>>

The Street Sees No Upside. Is It Missing the Bigger Picture?

Wall Street’s consensus target sits around $105, which is actually below where the stock was trading before earnings. After one of the steeper declines in consumer tech over the past year, the average analyst covering this company sees no upside at current levels.

The bear case comes down to two things: flat top-of-funnel user growth in Q1, and lingering skepticism around subscriber conversion. Hundreds of millions of people have downloaded this app, but the share of those users who actually pay for a subscription remains low. Whether that gap represents a genuine opportunity or a structural ceiling on the business is the central debate right now.

The bull case is about AI, and it is more concrete than it might sound. Duolingo has increased content production velocity by roughly 10 times over the past two years, publishing over 20,000 course units in Q1 alone. CEO Luis von Ahn has been consistent in framing this as early innings, and management was explicit that 2026 is an investment year, with the financial payoff expected in the years that follow. Making a judgment call on whether the current deceleration is temporary or structural is what makes this stock genuinely difficult to own right now.

The Underlying Business Is Stronger Than the Stock Price Suggests

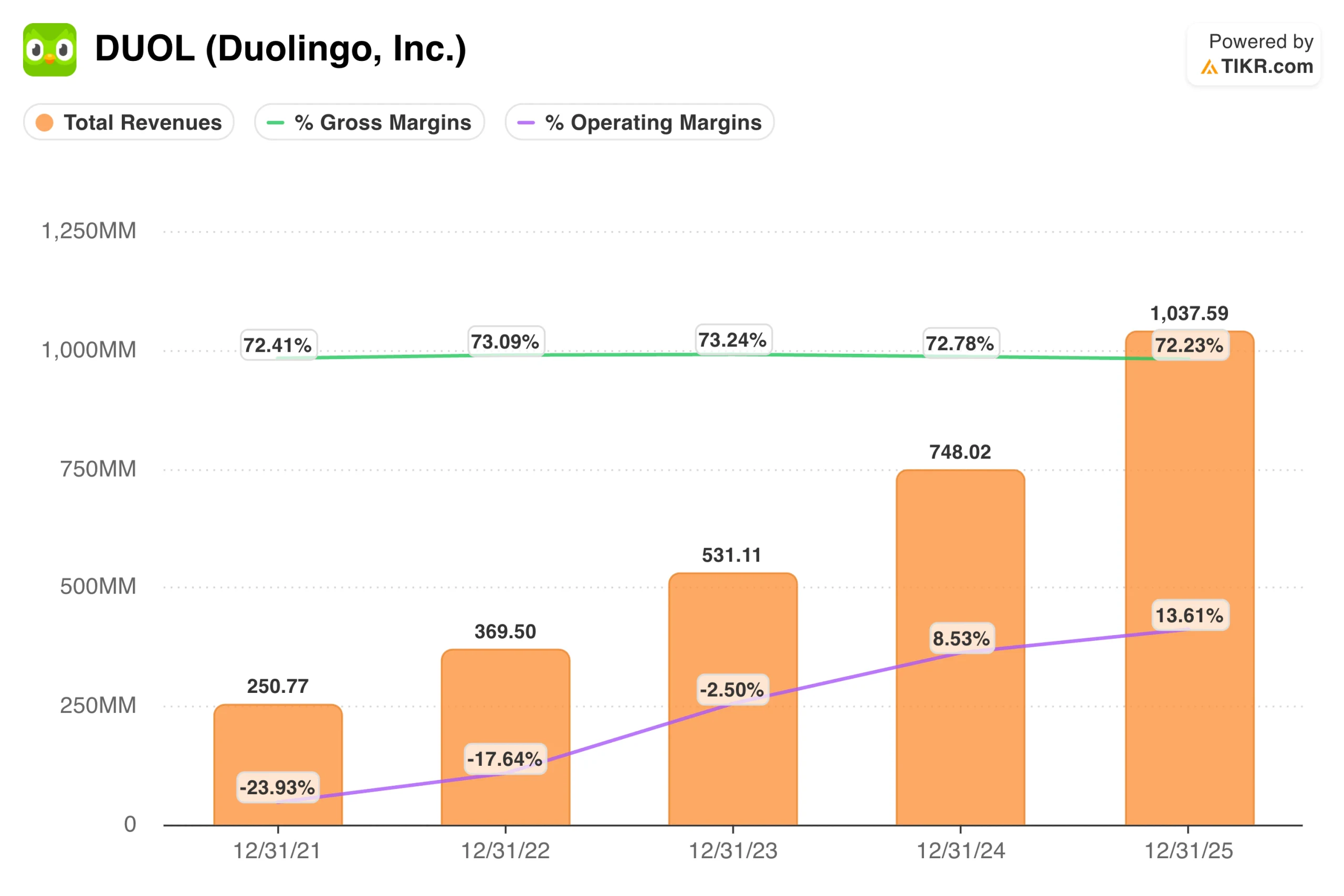

Stripping away the near-term noise, the financial profile here is genuinely solid. Revenue has compounded at around 40% annually over the past three years. Operating margin expanded to 15% in Q1, up from 10% in the same period last year. The company carries over $1 billion in cash, has no debt, and expects to generate over $350 million in free cash flow this year.

The margin story is where it gets more complicated. Gross margin is expected to step down from around 72% today to roughly 69% by year-end as AI-powered features expand across the product. That compression flows through to the bottom line, which is why the company is guiding full-year EBITDA margins around 25% despite posting 29% in Q1.

Forward EPS estimates are essentially flat over the next two years, removing a catalyst that growth investors would normally lean on. Management is making a deliberate choice to prioritize long-term product quality and user engagement over near-term profitability. Whether that trade-off pays off depends almost entirely on what happens with subscriber conversion over the next few years.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What a Fair Price for DUOL Actually Looks Like Right Now

TIKR’s valuation model targets around $170 for DUOL, implying roughly 55% total return from current levels over about five years, or around 10% annualized. The mid-case assumes revenue growing around 10% annually through 2030, with net income margins expanding to roughly 33%. There is no assumption of multiple expansions baked in. The model simply assumes the business executes and the stock gradually closes the gap to fair value.

What the Bulls Are Betting On:

- AI is compounding content velocity. Duolingo published over 20,000 course units in Q1 alone, a 10x improvement versus two years ago. More content, better learning outcomes, and stronger retention are the foundation of the long-term monetization case.

- The user base is structurally under-monetized. Subscriber penetration relative to total downloads remains low, which management views as upside rather than a ceiling. Ongoing experiments around free trials and the Super tier are aimed directly at closing that gap.

- Asia is becoming a meaningful growth driver. China leads regional DAU expansion, and profitable performance marketing is now possible in select markets due to improved infrastructure. International growth diversifies the revenue base beyond the core English-speaking markets.

- The balance sheet provides real optionality. With over $1 billion in cash, no debt, and more than $350 million in expected free cash flow this year, management has room to invest, buy back stock, and pursue acquisitions without financial pressure.

What the Bears Are Watching:

- Bookings growth is decelerating sharply in the near term. Guiding to around 6% bookings growth in Q2 is a meaningful step down, and even the full-year guidance of 10 to 12% implies the business is running at a fraction of its recent growth rate.

- Gross margin compression is coming. Exiting the year with a 69% gross margin, versus where the business has historically operated, creates a headwind that compounds near-term EPS pressure.

- Forward EPS is essentially flat for two years. Revenue is growing, but earnings per share are not, which limits the near-term earnings narrative and makes the current multiple harder to justify for growth-oriented investors.

- The multiple is still elevated relative to near-term fundamentals. Forward EBITDA of around 14 times and forward earnings of 16 times are not distressed valuations. If growth continues to disappoint, there is room for further multiple compression before the stock reaches a level where the risk-reward is clearly favorable.

Should You Invest in DUOL?

Duolingo is a business with genuine quality. Free cash flow margins are exceptional for a consumer internet company, the balance sheet is clean, and the AI-driven content engine represents a real structural advantage that is difficult to replicate quickly. Nothing in the fundamentals suggests the franchise is permanently impaired.

The tension is that quality and valuation are distinct. Even after a 78% decline from its highs, DUOL is not obviously cheap. Investors paying around 14 times forward EBITDA today are essentially paying for a recovery in bookings growth and subscriber conversion that has not yet shown up in the numbers. If the investment cycle extends longer than expected or conversion rates stay stubbornly low, there is a reasonable path to further downside before the model’s assumptions play out.

For patient investors with a multi-year time horizon, the current price offers a reasonable starting point for a measured position. The TIKR model’s projected 10% annualized return is an honest reflection of the uncertainty involved rather than a signal that the risk-reward is clearly in your favor.

What to watch over the next few quarters is straightforward: does bookings growth reaccelerate in the back half of the year as management has guided, and does subscriber conversion improve as the new AI features reach more of the user base? Those two data points will do more to clarify the investment case than anything else.

Analyze DUOL stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!